Stress-testing a portfolio means understanding four interconnected risk factors: relative performance in downturns, volatility, drawdown depth and recovery time, and asset correlations. Private markets have historically shown lower drawdowns and better risk-adjusted returns. Diversification doesn't eliminate loss — it manages the irreducible uncertainty inherent in all investing.

Diversifying investments can manage inherent market risk and mitigate unpredictability.

Assess risk by understanding how assets perform relatively in downturns, their volatility, drawdowns, and correlations.

Optimise your portfolio's risk-adjusted returns to get the best compensation for the risk you take

In the first part of this series, {{Diversification and portfolio resilience: Part 1 – Carving conviction}}, we focused on how diversification helps you capture upside—aligning your portfolio with your worldview and positioning for growth. But the real test of any portfolio isn’t when things go right. It’s when they don’t.

No matter how sophisticated your investment strategy or how granular your due diligence, markets are non-linear. Information is incomplete. Timing is unpredictable. And even the best data is backwards-looking.

This makes investing inherently risky. One way to mitigate this risk is through diversification. By spreading investments across various asset classes, industries, and geographical regions, the risks associated with each investment can offset one another.

Risk is relative

First things, first: when markets unravel, they rarely do so in isolation. Risk doesn’t show up neatly in one corner of your portfolio—it cascades. And when that happens, the question isn’t “what’s safe?” It’s “what’s safer relative to everything else?”

That’s why downside protection is a relative exercise. Most assets may decline during market stress. Meanwhile, as we’ll soon see, some have historically shown smaller drawdowns or faster recoveries. For your risk assessment, this means understanding four things:

Relative performance: Which assets tend to fare better in a downturn?

Volatility: How sharp and frequent are the pricing swings?

Drawdown: How far an asset falls from its peak, and how long it takes to recover.

Correlated behaviour: How your exposures move together when markets buckle?

As you’ll see, these factors are inherently interlinked. However, it is worth considering them in isolation before we bring them all together.

Some assets demonstrate greater resilience during downturns

During periods of market stress, some assets fall harder than others—i.e., their performance diverges based on factors such as liquidity, capital structure, and exposure to macroeconomic variables. These differences reflect each asset’s structure and underlying value drivers.

