Private equity compensation aligns managers with investor outcomes through management fees and performance-based carry. Structures like hurdles, clawbacks, and waterfalls determine how profits are shared and shape behaviour. While “2 and 20” balances stability and incentives, design nuances matter—ultimately making alignment a key driver of returns, risk-taking, and long-term investor trust.

Alignment of interest is foundational for any relationship to thrive, and the relationship between you and your asset management is no exception to this rule. Understanding how private equity fund managers are compensated is crucial for Limited Partners (LPs), as it directly impacts your net returns.

Unlike traditional public market fund managers, who often earn a flat percentage of assets under management, private equity compensation structures are designed to heavily align the GP's interests with the fund's performance and value creation.

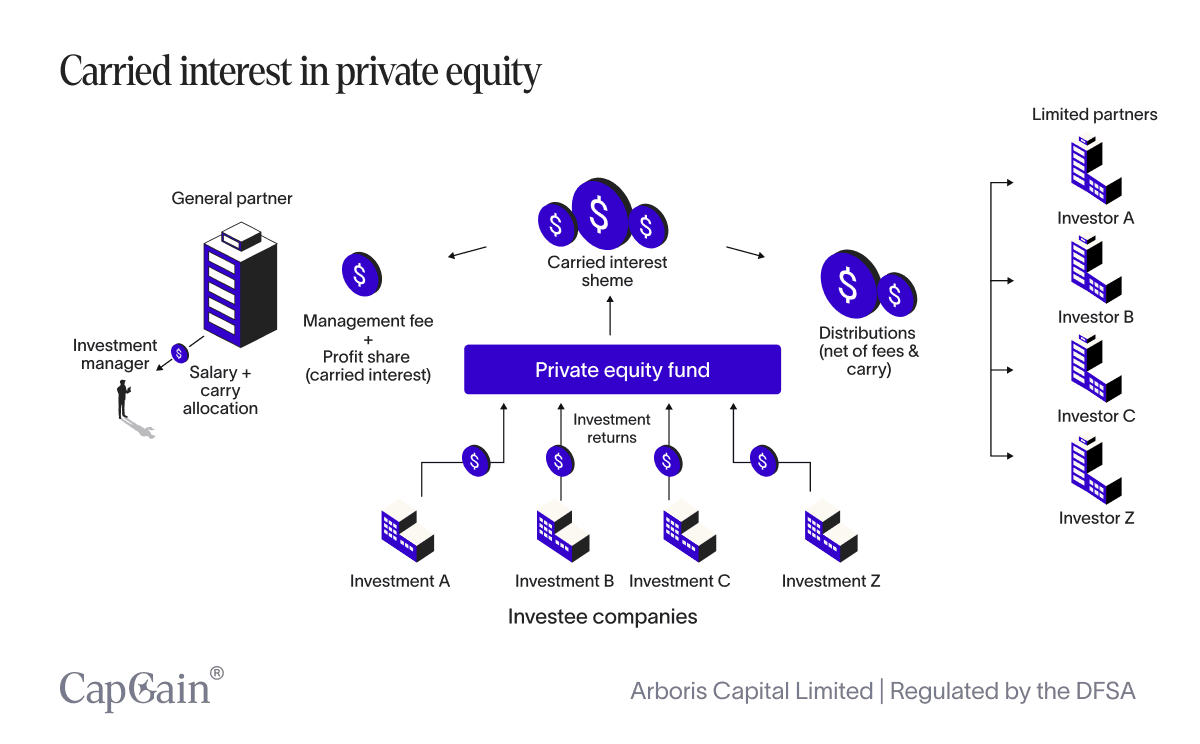

The remuneration of an investment manager (also known as the carried interest scheme) is structured into two primary components:

Management fees: These fees are based on the assets under management (AUM). They are typically expressed as a percentage of the total assets managed by the fund.

Carry: Also known as carried interest, this is a performance-based fee that allows fund managers to share in the profits of the fund.

