Private equity has consistently outperformed public markets across cycles, rate environments, and time horizons — driven not by sentiment, but by active ownership and operational transformation. It opens access to the vast majority of the economy that public markets don't reach, and when sized appropriately, improves a portfolio's returns, resilience, and risk-adjusted outcomes. Patience, here, is genuinely rewarded.

Private equity has historically outperformed public equities across all major time horizons — by an average of 455 basis points annually over 25 years

This outperformance holds across interest rate environments and public market cycles, including during bear markets

Returns are driven by active value creation — strategic, operational, and governance improvements — not market sentiment

PE firms source deals through proprietary networks, giving them earlier access and less competition than public market investors

Direct negotiation means PE firms typically acquire companies at a meaningful discount to equivalent public market valuations

87% of US and 96% of European companies with revenues over USD 100 million annually are privately held — public portfolios miss most of the real economy

Adding a 30% PE allocation to a 70/30 portfolio increases projected returns, improves the Sharpe ratio, and raises the probability of meeting long-term return targets

Illiquidity is a feature as much as a risk — investors are compensated for it through the illiquidity premium

Private equity is everywhere. Since its inception, private equity has played a vital role in not just the financial markets but the economy at large. As a provider of crucial capital for expansion, operational improvements, and strategic initiatives, private equity is often considered a catalyst for innovation, economic growth, and, ultimately, job creation.

It has facilitated innovation across a wide spectrum of areas of the economy, from niche sectors such as biotech to industries that we encounter in our daily lives, like dentistry, logistics or even poultry (and of course a wealth of vegan alternatives).

From exclusivity to access

While private equity is present in every aspect of daily life, it is perhaps best known for its exclusivity. Historically, private equity investments were only accessible to institutional investors or high-net-worth individuals. The reasons behind this were threefold.

High minimums: Investments often started at USD 5–10 million

Long lock-ups: Capital was committed for 7–10 years

Opaque access: Opportunities weren’t publicly listed

However, as the industry continues to evolve, private equity has become far more accessible and attractive to retail investors. Platforms such as CapGain now enable access to private market investments with lower ticket sizes, making capital investment more feasible for novice investors.

Today, platforms like CapGain are changing that. Through structured feeder vehicles, evergreens, and secondaries, investors can now:

Enter at lower ticket sizes

Access professional-grade funds

Gain exposure to investment structure with more flexible holding periods

Why invest in private equity?

With private equity becoming more broadly accessible, one question remains: are they a good investment? And are they right for you? In the next sections, we take a look at some of the compelling reasons why private equity might deserve a place in your portfolio.

Patience pays: The illiquidity premium

First things first: Private equity is a long-term and illiquid investment, meaning it locks up capital for an extended period of time with no secondary market.

That being said. Patience pays.

Because investors give up immediate access to their money, they’re compensated with the potential for higher returns. Think of it as a reward for waiting. In financial terms, this is called the illiquidity premium, the excess return investors demand for tying up their capital in assets that can’t be quickly sold or traded.