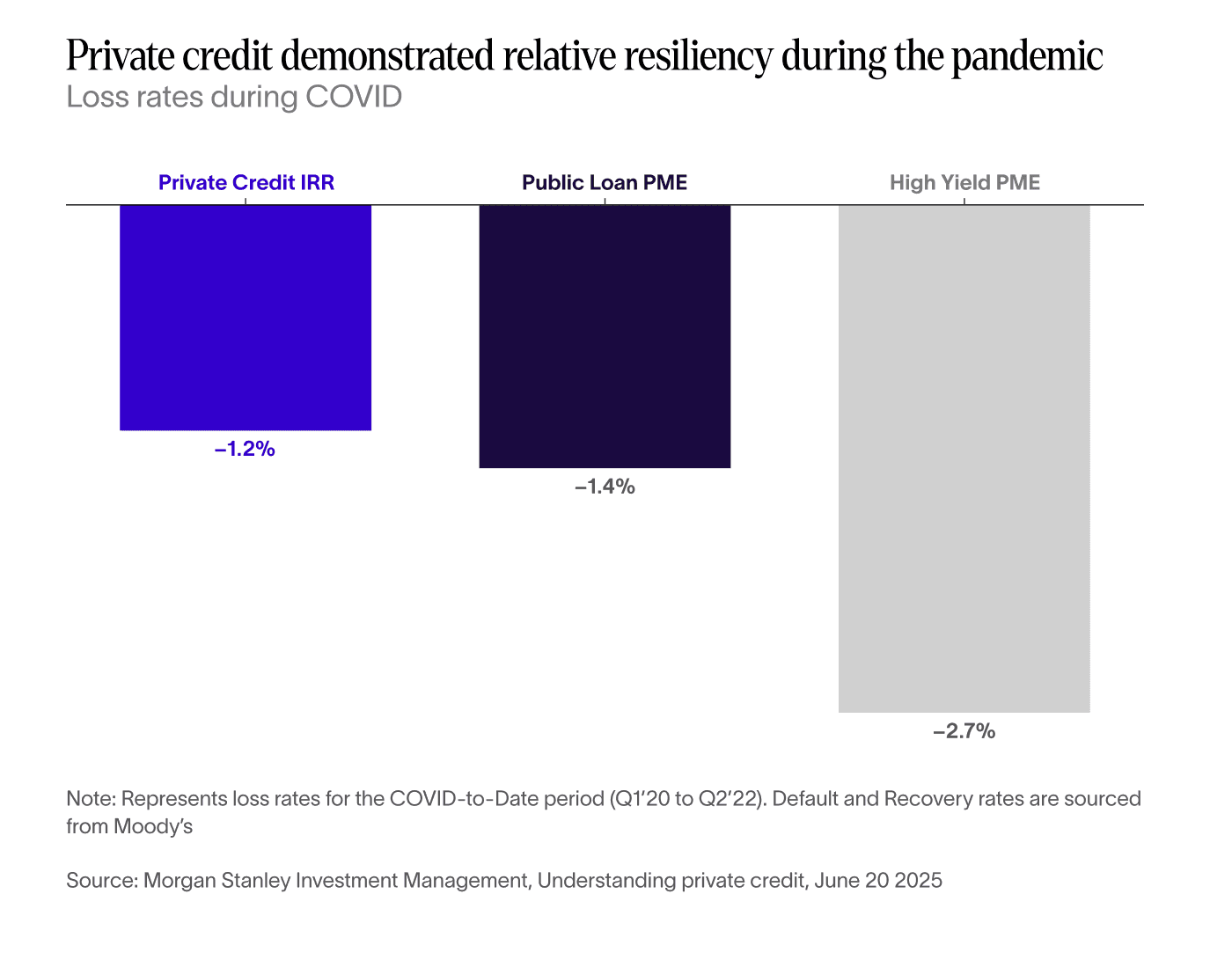

Understanding what insulates one asset class while another collapses is key to building true resilience. Take COVID: a live-fire stress test across global markets. Between the onset of the pandemic in Q1 2020 and Q2 2022, direct lending fell just 1.1%, while leveraged loans dropped 1.3% and high-yield bonds sank 2.2%.¹

What volatility means for allocation

When assessing downside risk, it’s not just about how far assets can fall—but how erratically they behave on the way there. Volatility helps capture this dynamic.

Volatility measures the degree of variation in an asset’s returns over time, typically expressed as annualised standard deviation. It doesn’t indicate whether returns are positive or negative—only how dispersed they are. Lower volatility means less extreme price swings, which can reduce tail-risk exposure and improve overall portfolio stability, especially when compounded across time and across assets.

This matters in portfolio construction because volatility influences how much risk each asset contributes. Even a small position can create outsized instability if its price movements are sharp and frequent.

Take private and public equity as an example. Over the past three decades (to 30 June 2024), the Cambridge Associates U.S. Buyout Index delivered approximately 15% annualised returns with 11% volatility, compared with around 10% and 17%, respectively, for the MSCI World Index.² These are historical index figures based on different compositions and methodologies, so they are not directly comparable. Past performance is not a reliable indicator of future results. That said, historical patterns suggest that private equity—particularly when combined with less correlated assets— has, in certain periods, may help stabilise a diversified portfolio in certain periods, subject to strategy, structure, and manager execution.

When losses linger: Why drawdown is the real test of resilience

While volatility is abstract, drawdown is tangible. It tells you what it actually feels like to live through a market crisis.

Drawdown is the peak-to-trough decline of a portfolio or asset—expressed as a percentage—before it recovers to its previous high.

That matters for two reasons:

Losses hurt more than gains help. A 25% drop requires a 33% gain to break even. A 50% drawdown? You need to double your money just to recover.

Recovery takes time—and fortitude. Deep drawdowns don’t just test portfolios. They test investors’ resolve, especially under liquidity pressure.

Let’s say your portfolio peaks at USD 1 million, falls to USD 700,000, and eventually recovers. Your drawdown was:

A 30% drawdown may take months—or even years—to recover. During that time, investors may face constraints on liquidity, reduced flexibility to rebalance, or pressure to exit positions prematurely, particularly when broader uncertainty persists.