Each component plays a critical role in shaping the manager's behaviour and aligning their interests with those of the investors. In the following sections, we’ll examine them separately and then explore their interplay.

Why is there an investment manager and a general partner?

If you’ve seen this graph before, you might wonder why the investment manager and general partner are separate in the depiction above.

The short answer: they’re two sides of the same coin — one is the legal authority, the other is the operating engine. The GP is the legal entity responsible for the fund, while the investment manager is the licensed company that runs it day-to-day. Separating them limits liability, meets regulatory requirements, and allows one manager to oversee multiple funds. Think of it as the GP signing the papers, and the investment manager steering the ship.

Management fees

Management fees cover the fund's operational expenses, such as salaries for the management team, administrative costs, and other overheads related to the day-to-day management of the fund's investments.

Management fees range from 1% to 2% per annum. The fees are typically calculated as a percentage of committed capital during the investment period (often 5 years), and then shift to a percentage of invested or remaining capital thereafter. This structure ensures a baseline operational budget early on while aligning fees more closely with deployed capital over time.

Carried interest: Driving performance beyond the baseline

Often referred to as the "carry," carried interest represents a share of the profits earned by the fund that is paid to the fund managers.

Usually, the fund manager only gains a share of the profit after reaching a certain return threshold, also known as the 'hurdle rate' or ‘preferred return’.

This motivates GPs to exceed return hurdles and unlock upside beyond the baseline.

Moreover, most funds also include a clawback mechanism, which ensures that GPs repay any excess carry if later losses reduce overall performance below the hurdle. This reinforces alignment across the full fund lifecycle.

As we’ll explore in the next sections, the carried interest structure varies significantly between the "deal-by-deal" model and the "fund-as-a-whole" model. Both approaches aim to align the interests of general partners (GPs) with those of limited partners (LPs). Still, they do so in different ways and have different implications for risk and reward distribution.

