Private equity often turns downturns into opportunity. Recession vintages benefit from lower valuations, reduced competition, and ample dry powder to deploy. By acquiring distressed or undervalued assets and driving operational improvements, firms position companies for recovery. When markets rebound, these strengthened businesses can deliver outsized returns, rewarding disciplined, well-capitalised investors.

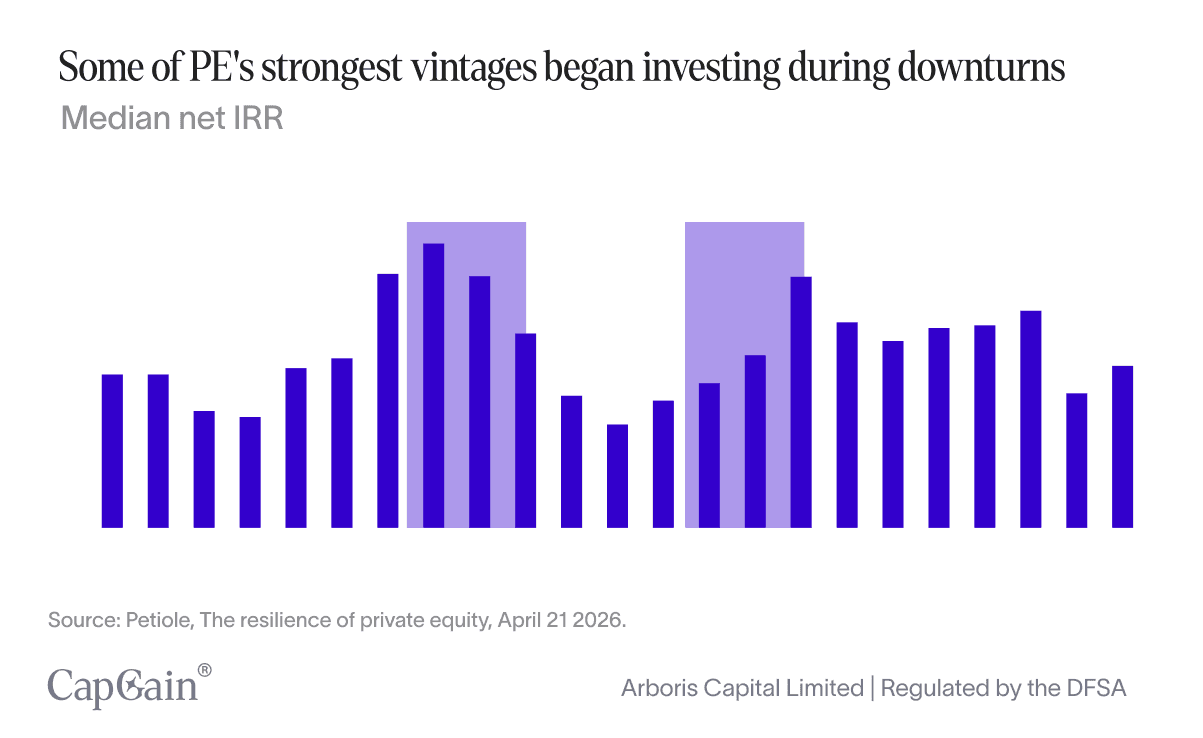

Downturn vintages can shine – Funds launched in recessions often post the strongest returns, buying quality companies at compressed valuations.

Valuation resets create opportunity – Lower asset prices and reduced competition allow private equity to negotiate favourable terms and avoid overheated bidding.

Dry powder fuels agility – Large reserves of unallocated capital let PE firms move quickly when others are sidelined, securing high-quality assets at discounts.

Distress unlocks value – Operational and financial turnarounds, as seen with Cheesecake Factory, can generate outsized profits when conditions stabilise.

Recoveries amplify gains – Companies strengthened during downturns, like Virgin Australia, are primed to capture disproportionate upside when markets rebound.

Some of the strongest vintages began investing during downturns

Recessions test every business model. They also reset valuations, thin competition, and open the door for disciplined investors to buy quality at a discount. For private equity, downturns aren’t just periods to survive—they’re moments to set the stage for future outperformance.