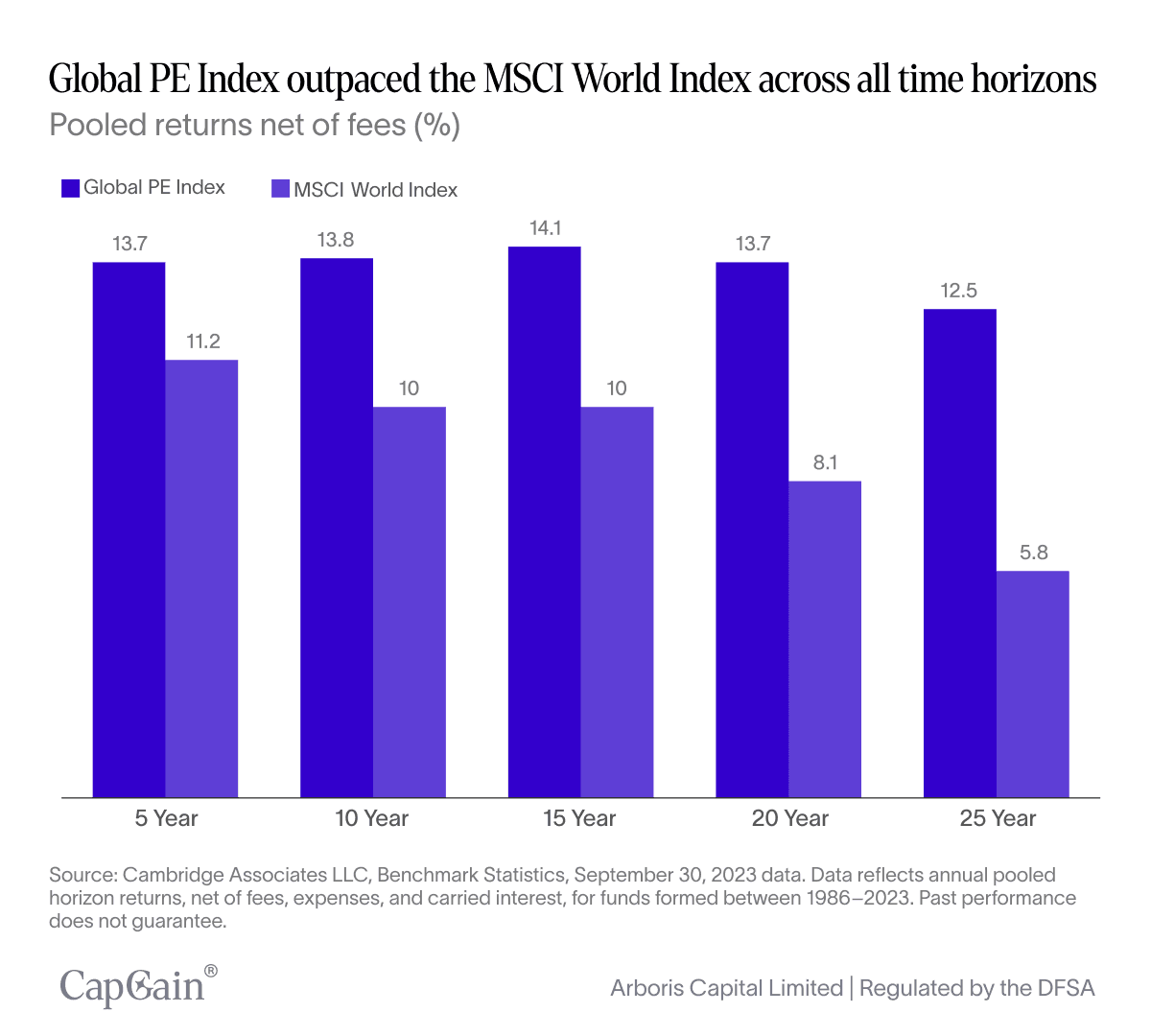

And historically, that premium has delivered: across all major time horizons, private equity has outperformed public equities.

Across all major time horizons, private equity has outperformed public equities. Over a 25-year period, the Global PE Index outpaced the MSCI World Index by an average of 455 basis points annually, according to Cambridge Associates (data as of September 30, 2023). Even at the 5-year mark, the gap remains meaningful — a testament to the compounding power of long-hold, actively managed strategies.¹

The longer holding periods allow fund managers to implement substantial operational changes, drive long-term strategy, and ride out market cycles without being held hostage to short-term sentiment.

