Venture capital pools investor capital to fund high-growth start-ups, deploying it selectively after rigorous screening. Returns are driven by a small number of breakout successes, while most investments fail. Beyond capital, VCs provide strategic support. The model is high-risk, high-reward—built on diversification, long time horizons, and the power-law dynamics of innovation-driven growth.

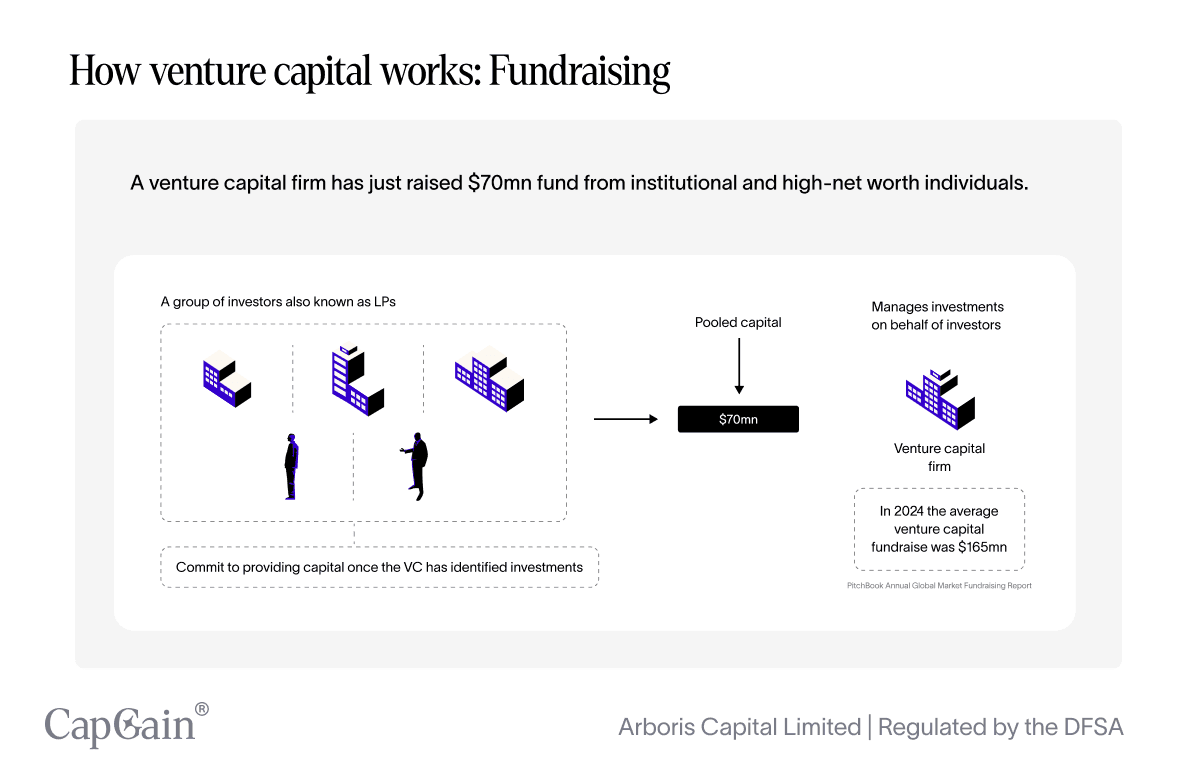

Venture capital firms raise pooled capital from institutional investors and high-net-worth individuals (LPs).

Capital is only deployed once the VC identifies investments that fit its mandate.

