Private equity has historically shown resilience during downturns, with smaller drawdowns and consistent outperformance versus public markets. Its strength lies in active ownership—using operational improvements, strategic flexibility, and long-term capital to navigate cycles. Outcomes vary widely, but skilled managers can mitigate downside risk and position portfolio companies for recovery and sustained value creation.

Private equity has historically shown resilience during economic downturns, often outperforming public markets like the S&P 500.

Private equity firms bring a wealth of experience and have blueprints for navigating economic uncertainties.

Through adaptive strategies such as adjusting pricing models and enhancing marketing efforts, private equity can help portfolio companies maintain and even grow revenue during downturns.

Economic downturns seldom spare anyone; they ripple through industries, unsettle capital flows, and leave balance sheets bruised. In such cascades, there are few true winners. That said, history shows private equity (PE) has repeatedly demonstrated an ability to mitigate key risk factors, and in many cases, deliver superior long-term outcomes relative to public markets.

Resilient performance through market stress

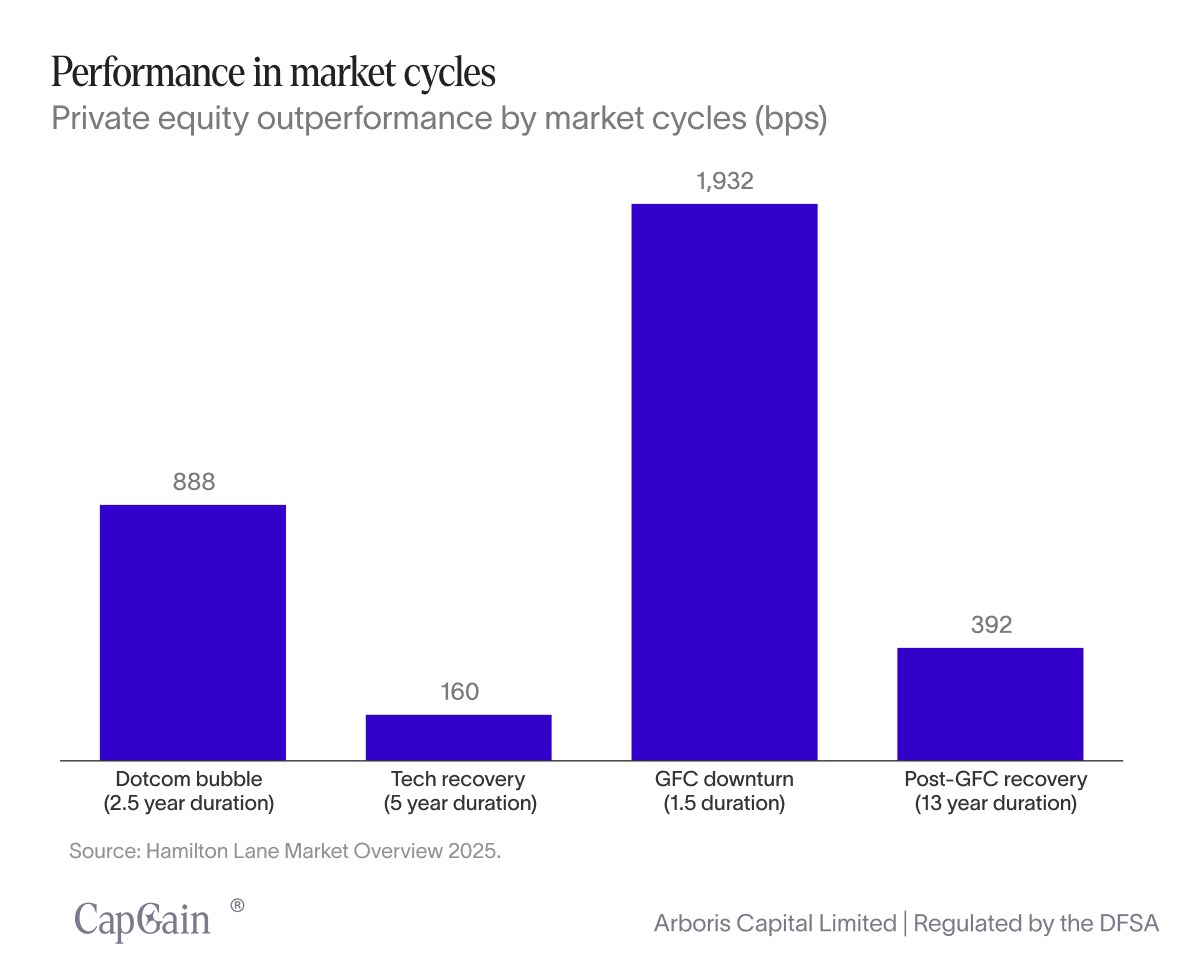

Private equity’s historical resilience has translated into meaningful outperformance across market cycles. Analysis by Hamilton Lane shows PE outperformed public market benchmarks by: ¹

888 bps during the dotcom bubble (2.5 years)

160 bps during the subsequent tech recovery (5 years)

1,932 bps in the GFC downturn (1.5 years)

392 bps in the post-GFC recovery (13 years)

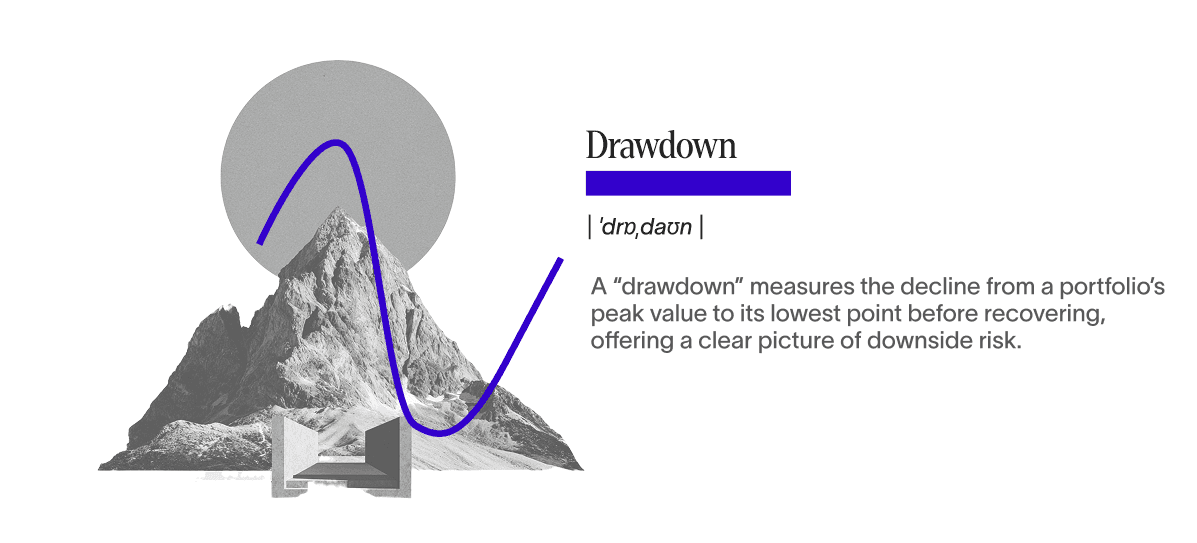

Shallower drawdowns vs. public benchmarks

Across multiple drawdown periods — from the dot-com bubble to the global financial crisis (GFC), the COVID-19 pandemic, and the post-pandemic adjustment — PE has experienced smaller peak-to-trough declines than major public market benchmarks:²

Dot-com bubble: PE declined 21.0%, compared with a 43.8% drop for the S&P 500.

GFC: The S&P 500 fell 45.8%, while PE drawdowns were limited to 27.5%.