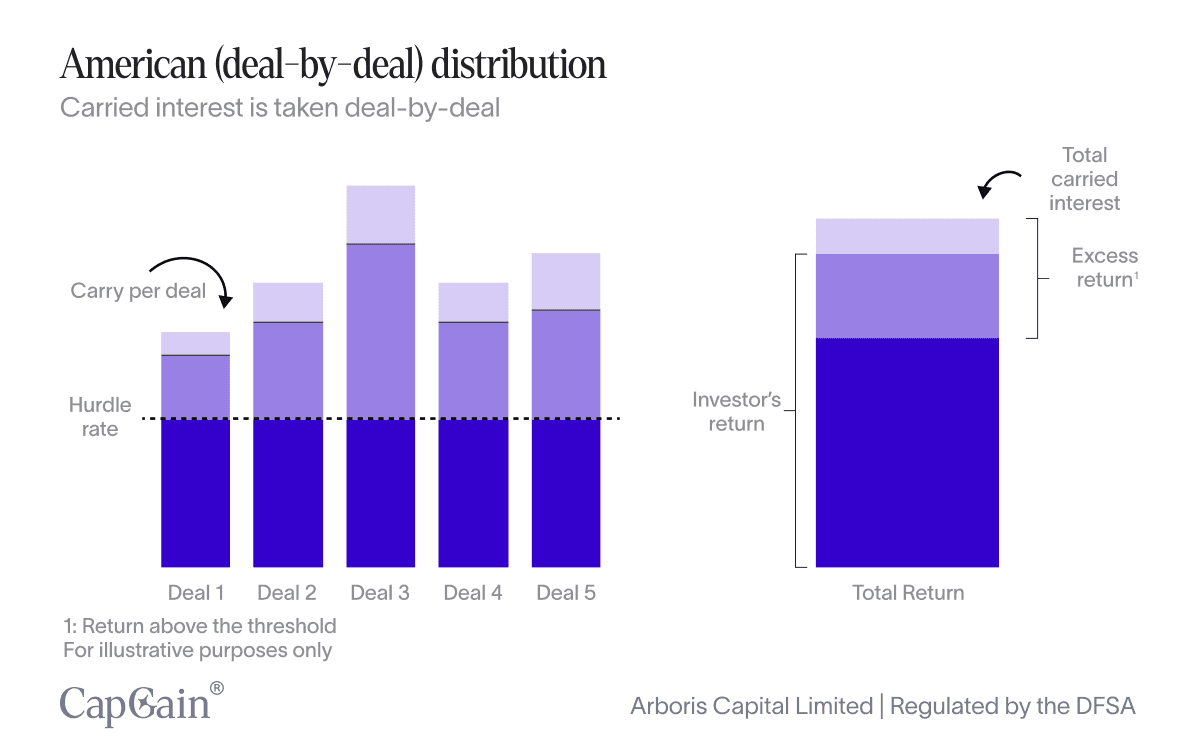

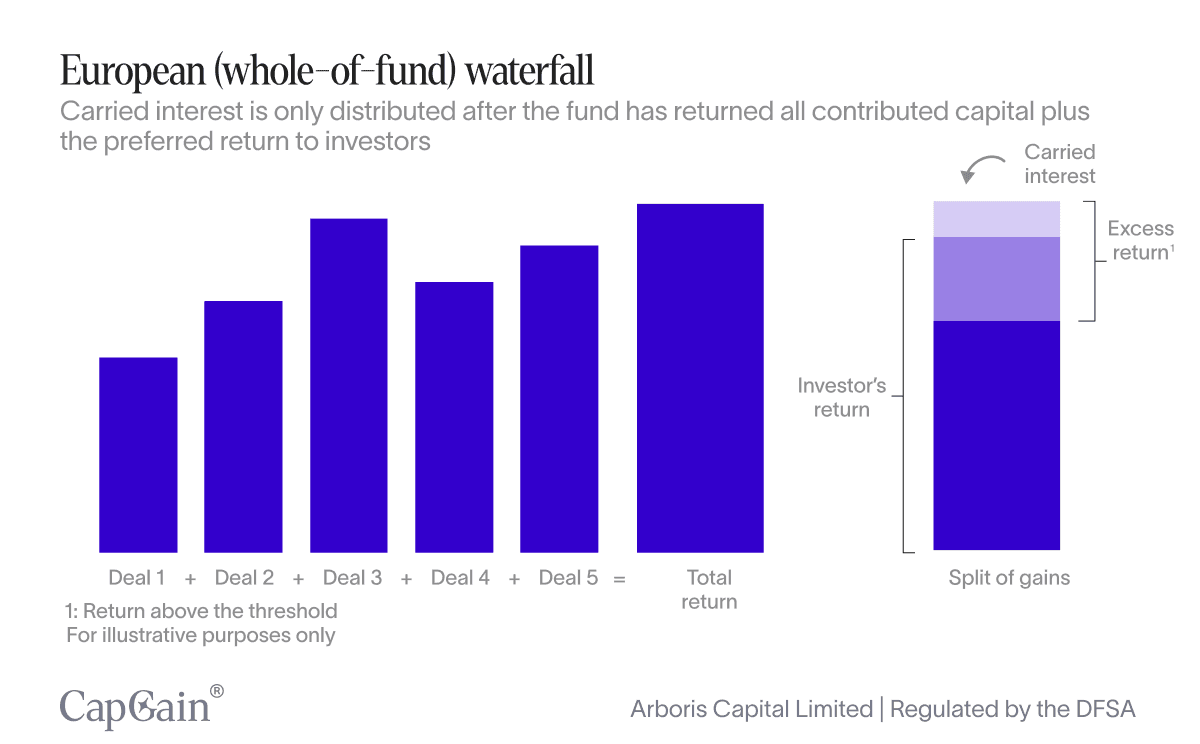

Distribution waterfalls: How profits are shared

A distribution waterfall is the formula that determines how and when profits are allocated between LPs and GPs. It ensures that LPs recover their initial capital and a preferred return before GPs participate in the upside—though how this is calculated varies.

While there are variations, two common types are ‘Deal by deal’ and ‘Fund as a whole’.