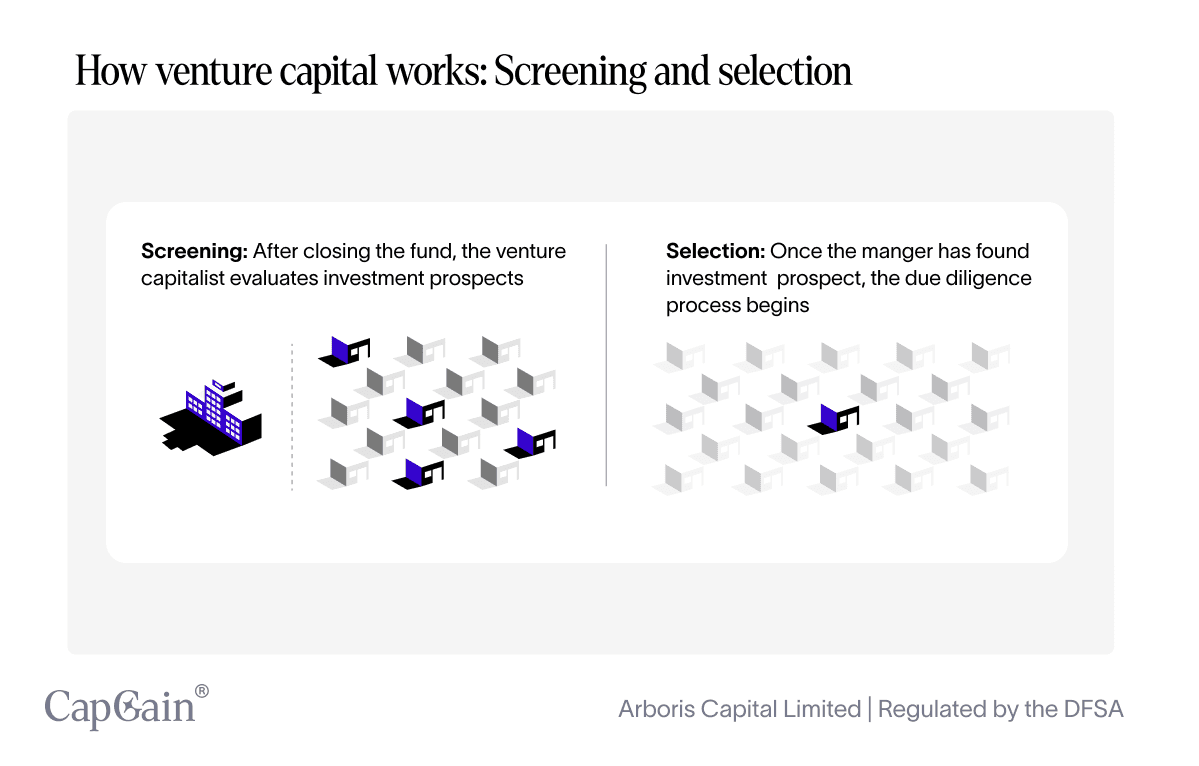

Investments undergo a rigorous screening and due diligence process before funding.