COVID-19 sell-off: PE losses were 8.7% versus 19.6% for the S&P 500.

Post-pandemic: PE slipped 3.5%, compared with a 23.3% decline in the S&P 500.

Note: A “drawdown” measures the decline from a portfolio’s peak value to its lowest point before recovering, offering a clear picture of downside risk.

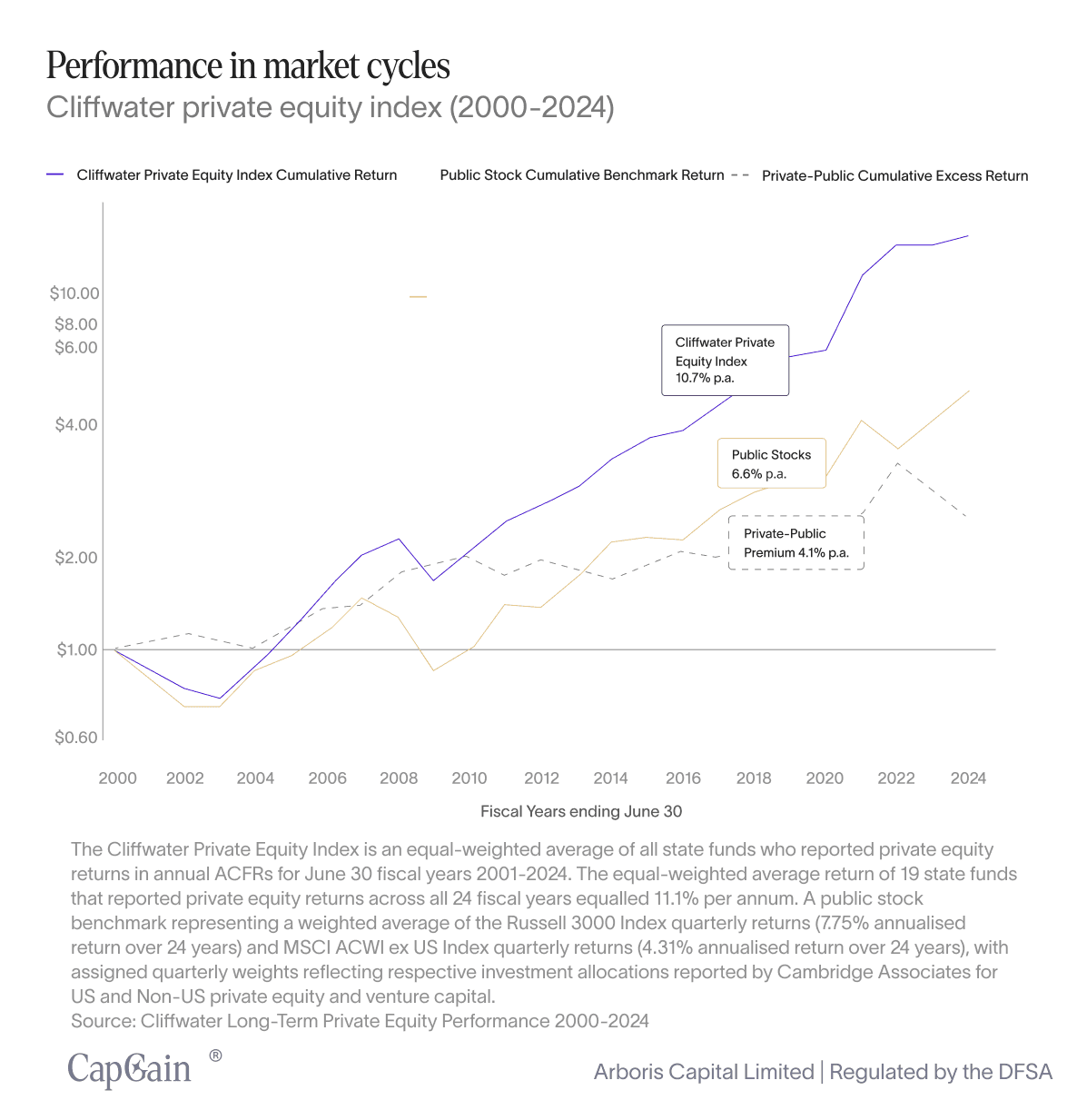

Consistent premium over public equities

Indices show the trend, but what does actual investor experience look like? To shed light on this, Cliffwater’s analysis of U.S. state pension plans provides a real-world benchmark.