According to Cambridge Associates, history shows that funds launched during recessions have often gone on to deliver some of the industry’s best results.¹

With the right combination of capital, patience, and operational expertise, these vintages can turn economic headwinds into a tailwind for returns.

In the next few sections, we unpack the mechanics behind why deals struck in downturns can deliver exceptional outcomes—from buying at compressed valuations, to stepping into less competitive markets, to using dry powder strategically when others are on the sidelines.

Laws of supply and demand: Buyers market

The market for private equity investments is governed by the basic laws of supply and demand: when demand exceeds supply, prices rise, and vice versa. Despite challenges such as repressed consumer spending and less fertile economic conditions, economic downturns also present unique opportunities for private equity firms.

Firstly, entry valuations tend to be lower during economic downturns as asset prices fall. This provides private equity firms with opportunities to acquire companies at a discount, potentially yielding higher returns as the economy recovers and valuations increase.

Moreover, economic downturns lead to a less competitive landscape. In times of economic uncertainty, there is generally less competition for acquisitions. With fewer buyers in the market, private equity firms can negotiate more favourable terms and avoid bidding wars that can inflate purchase prices during economic booms.

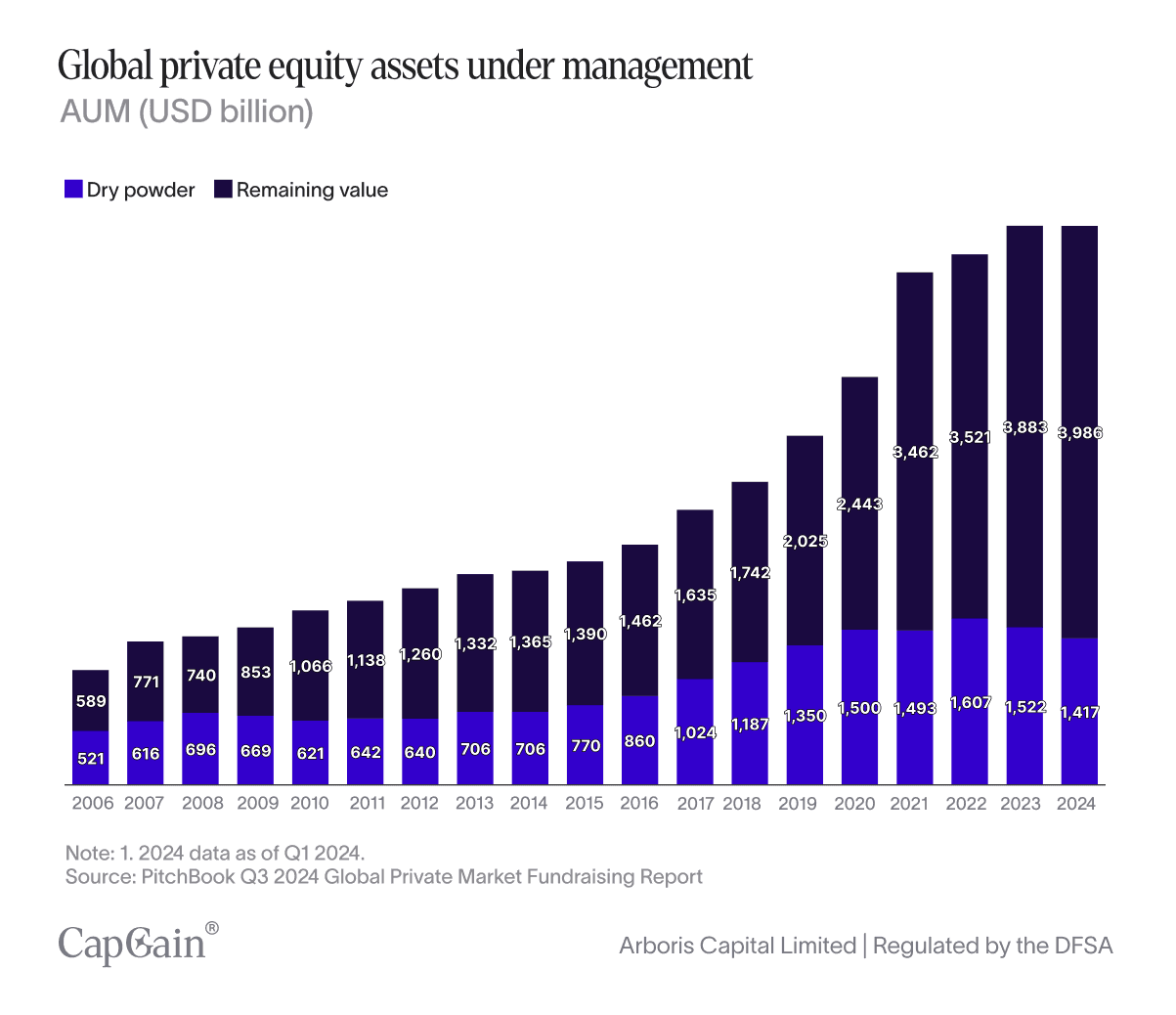

Additionally, private equity firms often enter recessions with substantial reserves of unallocated capital, known as “dry powder.” This capital, raised during preceding periods of market strength, gives them the flexibility to act decisively when asset prices fall and competition for deals is lower. By deploying dry powder into high-quality assets at depressed valuations, PE firms can position portfolios to capture outsized gains during the eventual recovery. Let’s see what that looks like in practice.

Distressed opportunities

Downturns create environments where businesses face operational and financial distress. Private equity firms, with their expertise in restructuring and strategic realignment, can capitalise on these situations. By injecting capital and operational improvements, they can turn around struggling companies, creating substantial value.

The Cheesecake Factory is a notable example from the COVID-19 pandemic. In early April 2020, the restaurant chain reported that first-quarter same-store sales had fallen about 13%, with March sales plunging roughly 46% as lockdown measures forced dining room closures. The company temporarily shut 30 locations—including three Cheesecake Factory restaurants—and faced significant liquidity pressure.²