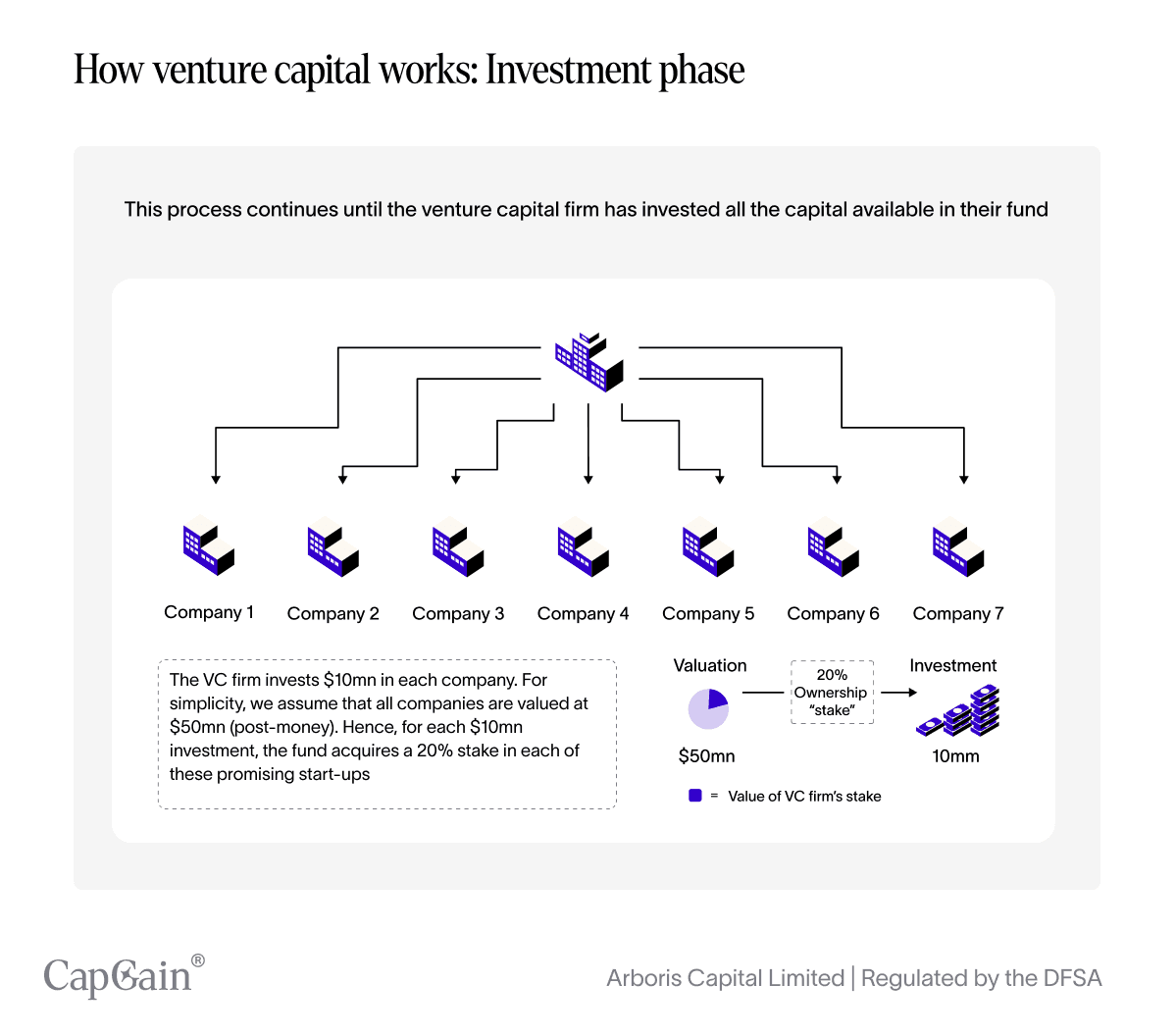

Funds are spread across multiple companies to diversify risk.

VCs provide mentorship, strategic guidance, and industry connections, not just money.

Many start-ups fail; a few succeed, and returns are heavily concentrated in the winners.

Venture capital (VC) is often portrayed as a mysterious engine behind the world’s most successful start-ups. In reality, while the industry can be complex, its underlying mechanics follow a fairly structured process. Here’s a clear breakdown of how venture capital works—from fundraising to investment returns.

Fundraising

The journey begins with the venture capital firm itself. A VC firm raises money from institutional investors and high-net-worth individuals who become limited partners (LPs). These investors commit capital, which the VC pools into a fund managed on their behalf.