Deal-by-Deal (American Waterfall)

In this model, the GP can begin collecting carried interest on a per-deal basis once that specific investment generates a profit and reaches certain hurdles. This means the GP might receive carry even if other investments within the fund haven't yet returned capital to LPs.

The deal-by-deal model provides immediate incentives for GPs on a per-deal basis. The GP is motivated to successfully exit high-performing assets quickly to boost distributions in the short term. Meanwhile, this structure can dilute long-term alignment with LPs, as it allows GPs to earn carried interest on early wins without having to first return the entire fund’s committed capital, potentially leaving LPs exposed if later deals underperform.

Fund-as-a-Whole (European waterfall)

Considered more LP-friendly, this model requires LPs to receive their full committed capital back, plus any preferred return, across all investments in the fund, before the GP is eligible to receive any carried interest.

This compensation structure, particularly the carried interest, is a powerful incentive for GPs to maximise the value of portfolio companies and achieve profitable exits, as their ultimate financial reward is directly tied to the fund's success.

Delays in compensation for GPs, as they must wait until the end of the fund’s life or until all investments are realised to receive their carried interest. Moreover, it may discourage GPs from pursuing individual deals with high potential if they do not significantly impact the fund’s overall performance.

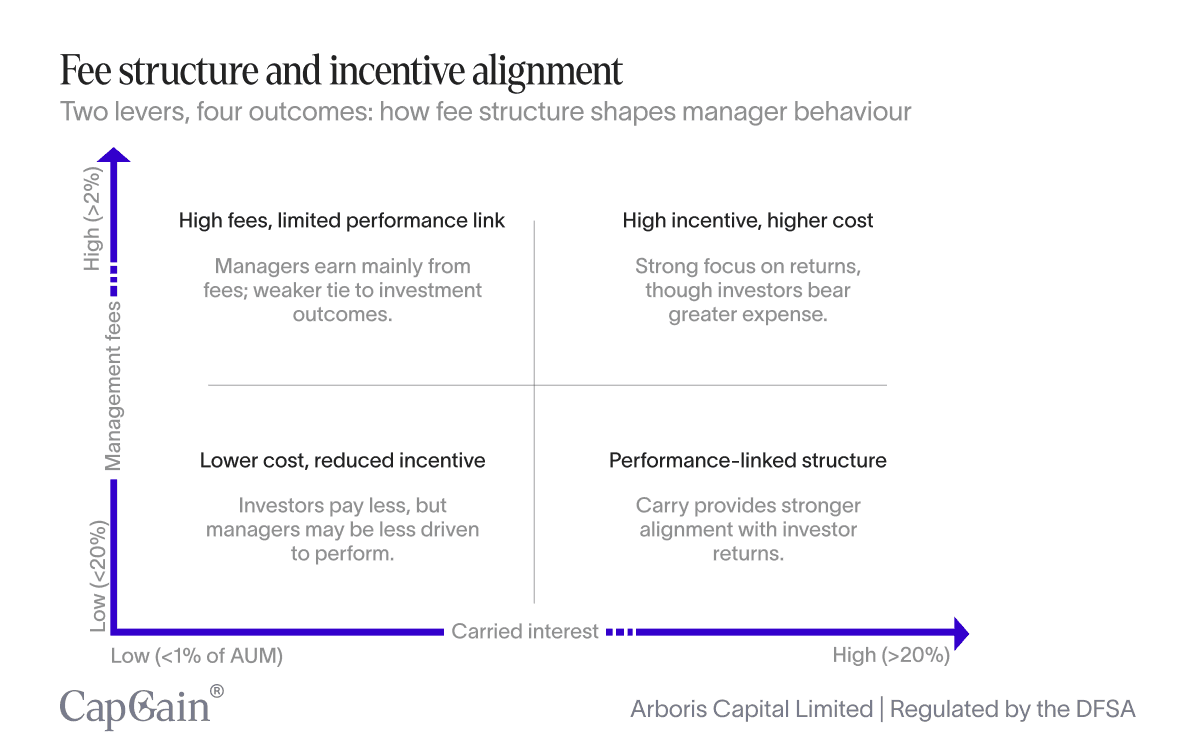

Compensation structure dictates behaviour

The interplay between carried interest and management fees significantly shapes fund manager incentives—and, by extension, fund outcomes. A purely fixed fee model—typically a flat percentage of assets under management (AUM)—can create complacency. Since compensation is decoupled from fund performance, managers may lack sufficient motivation to pursue alpha beyond preserving capital or scaling AUM. In essence, they get paid whether the fund performs or not.