Over the 22-year period ending June 30, 2024, U.S. state pension allocations to PE achieved an annualised net-of-fee return of 10.7%, compared with 6.6% for public equities — a premium of 4.1 percentage points per year.³

The private equity strategy spectrum: Navigating and capitalising through cycles

With a long-term perspective, private equity (PE) firms can implement strategic changes, operational improvements, and growth initiatives without the pressure of short-term market expectations. This flexibility enables portfolio companies to focus on sustainable, long-term value creation.

While these results do not guarantee future outperformance, they do pinpoint a unique facet of private equity, namely the ability to navigate uncertainty and economic headwinds.

Private equity firms employ a range of strategic approaches to navigate economic downturns and capitalise on market opportunities.

Adaptive: Involve adjustments to pricing models and marketing efforts to preserve and grow revenue.

Reactive: Focus on prioritising core competencies and divesting non-core assets to maintain stability.

Proactive: Drive long-term efficiency and competitive advantage through investments in technology and innovation.

Opportunistic: Leverage economic stress to expand market presence, acquire undervalued assets, and gain a competitive edge.

Each of these approaches plays a crucial role in enabling private equity firms to create and sustain value across diverse market conditions. Moreover, a private equity firm will often have weathered several storms, and it will have tried-and-tested blueprints for navigating times of uncertainty.

Operational efficiency: The secret is in the symbiosis

In times of economic stress, enhancing operational efficiency in portfolio companies is another critical strategy for private equity (PE) firms. Revenue strategies alone cannot successfully navigate an economic downturn; therefore, PE firms often couple revenue enhancements with operational overhauls and productivity improvements.

Cost rationalisation: Reviewing and rationalising costs, including renegotiating supplier contracts, reducing overheads, and streamlining operations to eliminate inefficiencies.

Process optimisation: Implementing lean management techniques and process improvements, such as adopting new technologies, automating repetitive tasks, and optimising supply chains.

Asset utilisation: Maximising asset use efficiency by selling underutilised assets, consolidating facilities, or investing in upgrades that improve operational efficiency.

Workforce optimisation: Adjusting workforce levels and productivity to match current operational needs, including training and development to enhance employee skills and productivity.

Talent acquisition: Seizing the opportunity to strengthen teams by acquiring top talent during downturns when companies downsize or close.

Negotiation leverage: Leveraging fewer buyers in the market to negotiate favourable terms with suppliers, leading to better costs of goods sold (COGS), improving margins, and competitive pricing strategies.