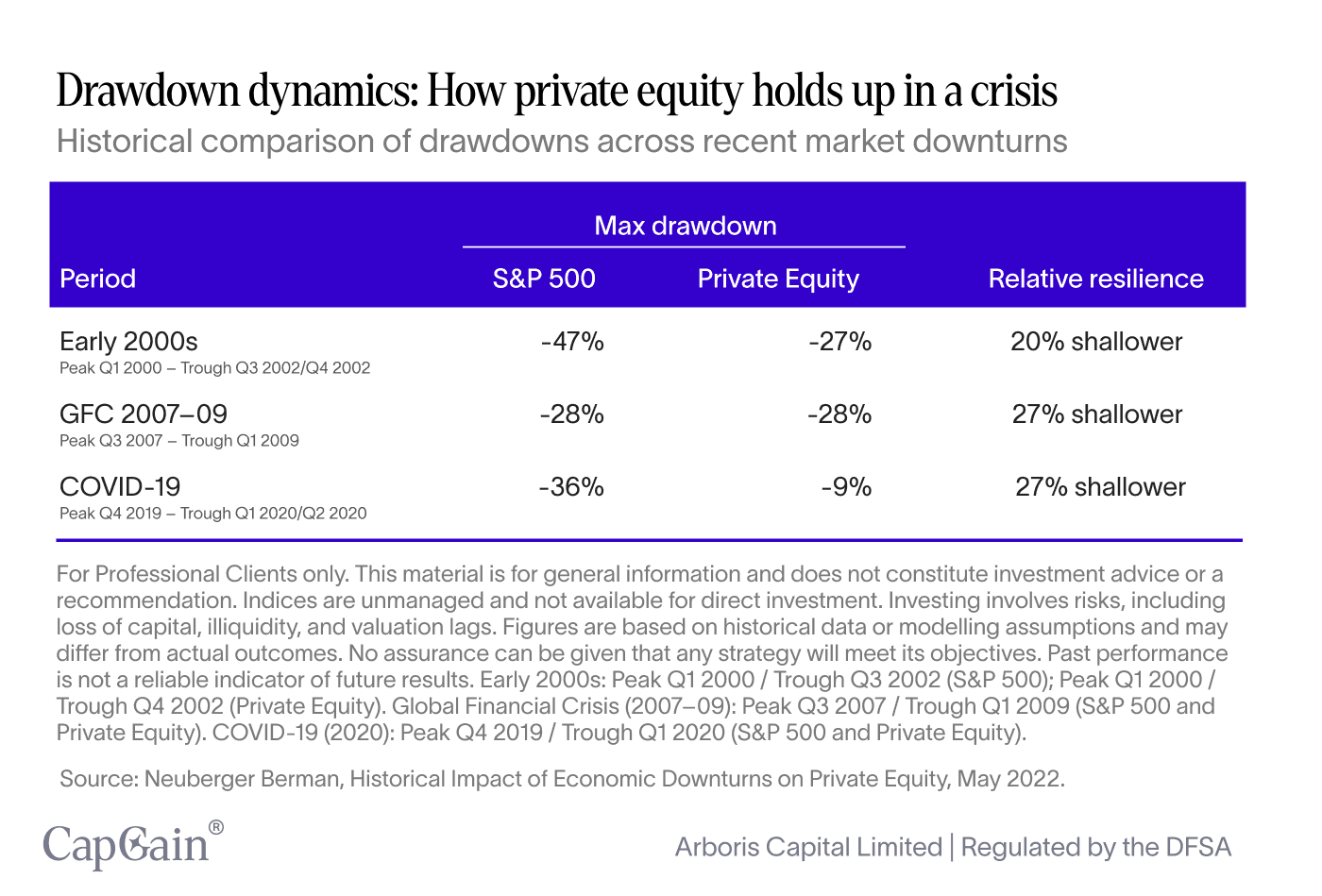

Case study: Private Equity vs Public Markets in a crisis

According to Neuberger Berman, in three major periods of market stress—the early 2000s, the Global Financial Crisis (2007–09), and COVID (2020)—private equity consistently showed lower drawdowns and faster recoveries than public equities.³

In the periods analysed by Neuberger Berman, private equity drawdowns in those periods were reported to be roughly half as severe as public equity, despite similar macro shocks. This is a testament to private equity’s structural characteristics: long-term capital, slower mark-to-market pricing, and often superior downside protection via operational control and covenant structures.

What correlation means for portfolio resilience

Financial markets are inherently interlinked. When markets are calm, you can afford to ignore those linkages. But risk tends to be systemic. Stress in one part of the system rarely stays contained. It spills, accelerates, and compounds. So the question isn’t just what each asset does on its own—it’s how they behave as a group when pressure hits.

Here, correlations can offer some guidance.

You want to find classes of assets that have less correlation, both historically and conceptually.