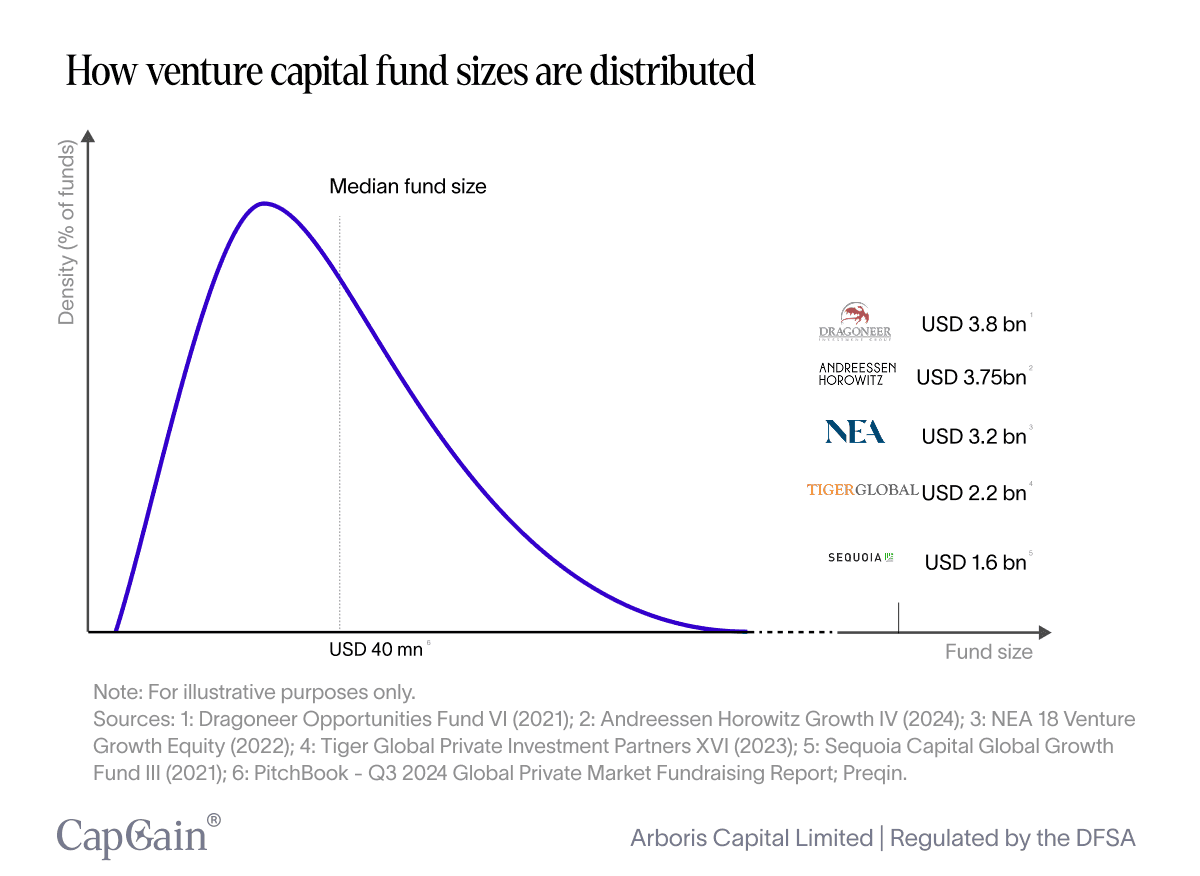

To ground this in reality: in 2024 the average venture capital fundraise was USD 165 million, according to the PitchBook Annual Global Fundraising Report. The median was USD 40 million.¹

The difference between these two figures illustrates the skewness of VC fund sizes. Most funds are relatively small, clustered around the lower tens of millions. Meanwhile, a handful of large venture capital firms such as Dragoneer Investment Group, Andreessen Horowitz, New Enterprise Associates and Sequoia, pull the average far above the median with fund raises far above the billion-dollar mark.² This is known as a right-skewed distribution: the “tail” of very large values stretches the scale upward.

Screening opportunities

Now, let’s imagine that a VC firm has raised a USD 70 million fund.

This money is not deployed all at once but invested gradually as the firm identifies promising opportunities.

Once the fund closes, the VC turns its attention to sourcing and evaluating potential investments. Every opportunity is first assessed against a predefined investment mandate—criteria such as industry, stage of growth, or geography.

When a start-up looks promising, the VC conducts due diligence. This process involves digging into the company’s financials, risks, market potential, and overall business model. In short, due diligence is about asking: Is this really “the one”?

Making investments

With opportunities vetted, the VC begins deploying capital. Suppose our USD 70 million fund invests USD 10 million into each of seven companies. For simplicity, assume each start-up is valued at USD 50 million post-money.

That means for every USD 10 million invested, the VC acquires a 20% ownership stake. At this stage, the VC holds pieces of several promising ventures, effectively diversifying risk across the portfolio.