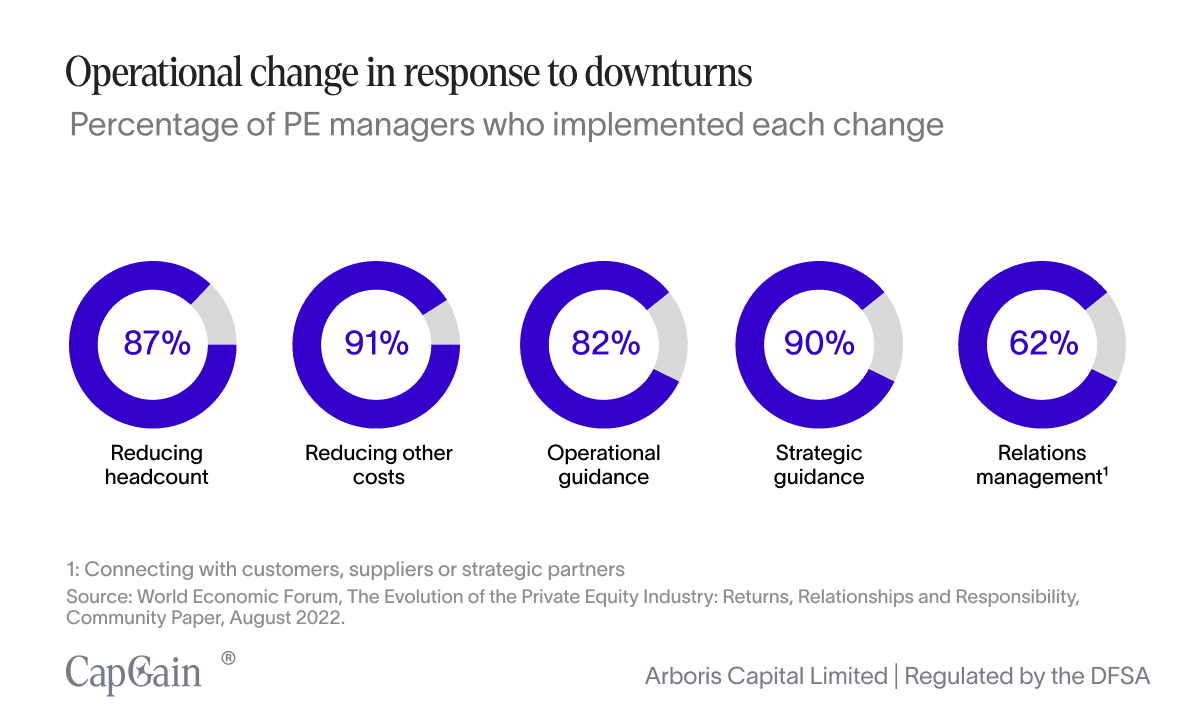

A study by the World Economic Forum⁴ revealed that PE firms during the pandemic employed various strategies to navigate the economic slowdown, ranging from strategic and operational guidance to cost reduction efforts. Some PE managers even extended their support by liaising between the portfolio company and its customers, suppliers, and strategic partners.

This holistic approach helps weather downturns and positions companies for stronger performance and valuation as the economic climate improves.