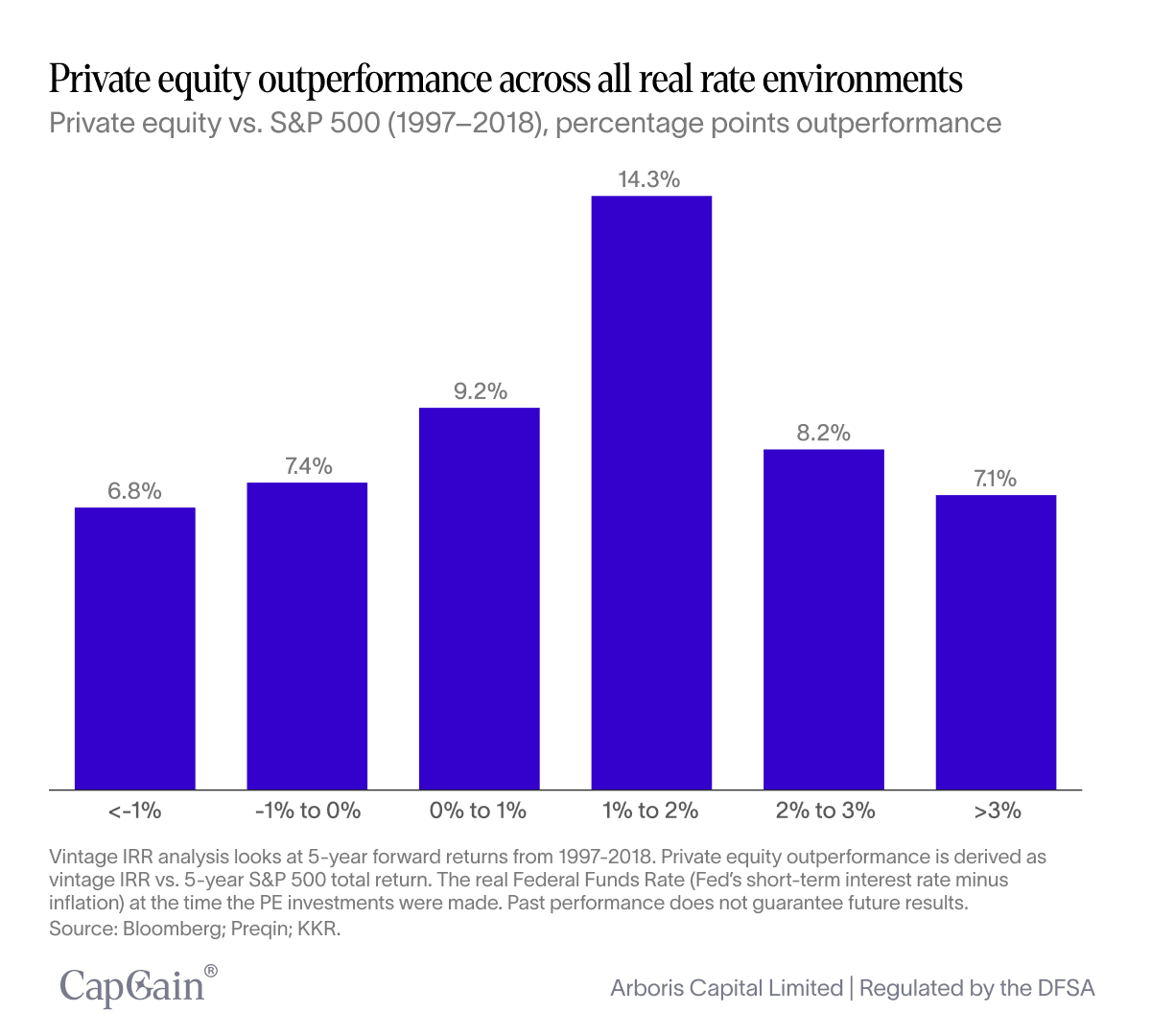

Resilience in all rate regimes

Private equity’s outperformance isn’t confined to a single market cycle. Data spanning more than four decades shows that the asset class has delivered strong relative returns across a range of real interest rate environments.