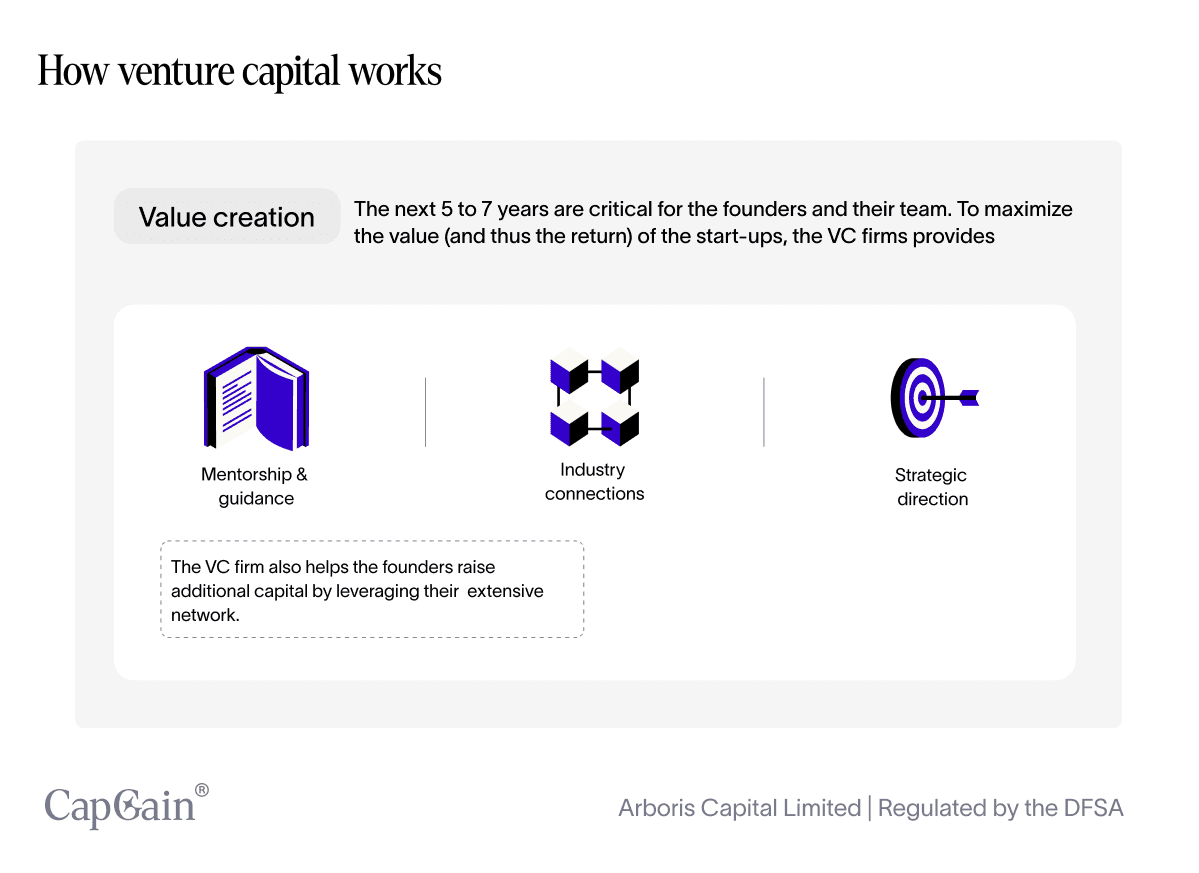

Value creation

Over the next five to seven years, the VC actively works with portfolio companies to build value. This is not a passive investment. VC firms typically provide:

Mentorship and guidance to help founders navigate challenges.

Industry connections that open doors to customers, talent, and future investors.

Strategic direction to strengthen business models and scale efficiently.

Beyond this, VCs often help companies raise additional rounds of funding, leveraging their networks to attract more capital.

Harvesting investments

Eventually, it’s time to realise returns. Some companies succeed, while others fail or stagnate.

In our example, let’s say Companies 5 and 6 grow substantially, achieving valuations of USD 250 million and USD 500 million, respectively. The VC’s stakes, diluted over time to 6%, are now worth USD 12.5 million and USD 25 million. Meanwhile, several other companies fail and shut down. This dynamic reflects the high-risk, high-reward nature of venture capital. A handful of winners can more than compensate for the losers.