Furthermore, predictable revenue from management fees can reduce cost discipline for GPs. Without pressure to earn performance-based compensation, managers may allow operational overhead to expand unchecked, potentially eroding net returns for Limited Partners (LPs).

Conversely, dialling down fixed fees and emphasising carried interest—a share of the profits earned only after achieving a performance hurdle—can better align General Partner (GP) incentives with LP outcomes. In this structure, GPs are rewarded for generating real economic value. But this model isn't without risk: with their compensation tied heavily to performance, GPs may be tempted to take outsized bets, skewing toward high-return, high-risk strategies that could jeopardise capital preservation.

Prevalent fee arrangement in private equity: “2 and 20”

The “2 and 20” model—comprising a 2% management fee and 20% carried interest—is frequently observed in the private markets industry and is intended to balance stable operational funding for GPs with performance-linked incentives for LPs.

The 2% management fee provides baseline operational funding, ensuring GPs can maintain a stable team, infrastructure, and deal sourcing capability without depending on uncertain profits.

The 20% carry ensures GPs have substantial skin in the game, rewarded only if they generate returns above a predefined threshold (the “preferred return” or “hurdle,” often around 8%).

This blend avoids both extremes: it discourages fee-driven asset gathering, while still providing the stability necessary to run the fund professionally. When structured well, with proper clawback provisions, hurdles, and escrow mechanics, it remains a durable model that may incentivise long-term value creation, aligning interests across stakeholders.

Final thoughts

When it comes to private market investing, the manager’s remuneration shapes how they behave, and ultimately how (and when) you get paid.

If this feels like an added layer of complexity to your investment analysis, don’t worry. Striking the right balance is crucial, not just for investors but also for the managers themselves. Keep in mind, private market investing is a long game, underpinned by long-lasting and mutually beneficial relationships.

A fund manager’s ability to raise funds depends on the success of his previous funds, and the success of his previous funds comes down to one thing: investor satisfaction.

At CapGain, we understand the importance of balanced relationships. That’s why we screen all managers diligently to ensure that incentives are aligned. Because long-term capital requires long-term trust.

Written by

Sarah Hansen

Head of Research

Disclaimer – For Professional Clients Only

This communication is intended solely for persons classified as Professional Clients as defined by the Dubai Financial Services Authority (DFSA). It is not directed at Retail Clients and should not be relied upon by any person who does not meet the criteria for classification as a Professional Client. The information provided herein is for general informational purposes only and does not constitute, and should not be construed as, an offer, solicitation, invitation, or recommendation to buy, sell, or otherwise transact in any investment product or to engage in any investment strategy.

The subject matter discussed does not relate to a DFSA-regulated financial product or service. The content is intended only to provide a general update on market conditions and does not consider the specific investment objectives, financial situation, or particular needs of any recipient. It should not be relied upon as the basis for any investment decision. Past performance is not a reliable indicator of future performance. The value of investments and any income from them may fluctuate, and there is no assurance that the original capital will be preserved or returned.

Although the information contained in this communication has been obtained from sources believed to be reliable, Arboris Capital Limited makes no representation or warranty as to its accuracy, completeness, or fitness for any particular purpose. No liability is accepted by Arboris Capital Limited, its employees, or affiliates for any direct or consequential loss arising from the use of or reliance on this material. Arboris Capital Limited is authorised and regulated by the Dubai Financial Services Authority (DFSA) and operates within the Dubai International Financial Centre (DIFC), United Arab Emirates.