According to research from KKR, private equity vintages launched in periods of moderate real rates (0–2%) — including where we stand today — have historically delivered the highest excess returns over public markets. But even in high-rate or near-zero-rate environments, performance remained consistently above public benchmarks.²

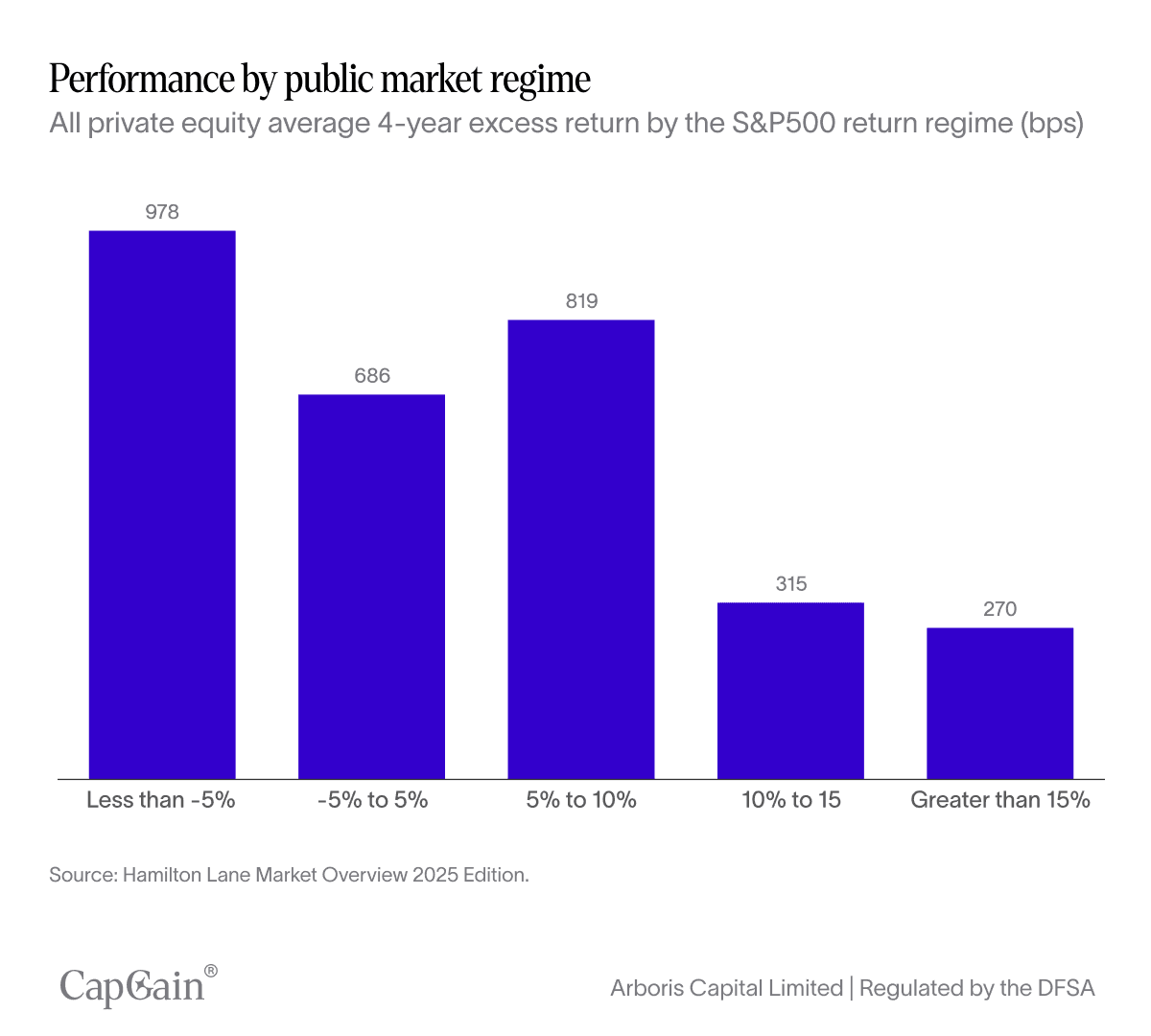

Private equity outperforms across public market cycles

Private equity’s ability to generate alpha is not confined to a specific phase of the public market cycle. When the S&P 500 delivered less than 5% annualised returns, private equity’s excess performance widened significantly, reaching +978 basis points in negative-return markets and +686 basis points when public returns were between 5% and 5%. Even during bull runs where the S&P 500 returned over 15% annually, private equity still posted positive relative gains — a testament to its role as a return enhancer across varying market climates.³

How does private equity outperform its public peers?