Historical correlation: Historical correlation tells you how asset classes have moved together in the past. It’s a useful reference point—but not a fixed rule. Correlations are not static. They shift across market regimes, interest rate cycles, and macro shocks. In 2020, many investors learned this the hard way: long-duration bonds and growth equities—once assumed to diversify each other—moved in lockstep as interest rate sensitivity converged. Understanding how these relationships evolve is critical for navigating systemic risk.

Conceptual correlation: This is where experience and intuition come in. It’s about asking: What are the underlying drivers of this asset’s performance? Do its cash flows depend on the same macro forces—rates, liquidity, credit spreads—as other parts of your portfolio? If so, it might behave more like them in a crisis than the historical data suggests.

In short, history gives you clues. But conceptual correlation tells you where the risks might show up next time.

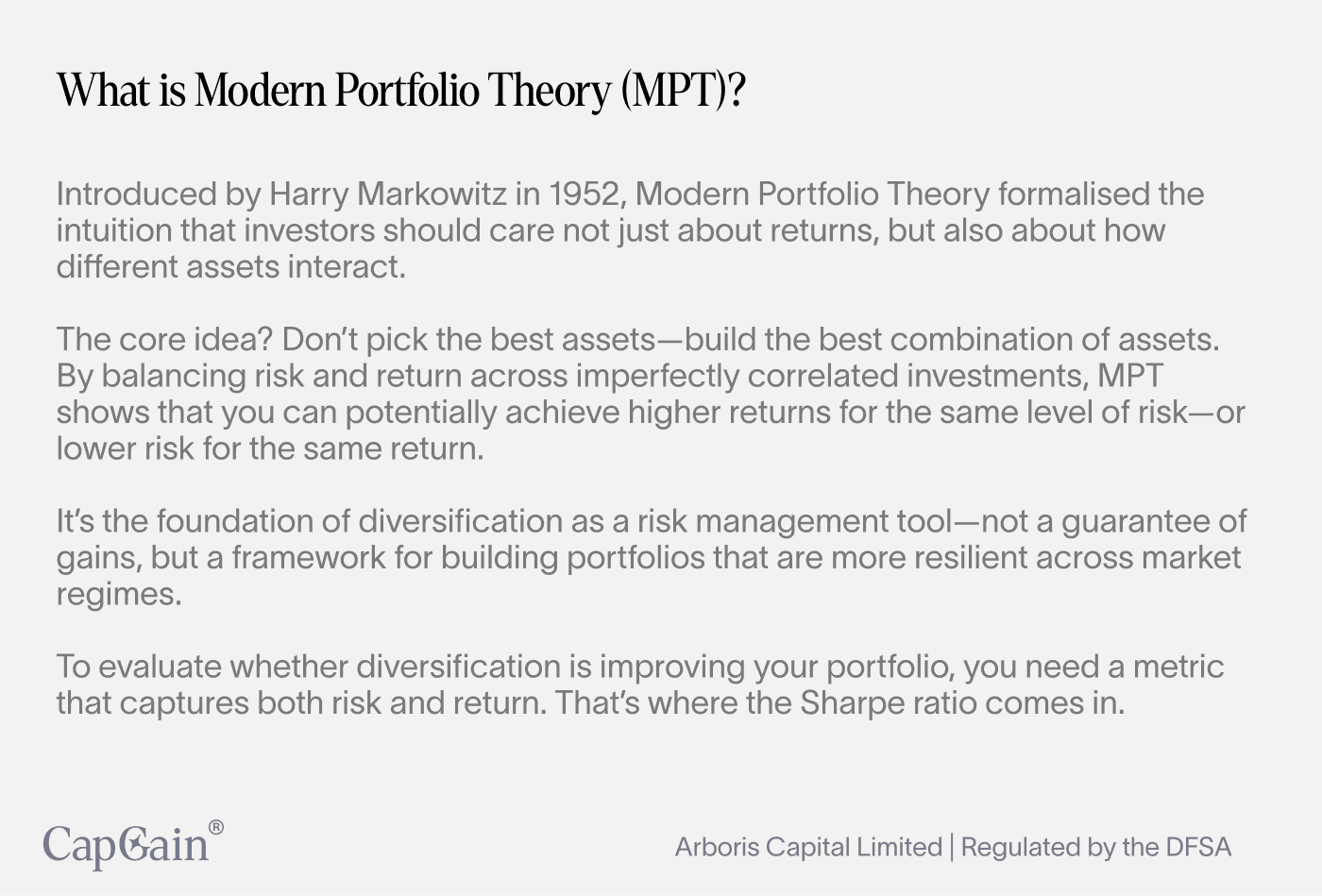

Risk reward: The essence of portfolio efficiency

Until now, we’ve discussed risk and return as distinct considerations. But in reality, they’re

intrinsically linked. As such, the question isn’t “How do I get the highest return?” but “How do I get the most return for the risk I’m taking?” That shift in perspective is at the heart of modern portfolio theory.

