This article provides a comprehensive beginner's guide to private equity, explaining what private equity firms are, how their investment funds work, and the various strategies they use—such as venture capital, buyouts, and secondaries. It also explores the broader industry ecosystem, including key stakeholders like limited partners, buyers, and regulators, as well as the many advisors and service providers who facilitate deals.

PE firms are key agents in private equity, managing all aspects from acquiring to managing companies.

Private equity funds are the vehicles.

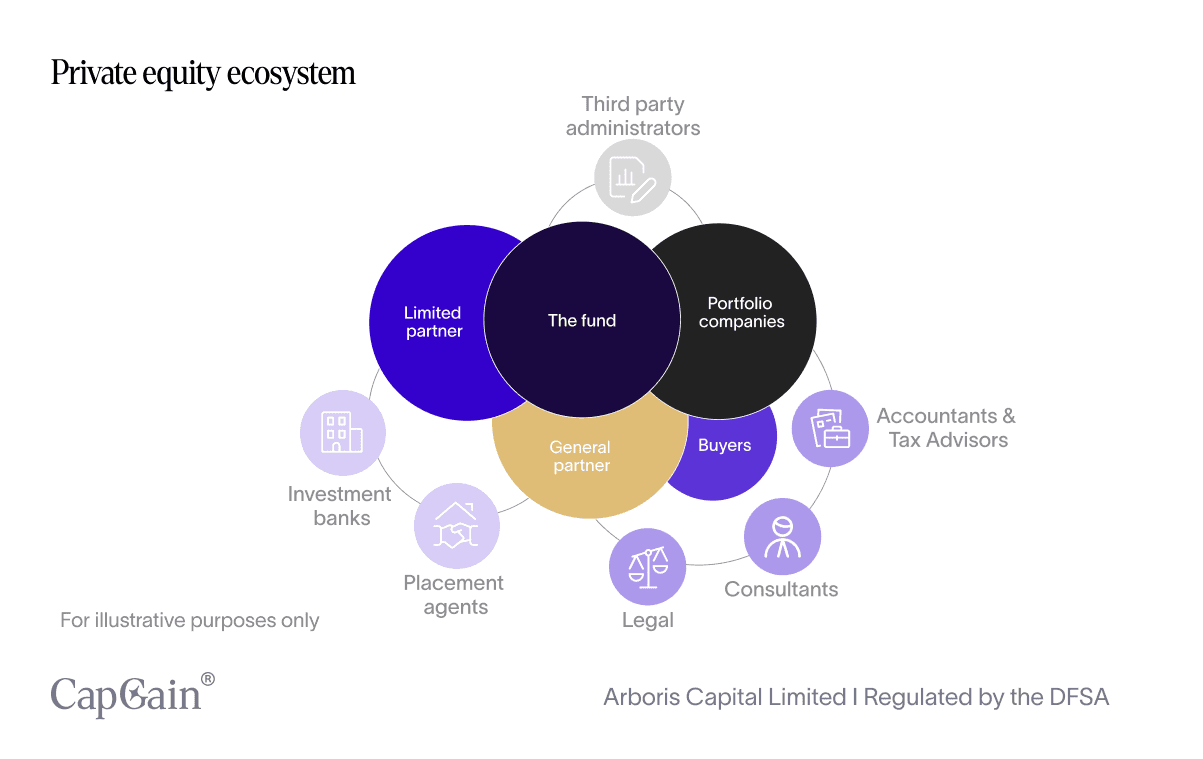

The private equity industry includes a network of financial advisors, legal and tax consultants, and investment banks, all critical for operational compliance and smooth transactions.

If you're new to alternative investments, you’ve probably noticed that the term 'private equity' is used in different contexts—from referring to the firms themselves to the funds, the strategies, or even the industry ecosystem. No wonder it’s hard to wrap your head around

Don’t worry. We get you, and we’ve got you. This brief guide provides a comprehensive overview of private equity, beginning with a who’s who of the industry and a definition of the term investment strategy.

What are private equity firms?

Let’s begin with the most common use of the term: the firms behind the deals.

Private equity firms—or PE firms—represent the investment managers who raise funds from investors to acquire and manage private companies.

The roles and responsibilities of the private equity firm are far-reaching, ranging from deal sourcing, due diligence, and deal-making to actively managing the portfolio companies from the day of investment until the eventual exit. Due to the multifaceted aspects of this endeavour, private equity firms are also known as ‘sponsors.’

Blackstone, KKR, and Carlyle Group are among the most well-known private equity firms. From their early inception until today, these firms have played instrumental roles in shaping the industry, setting precedents for both performance and practices.