This persistence speaks to private equity’s underlying drivers of value creation — strategic control, operational transformation, and disciplined capital deployment — which operate largely independent of short-term monetary conditions.

In other words, while public markets are at the whim of central bank policy and stock market movements, PE managers tend to work on multi-year timeframes where the impact of stock markets and rates can be mitigated strategically.

Value creation: The growth engine

While the exact reason for this outperformance is unique to each investment case, there are some key aspects that influence this performance:

Strategic overhaul: Refocus core business, enter new markets, or divest non-core assets to channel resources into the highest-growth areas.

Operational improvements: Boost efficiency through best practices, new tech, and process optimisation to cut costs and raise productivity.

Governance & Leadership: Strengthen boards, refresh management teams, and align incentives with long-term performance goals.

Growth via acquisitions: Expand market share or product lines through strategic M&A, unlocking synergies and scale benefits.

‘Network is net worth’

Starting with deal sourcing, Private Equity (PE) has a distinctive advantage in identifying, accessing, and capitalising on undervalued assets. This is partly due to their comprehensive experience in the field. The average PE firm will have decades, if not centuries, of experience and expertise spanning various sectors, stages and regions. As a result, they are incredibly apt at identifying growth opportunities.

In addition to in-house expertise, private equity firms also have an immense advantage in the form of external expertise and relations. Connections are often considered a core asset for PE firms, which dedicate significant resources to building and maintaining extensive networks of industry contacts, advisors, consultants, and investment bankers.

These relationships provide PE firms with early or exclusive access to investment opportunities that are not widely marketed or known to the public. This means less competition and the opportunity to negotiate directly with the company.