Sharpe ratio

The Sharpe Ratio measures the amount of excess return you receive for the extra volatility you endure. In other words, it’s a way to quantify whether you're being properly compensated for taking on additional risk.

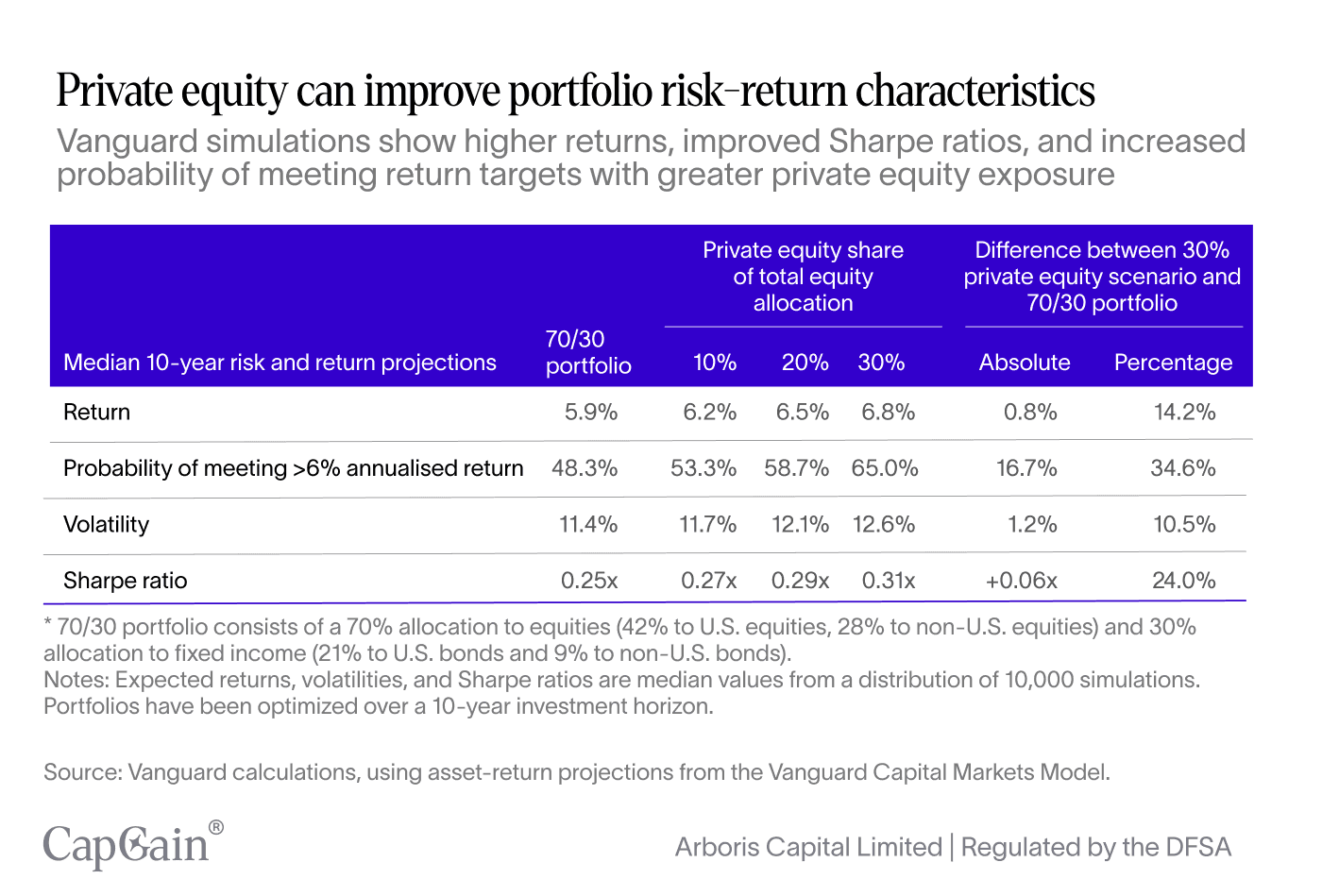

In a Vanguard simulation using historical asset class data and hypothetical portfolio construction, a model portfolio with a 30% allocation to private equity (within a 70% equity / 30% fixed income structure) produced a Sharpe ratio of 0.31x, compared with 0.25x for the same portfolio without private equity exposure. Furthermore, this allocation could yield higher nominal annualised returns, increasing from 5.9% to 6.8%.⁴

Note: These results are based on historical data, modelling assumptions, and are illustrative only; they do not represent actual or guaranteed performance.