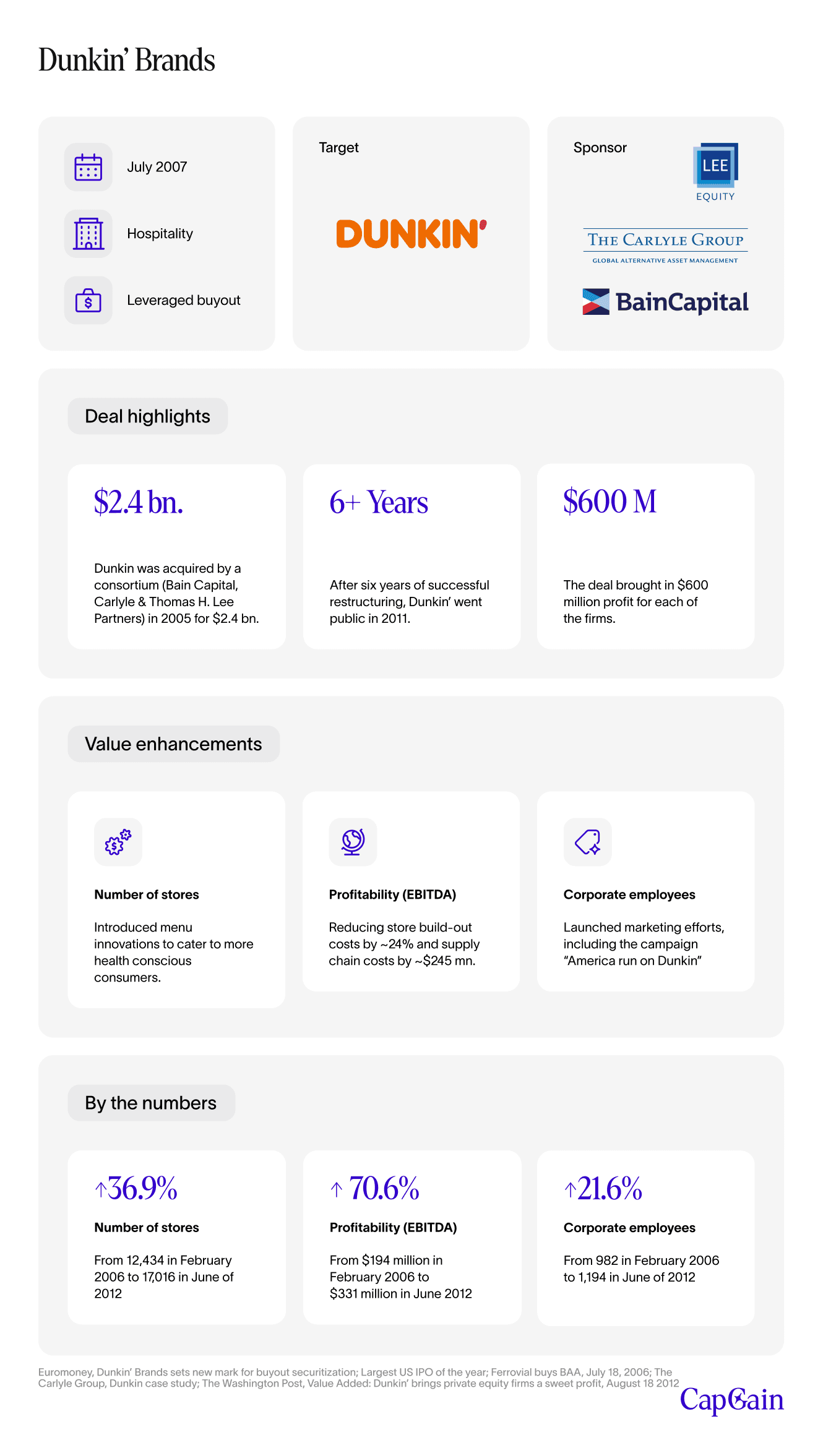

Case study: Dunkin’ Brands

An example of a private equity-owned company which navigated economic downturn with the guidance of private equity is Dunkin' Brands, the parent company of Dunkin' Doughnuts and Baskin-Robbins.

In 2006, Bain Capital, Carlyle Group, and Thomas H. Lee Partners, each acquired a 33% stake at a USD 2.4 billion valuation.⁵

Less than two years after the acquisition, the global financial crisis hit, posing a substantial threat to Dunkin' Brands due to high debt levels and decreased consumer spending. To address these challenges, Dunkin' Brands implemented various strategies to accommodate changing consumer spending patterns.

They targeted health-conscious consumers by offering healthier snacks, such as egg-white breakfasts, and expanded their menu with lunches and espresso Turbo Shots. To retain cost-conscious consumers, they introduced value offerings. This balanced approach helped maintain and attract new customers.

These initiatives were promoted through an extensive marketing campaign called “What are you Drinkin’?” and "America Runs on Dunkin."

Between 2008 and mid-2012, Dunkin’ opened 2,125 new domestic stores—many in untapped markets—demonstrating the brand’s potential beyond its traditional footprint. The company also accelerated international growth, adding 2,800 net new stores across China, India, and Latin America.