The number of PE firms has steadily increased over the years, driven by the growing appeal of private equity as an asset class among institutional and individual investors. Estimates suggest that there are several thousand private equity firms operating worldwide. For instance, Prequin's data has indicated that there are over 8,000 private equity firms globally. These range from global giants managing hundreds of billions to small, specialist firms targeting specific sectors or geographies.

How private equity funds work

Next, we zoom in on the vehicles they use to deploy capital: the funds.

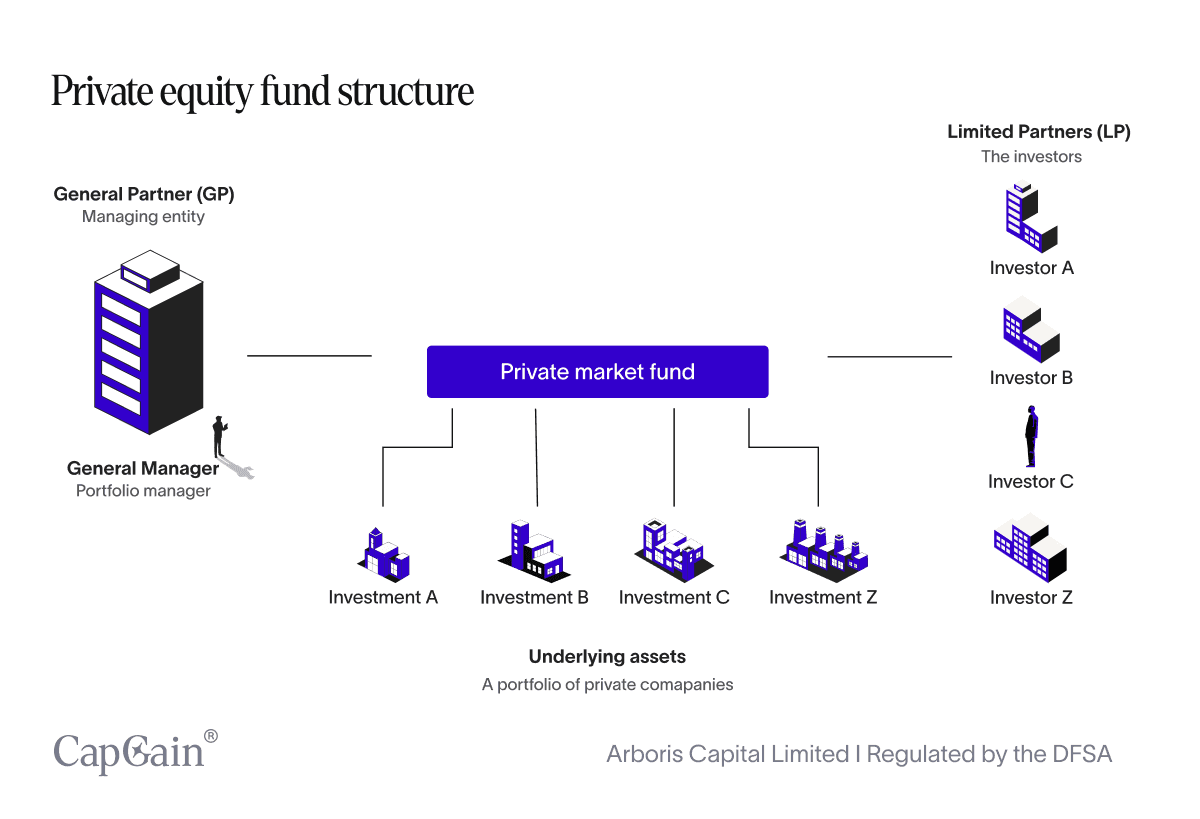

Before investing in companies, private equity firms pool capital from individuals or institutional investors (e.g., pension funds, endowments) and structure it into an investment vehicle, a process commonly referred to as fundraising.

The funds are typically structured as limited partnerships (LPs) or limited liability companies (LLCs). In this arrangement, the PE firm acts as the general partner (GP), assuming responsibility for managing the fund's investments and operations. For this reason, you’ll notice that private equity firms are sometimes referred to as general partners (GPs).

Private equity fundraising is termed 'closed-end,' meaning it involves raising a fixed amount of capital within a specific timeframe. Once the fundraising period concludes, the fund is closed to new investors. The capital raised is locked up while the private equity firm deploys it into investments over the fund's life, typically 10-12 years.