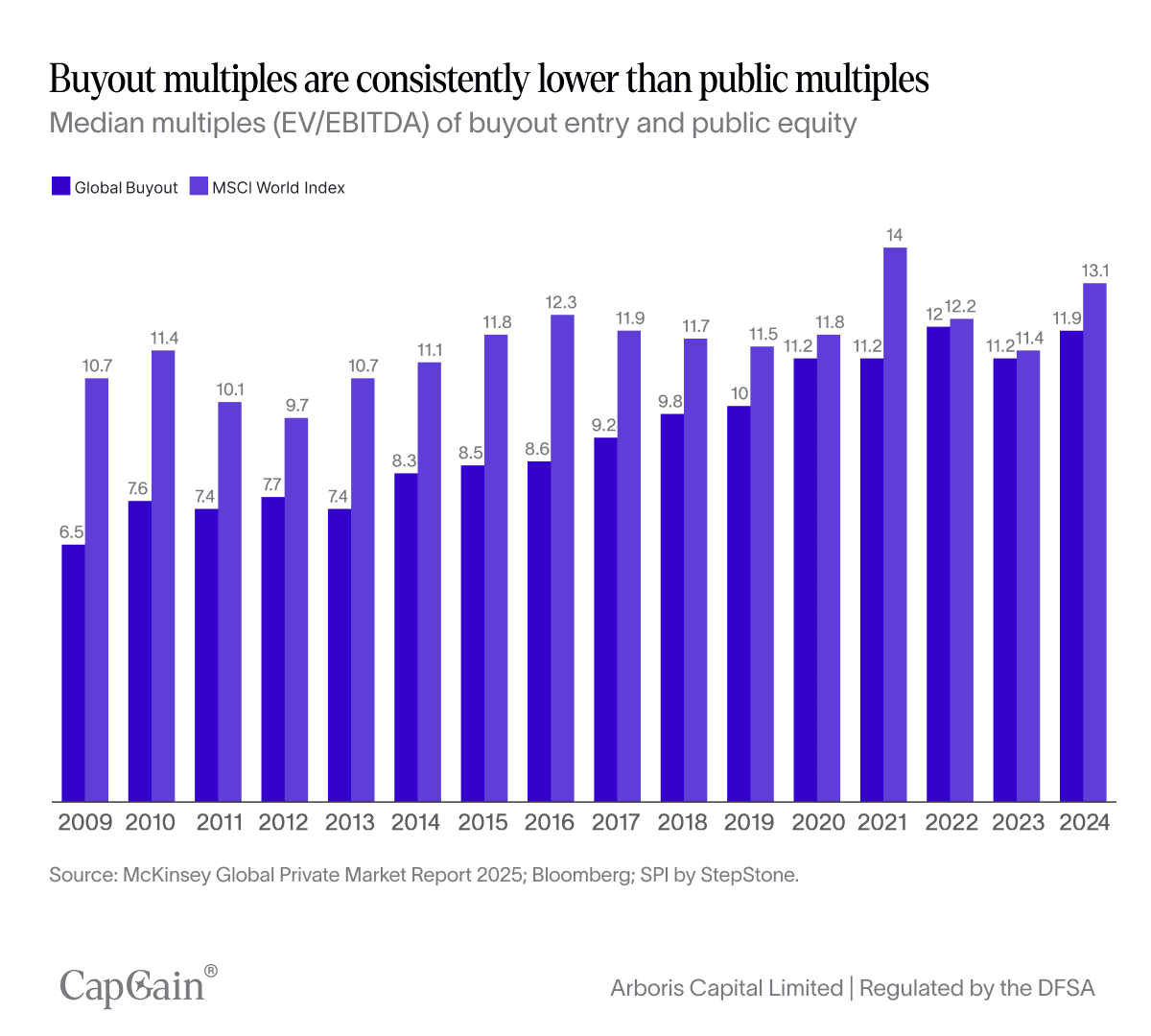

Direct negotiation enables favourable deal terms

Which leads us to the next point: deal negotiation. Being able to negotiate directly with the target company is another key advantage of private equity.

Public market investments are often the by-product of competitive and public bidding processes. As a result, they are often influenced by market sentiment rather than sensibility. In a PE investment, on the other hand, each transaction involves direct negotiations with company owners or stakeholders.

Before committing capital, PE firms rigorously analyse their investment prospects based on direct and exclusive access to the company’s records, such as financial statements, customer data, and supplier agreements.

This proprietary access allows PE firms to conduct thorough due diligence and negotiate favourable terms. As a result, PE firms generally acquire private companies at significantly lower prices than their public counterparts. According to McKinsey’s Global Private Markets Review 2025, global buyouts have consistently entered at a discount to public equity valuations, with median entry multiples (EV/EBITDA) averaging 1–4 turns lower than the MSCI World Index over the past 15 years — a pricing edge driven by proprietary access, targeted sourcing, and direct negotiation.⁴

Private equity in the portfolio

Insofar, we’ve discussed private equity in general — its performance, resilience, and value-creation advantages. In this section, we examine private equity’s role within a broader portfolio — moving beyond its general performance, resilience, and value-creation advantages to assess how it can expand exposure, enhance diversification, and strengthen risk-return dynamics.

Diversification beyond the public markets

The first key benefit is diversification. With most companies operating outside public markets, private equity offers access to a much broader slice of the global economy. According to Hamilton Lane and S&P Capital IQ, 87%⁵ of US companies and 96%⁶ of European companies with revenues exceeding USD 100 million remain privately held.

Public equity portfolios, by definition, miss the vast majority of potential growth opportunities — meaning that without PE exposure, investors are structurally under-invested in the real economy’s growth engine.

De-correlation: The quiet contributor to resilience

While precise correlation figures vary by strategy, geography, and market cycle, private equity has historically shown lower correlation to public equities than public market segments do to each other.