It was in this context that Roark Capital invested USD 200 million in April 2020, bolstering the company’s balance sheet and providing the financial runway to weather the crisis “This transaction not only meaningfully enhances our liquidity position to navigate the near-term COVID-19 landscape and get our affected staff members back to work as soon as practicable,” said David Overton, Cheesecake Factory CEO and chairman, “but also importantly, solidifies our ability to manage the business for the long-term for all of our stakeholders once we emerge on the other side of this crisis.”

Cheesecake Factory did indeed stabilise and reposition for long-term performance. By June 2021—just over a year later—the company had recovered sufficiently to repurchase most of Roark Capital’s equity stake in a deal valued at USD 457.3 million, delivering a net profit of USD 275.3 million to the fund.³

Benefit from economic recoveries

While downturns can feel like the point of no return, cycles do turn, and valuations often rebound sharply once macro conditions stabilise. For private equity, that rebound can be a force multiplier. With operational improvements already in place and balance sheets strengthened during the lean years, portfolio companies are primed to capture outsized gains when growth resumes.

With the help of PE professionals, investments made during downturns are well-positioned to benefit from recoveries as the economy improves, consumer confidence returns, and spending increases.

Case study: Virgin Australia

The acquisition of Virgin Australia by Bain Capital in 2020 stands out as a prominent example.

Virgin Australia, Australia's second-largest airline, entered voluntary administration in April 2020, primarily due to the severe impact of the COVID-19 pandemic on the global travel industry. This made it one of the world's largest airlines to succumb to the pressures of the pandemic.

In June 2020, Bain Capital announced it had entered into an agreement with Virgin Australia's administrators to acquire the airline for AUD 3.5billion in a bid to reposition it for future success. Bain Capital's strategy for Virgin Australia focused on several key areas to ensure its revitalisation:⁴

Operational Restructuring: Bain Capital worked on restructuring the airline's operations to make it more efficient and competitive. This included reducing the fleet size, focusing on core domestic and short-haul international routes, and cutting unprofitable routes.

Financial Health: A significant part of the strategy involved stabilising Virgin Australia's finances, which included restructuring its debt, securing new funding, and making the cost structure more sustainable.