This quantitative enhancement suggests that private markets can enhance a portfolio's risk-adjusted performance. Keeping in mind that performance varies widely across vintages and managers, and outcomes are highly path-dependent.

Box: What is Sharpe ratio?

What it measures:

The Sharpe Ratio evaluates an investment’s return relative to its risk. It tells you how much excess return you're getting for each unit of volatility you’re taking on.

Forumla

Why it matters:

Two portfolios might have the same return, but the one with lower volatility will have a higher Sharpe Ratio. That makes it a crucial metric for assessing risk-adjusted performance across asset classes. Higher is generally better—but it’s not infallible. It assumes returns are normally distributed and can underrepresent tail risk.

Use it to:

Compare different portfolios or asset classes on equal footing

Spot when returns come with disproportionate risk.

Final thoughts

“Diversification is protection against ignorance.”

— Peter Thiel (echoing Buffett), PayPal Co-founder & Venture Capitalist

In volatile, path-dependent markets, diversification acts as a practical hedge against what even the best analysis cannot predict in advance. In this context, “ignorance” is not a lack of effort, but the irreducible uncertainty and model risk inherent in investing.

Because when you invest, you are essentially "placing a bet" on an unknown future. You place capital in motion based on how you think the world will unfold. But history reminds us: even the most precise bets can unravel in the face of macro shocks, black swans, or plain old policy shifts.

That’s where diversification earns its keep: as a response to the limits of foresight.

Spreading exposure across imperfectly correlated assets can help reduce the impact of being wrong on any single position. However, diversification does not eliminate loss risk or ensure profits. Moreover, what constitutes effective risk mitigation depends on your specific goals, constraints, and risk appetite.

Morgan Stanley Investment Management, Understanding private credit, June 20 2025, Accessed July 23 2025. https://www.morganstanley.com/ideas/private-credit-outlook-considerations

Ares Wealth Management Solutions, Building with private markets in 5 charts, March 2025, Accessed 23 July 2025. https://www.areswms.com/sites/default/files/2025-03/Private-Markets-in-5-Charts-Brochure.pdf

Nueberger Berman, The Historical Impact of Economic Downturns on Private Equity: An assessment of private equity return patterns in three recent significant downturns, December 2022, Accessed August 5 2025. https://www.nb.com/handlers/documents.ashx?id=d72a6d24-0994-4a90-acb9-145601940a3b

Vanguard Private Equity Perspectives, The diversification benefits of private equity, October 2023, Accessed July 22 2025 https://corporate.vanguard.com/content/dam/corp/research/pdf/vanguard_diversification_benefits_of_private_equity.pdf

Written by

Sarah Hansen

Head of Research

Disclaimer – For Professional Clients Only

This communication is intended solely for persons classified as Professional Clients as defined by the Dubai Financial Services Authority (DFSA). It is not directed at Retail Clients and should not be relied upon by any person who does not meet the criteria for classification as a Professional Client. The information provided herein is for general informational purposes only and does not constitute, and should not be construed as, an offer, solicitation, invitation, or recommendation to buy, sell, or otherwise transact in any investment product or to engage in any investment strategy.

The subject matter discussed does not relate to a DFSA-regulated financial product or service. The content is intended only to provide a general update on market conditions and does not consider the specific investment objectives, financial situation, or particular needs of any recipient. It should not be relied upon as the basis for any investment decision. Past performance is not a reliable indicator of future performance. The value of investments and any income from them may fluctuate, and there is no assurance that the original capital will be preserved or returned.

Although the information contained in this communication has been obtained from sources believed to be reliable, Arboris Capital Limited makes no representation or warranty as to its accuracy, completeness, or fitness for any particular purpose. No liability is accepted by Arboris Capital Limited, its employees, or affiliates for any direct or consequential loss arising from the use of or reliance on this material. Arboris Capital Limited is authorised and regulated by the Dubai Financial Services Authority (DFSA) and operates within the Dubai International Financial Centre (DIFC), United Arab Emirates.