Core to this expansion was a focus on franchisee economics. The team implemented initiatives to improve store-level returns, including menu simplification, standardised store designs, and supply chain optimisation—cutting build-out costs by ~24% and reducing supply chain expenses by USD 245 million.⁶

By the time of its IPO in 2011, the firm had not only stabilised but scaled, delivering USD 600 million in profit to each sponsor. It was a case study in how private equity, even amid a crisis, can engineer operational resilience and growth.⁷

Final thoughts

History shows that private equity has the potential to navigate periods of market disruption more effectively than many public market strategies, at times delivering superior long-term results. That said, past performance is no guarantee of future outcomes, and returns can vary significantly depending on market conditions, strategy, and — perhaps most importantly — the quality of the manager.

Manager selection remains a decisive factor: the dispersion between top-quartile and bottom-quartile managers can mean the difference between meaningful outperformance and material underperformance. For investors with the expertise, resources, and patience to conduct thorough due diligence and commit to a long-term horizon, private equity can offer a differentiated and potentially resilient path through economic uncertainty. However, the asset class is complex, illiquid, and carries the risk of capital loss — making informed, disciplined entry essential.

Hamilton Lane, Market Overview 2023, Accessed August 15 2025, https://www.hamiltonlane.com/en-us/news/hamilton-lane-2023-market-overview

Pitchbook, Private Capital Indexes, Q4 2024, Accessed August 15 2025. https://files.pitchbook.com/website/files/pdf/Q4_2024_PitchBook_Private_Capital_Indexes_19104.pdf

Clifwater, January 13 2025, Long-term private equity performance 2000-2024, Accessed August 15 2025. https://cliffwater.com/ResourceArticle/longterm-private-equity-performance-20002024?docId=26043

World Economic Forum, The Evolution of the Private Equity Industry: Returns, Relationships and Responsibility – Community Paper, August 2022, Accessed August 15 2025. https://www3.weforum.org/docs/WEF_Private_Equity_Industry_2022.pdf

Dunkin’ Brands sets new mark for buyout securitization; Largest US IPO of the year; Ferrovial buys BAA, July 18, 2006, Accessed August 26 2025 https://www.euromoney.com/article/27bjsstsqxhkmh1h5ne7j/capital-markets/dunkin-brands-sets-new-mark-for-buyout-securitization-largest-us-ipo-of-the-year-ferrovial-buys-baal.

The Carlyle Group, Dunkin case study, Accessed 15 2025, https://www.carlyle.com/sites/default/files/case-studies/Dunkin_case_study.pdf

The Washington Post, Value Added: Dunkin’ brings private equity firms a sweet profit, August 18 2012, Accessed 15 2025. https://www.washingtonpost.com/value-added-dunkin-brings-private-equity-firms-a-sweet-profit/2012/08/16/2d82857c-e5d0-11e1-8741-940e3f6dbf48_story.html

Written by

Sarah Hansen

Head of Research

Disclaimer – For Professional Clients Only

This communication is intended solely for persons classified as Professional Clients as defined by the Dubai Financial Services Authority (DFSA). It is not directed at Retail Clients and should not be relied upon by any person who does not meet the criteria for classification as a Professional Client. The information provided herein is for general informational purposes only and does not constitute, and should not be construed as, an offer, solicitation, invitation, or recommendation to buy, sell, or otherwise transact in any investment product or to engage in any investment strategy.

The subject matter discussed does not relate to a DFSA-regulated financial product or service. The content is intended only to provide a general update on market conditions and does not consider the specific investment objectives, financial situation, or particular needs of any recipient. It should not be relied upon as the basis for any investment decision. Past performance is not a reliable indicator of future performance. The value of investments and any income from them may fluctuate, and there is no assurance that the original capital will be preserved or returned.

Although the information contained in this communication has been obtained from sources believed to be reliable, Arboris Capital Limited makes no representation or warranty as to its accuracy, completeness, or fitness for any particular purpose. No liability is accepted by Arboris Capital Limited, its employees, or affiliates for any direct or consequential loss arising from the use of or reliance on this material. Arboris Capital Limited is authorised and regulated by the Dubai Financial Services Authority (DFSA) and operates within the Dubai International Financial Centre (DIFC), United Arab Emirates.