This is partly structural — valuations are marked less frequently, driven more by operational performance than by daily market sentiment. As a result, private equity returns tend to be less sensitive to short-term public market swings, which can help smooth portfolio volatility over time.

That said, correlation is not zero — PE is still exposed to macroeconomic forces — but its differentiated drivers of value creation mean it can act as a complementary return stream rather than a simple extension of public market beta.

Beyond diversification

Of course, diversification for the sake of diversification is frivolous.

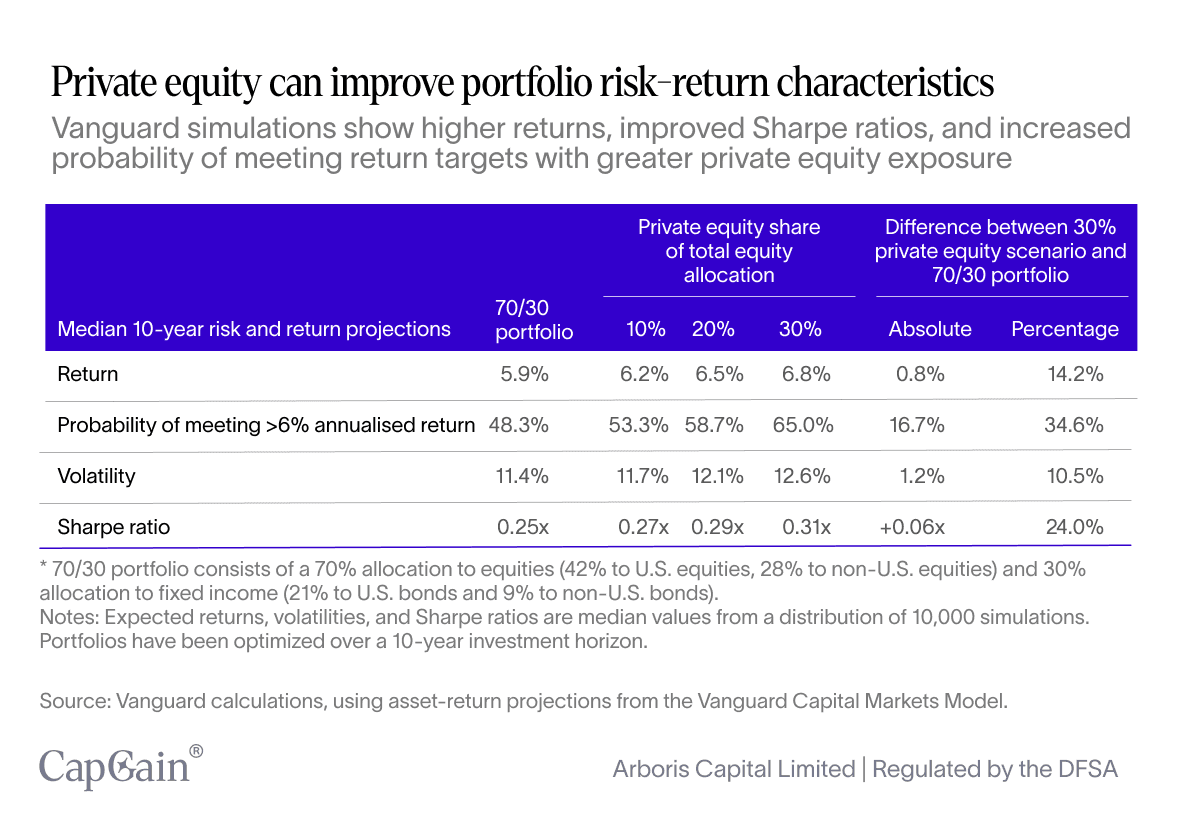

Diversification in itself is not a virtue. The real question is whether an allocation improves the overall portfolio on a risk-adjusted basis. Again, the data is compelling. Vanguard simulations show that adding private equity to a traditional 70/30 equity-bond portfolio meaningfully enhances performance:

Return: Increases from 5.90% to 6.80% with a 30% PE equity allocation (+14.2%)⁷

Probability of meeting >6% annualised return: Rises from 48.3% to 65% (+34.6%)⁷

Sharpe ratio: Improves from 0.25x to 0.31x (+24%)⁷

In other words, beyond its role as a return enhancer, PE can act as a portfolio stabiliser — widening opportunity sets while improving the odds of meeting long-term return targets.