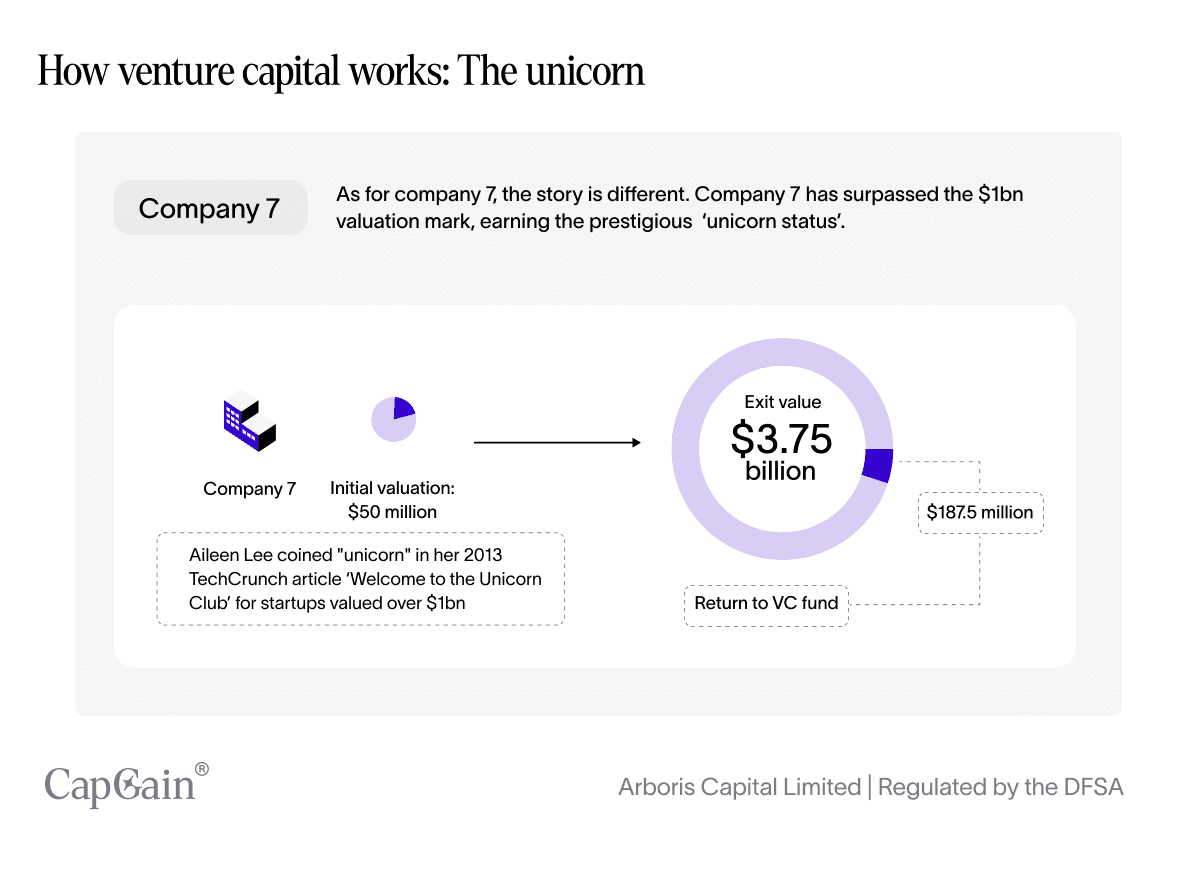

The one in 7: The unicorn outcome

But occasionally, a start-up breaks away from the pack. In our example, Company 7 surpasses the coveted USD 1 billion valuation, earning “unicorn” status—a term coined by Aileen Lee in 2013.

With a valuation of USD 3.75 billion, the VC’s diluted 6% stake is now worth USD 187.5 million—a single investment that dramatically shifts the fund’s overall performance.