Customer and Brand Focus: Recognising the strength of the Virgin brand, Bain aimed to maintain a strong customer service ethos, enhancing the airline's value proposition to ensure loyalty and attract new customers in a competitive market.

Adapting to Market Conditions: Bain Capital planned for a flexible approach in scaling the airline's operations, acknowledging the uncertain trajectory of the global pandemic and its impact on travel demand.

Ready for second take-off

Virgin Australia emerged from administration in November 2020, with Bain Capital's acquisition marking a new chapter for the airline. Under Bain's ownership, Virgin Australia has focused on consolidating its position in the Australian domestic market, competing effectively with its rivals, and gradually expanding its global presence.

In October 2023, Virgin Australia reported a statutory net profit after tax of AUD 129 million (USD 82.93 million) for the entire year ended June 30, 2023. This was a significant improvement from the year before, when the company reported a loss of AUD 565.5 million in 2022. The profit also marked a major milestone for the airline carrier, which had been unprofitable for 11 years.⁵

Virgin Australia’s turnaround under Bain Capital came full circle in late 2024 with a USD 1.7bn IPO on the Australian Securities Exchange, marking its return to public markets after four years in private hands. Shares closed up 11.4% on debut, boosting its market value to AUD 2.58bn and underscoring the depth of investor demand.⁶