Final thoughts

Private equity is no longer just the preserve of large institutions and ultra–high-net-worth investors. It has proven its ability to outperform public markets across cycles, navigate varying rate environments, and create value through strategic, operational, and governance levers that public companies often can’t match.

As access broadens, its role within a diversified portfolio becomes clearer: it opens the door to parts of the economy public markets don’t reach, offers differentiated return drivers with lower public equity correlation, and — when sized appropriately — can improve the portfolio’s overall risk-return profile.

For investors with the right time horizon, risk tolerance, and liquidity profile, private equity is not simply an “alternative” — it’s a core component of modern portfolio construction. The key is disciplined manager selection, thoughtful allocation, and a clear understanding of how it fits into long-term objectives.

Sources:

KKR, Staying on Course in Private Equity, April 2025, Accessed August 13 2025 https://www.kkr.com/insights/private-equity-staying-on-course

KKR Insights Global Macro Trends, An Alternative Perspective: Past, Present, Future, September 2024. Accessed August 14 2025. https://www.kkr.com/content/dam/kkr/insights/pdf/2024-september-an-alternative-perspective.pdf

Hamilton Lane, Market Overview 2025, March 12 2025, Accessed August 13 2025, https://www.hamiltonlane.com/en-us/insight/2025-market-overview

Mckinsey, Global Private Market Report 2025, Accessed August 14 2025. https://www.mckinsey.com/industries/private-capital/our-insights/global-private-markets-report

Hamilton Lane Private Wealth, Private Market Investing: Staying Private Longer Leads to Opportunity, April 14 2022, Accessed July 18 2025. https://www.hamiltonlane.com/en-us/insight/staying-private-longer

Apollo Academy, Many More Private Firms in Europe, April 28 2025, Accessed July 18 2025, https://www.apolloacademy.com/many-more-private-firms-in-europe/

Vanguard, The diversification benefits of private equity - Private Equity Perspectives, October 2023, https://corporate.vanguard.com/content/dam/corp/research/pdf/vanguard_diversification_benefits_of_private_equity.pdf

Written by

Sarah Hansen

Head of Research

Disclaimer – For Professional Clients Only

This communication is intended solely for persons classified as Professional Clients as defined by the Dubai Financial Services Authority (DFSA). It is not directed at Retail Clients and should not be relied upon by any person who does not meet the criteria for classification as a Professional Client. The information provided herein is for general informational purposes only and does not constitute, and should not be construed as, an offer, solicitation, invitation, or recommendation to buy, sell, or otherwise transact in any investment product or to engage in any investment strategy.

The subject matter discussed does not relate to a DFSA-regulated financial product or service. The content is intended only to provide a general update on market conditions and does not consider the specific investment objectives, financial situation, or particular needs of any recipient. It should not be relied upon as the basis for any investment decision. Past performance is not a reliable indicator of future performance. The value of investments and any income from them may fluctuate, and there is no assurance that the original capital will be preserved or returned.

Although the information contained in this communication has been obtained from sources believed to be reliable, Arboris Capital Limited makes no representation or warranty as to its accuracy, completeness, or fitness for any particular purpose. No liability is accepted by Arboris Capital Limited, its employees, or affiliates for any direct or consequential loss arising from the use of or reliance on this material. Arboris Capital Limited is authorised and regulated by the Dubai Financial Services Authority (DFSA) and operates within the Dubai International Financial Centre (DIFC), United Arab Emirates.