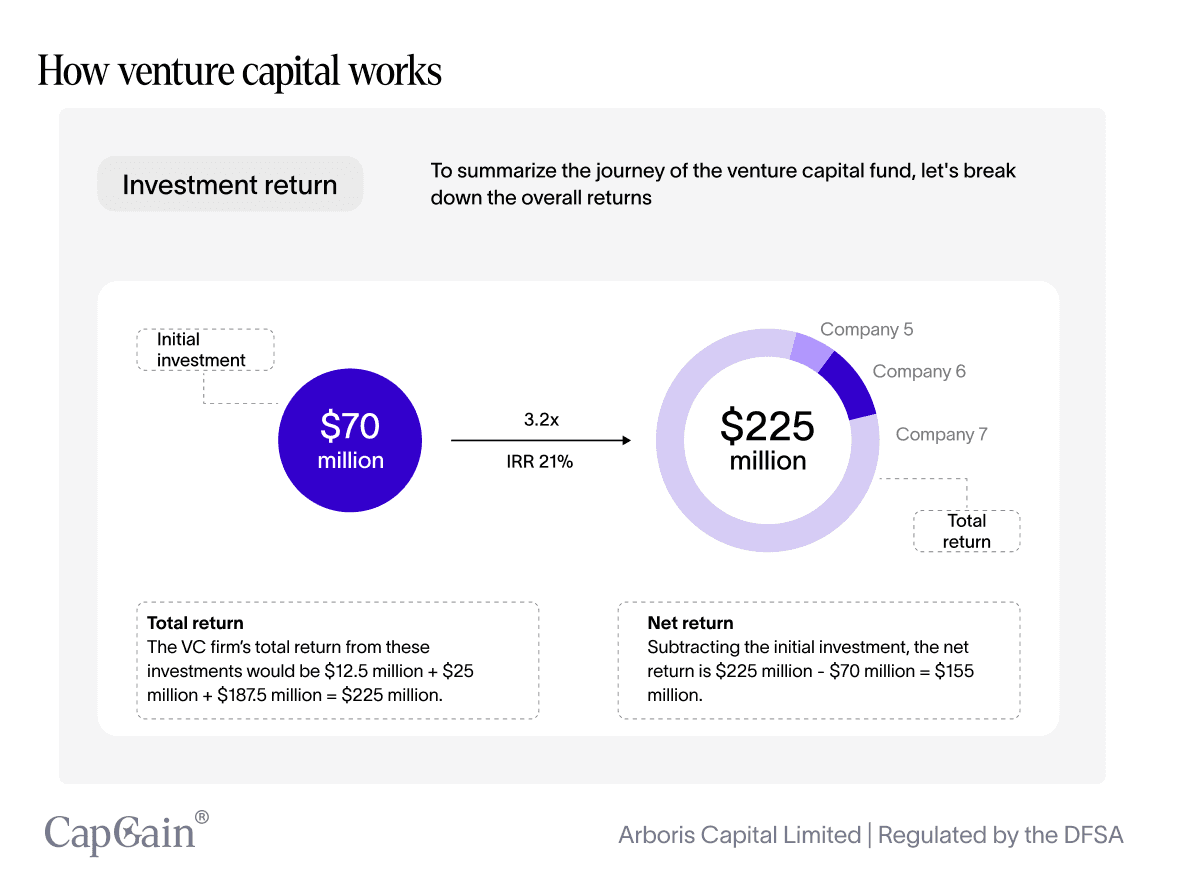

Investment returns

When tallying the results, here’s what the fund looks like:

Company 5 return: USD 12.5 million

Company 6 return: USD 25 million

Company 7 return: USD 187.5 million

Total return: USD 225 million

Subtracting the initial USD 70 million investment, the net return comes to USD 155 million. This equates to a 3.2x return with an internal rate of return (IRR) of 21%.

Final thoughts

The venture capital model thrives on calculated risk. Most start-ups fail, but the winners—especially unicorns—generate outsized returns that drive the entire portfolio.

For investors, VC offers access to innovation and exponential growth. For entrepreneurs, it provides not just capital but mentorship, networks, and guidance critical to scaling. And for the broader economy, venture capital plays a pivotal role in funding the ideas that shape tomorrow’s industries.

This guide is a high-level explanation of a much more nuanced reality. Venture capital, in practice, is shaped as much by timing, power dynamics, and narrative as it is by numbers and models. If you want to go deeper—into how deals are actually structured, how returns are really generated, and where the risks quietly compound—our Private Markets Masterclass unpacks it in full.

Pitchbok, Global Private Market Fundraising Report Summary Q3 2024, Accessed October 14 2025

Preqin database, Accessed October 14 2025

Written by

Sarah Hansen

Head of Research

Disclaimer – For Professional Clients Only

This communication is intended solely for persons classified as Professional Clients as defined by the Dubai Financial Services Authority (DFSA). It is not directed at Retail Clients and should not be relied upon by any person who does not meet the criteria for classification as a Professional Client. The information provided herein is for general informational purposes only and does not constitute, and should not be construed as, an offer, solicitation, invitation, or recommendation to buy, sell, or otherwise transact in any investment product or to engage in any investment strategy.

The subject matter discussed does not relate to a DFSA-regulated financial product or service. The content is intended only to provide a general update on market conditions and does not consider the specific investment objectives, financial situation, or particular needs of any recipient. It should not be relied upon as the basis for any investment decision. Past performance is not a reliable indicator of future performance. The value of investments and any income from them may fluctuate, and there is no assurance that the original capital will be preserved or returned.

Although the information contained in this communication has been obtained from sources believed to be reliable, Arboris Capital Limited makes no representation or warranty as to its accuracy, completeness, or fitness for any particular purpose. No liability is accepted by Arboris Capital Limited, its employees, or affiliates for any direct or consequential loss arising from the use of or reliance on this material. Arboris Capital Limited is authorised and regulated by the Dubai Financial Services Authority (DFSA) and operates within the Dubai International Financial Centre (DIFC), United Arab Emirates.