Final thoughts

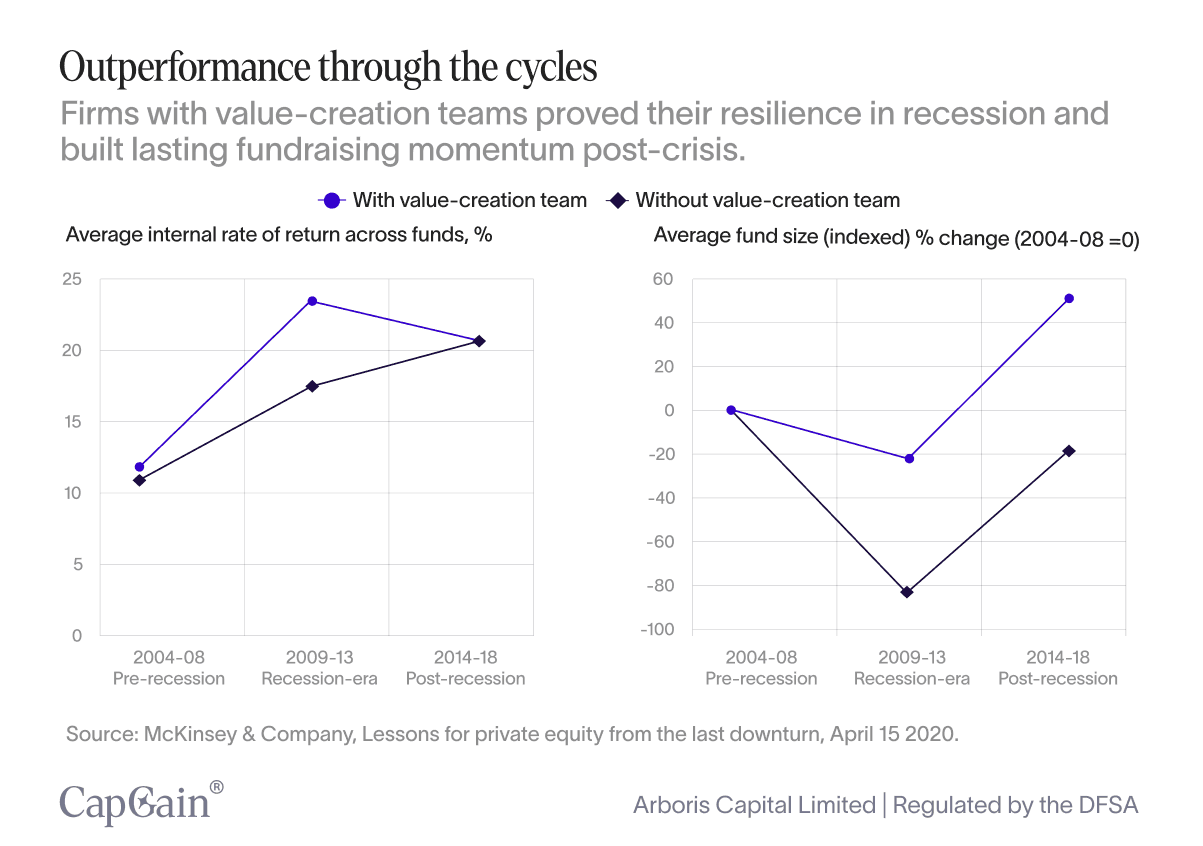

Downturns act as a natural stress test, exposing under-resourced, hands-off managers while rewarding those with the operational muscle to steer portfolio companies through turbulence. McKinsey’s research underscores the point: after 2008, firms with dedicated value-creation teams delivered IRRs of 25%, compared to just 18% for less proactive peers. Investors noticed, directing more capital to proven hands, enabling them to raise larger funds, strengthen their capabilities, and compound their advantage in the next cycle.

For investors, this dynamic can be highly constructive: market dislocations naturally differentiate managers, enabling capital to flow toward those with demonstrated resilience and operational expertise—often positioning portfolios to capture attractive opportunities as conditions improve.

Petiole, The resilience of private equity, May 3 2022, Accessed August 27 2025, https://www.petiole.com/en/insights/articles/the-resilience-of-private-equity

NRN, Roark Capital invests $200 million in Cheesecake Factory, April 20 2020, Accessed August 15 2025. https://www.nrn.com/casual-dining/roark-capital-invests-200-million-in-cheesecake-factory

Restaurant Business, Cheesecake Factory buys most of Roark's stake for $457M, June 15 2021, Accessed August 15 2025. https://www.restaurantbusinessonline.com/financing/cheesecake-factory-buys-most-roarks-stake-457-million

Private Equity Insigts, Bain-backed Virgin Australia returns to public markets with $1.7bn lift-off, https://pe-insights.com/bain-backed-virgin-australia-returns-to-public-markets-with-1-7bn-lift-off/

Virgin Australia, Virgin Australia returns to profitability in FY23, transformation plan well underway, October 9 2023, Accessed August 15 2025 https://www.virginaustralia.com/ae/en/newsroom/2023/10/virgin-australia-returns-profitability-fy23-transformation-plan-well-underway/

Private Equity Insights, Bain-backed Virgin Australia returns to public markets with $1.7bn lift-off, June 2025, Accessed August 27 2025 https://pe-insights.com/bain-backed-virgin-australia-returns-to-public-markets-with-1-7bn-lift-off/

McKinsey & Company, Lessons for private equity from the last downturn, April 15 2020, Accessed April 21 2026, https://www.mckinsey.com/industries/private-capital/our-insights/lessons-for-private-equity-from-the-last-downturn

Written by

Sarah Hansen

Head of Research

Disclaimer – For Professional Clients Only

This communication is intended solely for persons classified as Professional Clients as defined by the Dubai Financial Services Authority (DFSA). It is not directed at Retail Clients and should not be relied upon by any person who does not meet the criteria for classification as a Professional Client. The information provided herein is for general informational purposes only and does not constitute, and should not be construed as, an offer, solicitation, invitation, or recommendation to buy, sell, or otherwise transact in any investment product or to engage in any investment strategy.

The subject matter discussed does not relate to a DFSA-regulated financial product or service. The content is intended only to provide a general update on market conditions and does not consider the specific investment objectives, financial situation, or particular needs of any recipient. It should not be relied upon as the basis for any investment decision. Past performance is not a reliable indicator of future performance. The value of investments and any income from them may fluctuate, and there is no assurance that the original capital will be preserved or returned.

Although the information contained in this communication has been obtained from sources believed to be reliable, Arboris Capital Limited makes no representation or warranty as to its accuracy, completeness, or fitness for any particular purpose. No liability is accepted by Arboris Capital Limited, its employees, or affiliates for any direct or consequential loss arising from the use of or reliance on this material. Arboris Capital Limited is authorised and regulated by the Dubai Financial Services Authority (DFSA) and operates within the Dubai International Financial Centre (DIFC), United Arab Emirates.