The capital that has yet to be invested is known as dry powder. This represents the capital available for investments. These investments are made by acquiring either the entire company, a controlling share, or a minority investment, depending on the fund’s strategy. E.g., venture capital acquires minority stakes in start-ups and scale-ups, and buyout usually buys controlling stakes in big companies.

Private equity investment strategies

Now let’s talk about what they actually invest in—and how strategies differ depending on stage, structure, or sector.

When discussing private equity, we often refer to the act of making private equity investments. That is, investing in a private company by acquiring the entire company, a controlling or a minority stake. In the simplest sense, private equity investments refer to investing in a company not listed on a public exchange. Of course, non-public is a broad term encompassing a wide range of companies across various sectors, scales, and, thus, differing financing needs.

To differentiate these investments, we distinguish private equity investments according to investment strategy. These strategies are often defined by the life cycle of the target companies, i.e., which stage of the business cycle they focus on:

Venture Capital (VC): Although often considered a distinct category, venture capital is a subset of private equity. It focuses on investing in startups and small businesses that are believed to have long-term growth potential.

Growth Capital: This refers to private equity investment, usually minority investments, in relatively mature companies looking for capital to expand or restructure operations, enter new markets, or finance a significant acquisition without a change of control of the business.

Leveraged Buyouts: This is perhaps the most widely recognised aspect of private equity. With this strategy, funds use a combination of equity and significant amounts of borrowed money to buy out companies, often aiming to improve operational efficiencies and sell them later at a profit. Often, you’ll see this type of investment referenced as LBOs or simply ‘buyouts.’

Distressed Investments: Some private equity firms specialise in investing in distressed or underperforming companies to turn them around by improving their operational efficiencies, financial structuring, or management.

Mezzanine Capital: This is a hybrid of debt and equity financing that gives the lender the right to convert to an equity interest in the company in case of default, generally after venture capital companies and other senior lenders are paid.

Beyond business stages: Strategy-led approaches

While many private equity strategies are defined by the life stage of the target company, others follow entirely different logics, focusing on diversification, liquidity management, or exposure to specific sectors or geographies instead.

Fund of funds

Fund of Funds is an example of an investment strategy that focuses on diversification. It involves investments in a fund that, in turn, invests in a portfolio of private equity funds. This allows investors to gain broad exposure to various fund strategies and geographies within the private equity sector.

Secondaries

Secondaries represent another type of private equity investment. This involves buying and selling pre-existing investor commitments from private equity and other alternative investment funds. Investors might sell their interests in the secondary market for various reasons, including the need for liquidity or rebalancing of their portfolios. Others may want to invest in secondaries to gain exposure to private equity investments later in the investment process. From this perspective, secondaries represent both a tool for liquidity management and diversification as well as their own investment strategy. For more information about secondaries, refer to our article about the basics of secondaries.

Finally, it’s important to note that a private equity firm often manages several funds. While the funds can have the same strategies, it is not uncommon for each fund to have its own distinct strategy. Moreover, some funds invest in a range of different strategies within the fund.

Who else is involved? The industry network

Lastly, you’ll sometimes hear PE mentioned when talking about the industry as a whole. Depending on the context, this might refer to the key players or be a general reference to the entire ecosystem, including all stakeholders and service providers. No wonder it is easy to lose track of what we’re talking about.

Key stakeholders: LPs, buyers, and regulators

Limited Partners

Among the most important in this context are the investors, also known as the limited partners or LPs. The LPs are the PE fund's primary capital source. They include institutional investors (such as pension funds, insurance companies, and endowments), sovereign wealth funds, and high-net-worth individuals. Unlike the private equity firms (or general partners) that manage the fund, the limited partners are not involved in managing the fund or the underlying portfolio companies. The word limited refers to their limited legal responsibilities.

Buyers

Equally important are the buyers, i.e., the legal entities that acquire the portfolio companies at the end of the fund cycle. Buyers of private equity-owned or backed firms typically fall into several categories, each with its strategic objectives and investment rationales. The landscape of buyers reflects the diverse nature of private equity transactions and the varied strategic goals these entities pursue.

Strategic Buyers/Corporates: These companies are often the most common buyers in private equity exits. They acquire businesses to enhance their strategic objectives, such as expanding product lines, entering new markets, achieving synergies, or consolidating their position within the industry. For strategic buyers, the acquisition is typically a long-term investment integrated into their broader business operations. Other Private

Equity Firms: Secondary buyouts have become a prevalent exit route, where another private equity firm buys the company. This can happen for various reasons, such as the new firm's belief in its ability to add further value, a different investment strategy, or a longer investment horizon. Secondary buyouts are attractive for private equity sellers as they can often be executed more swiftly than other exit routes, given the buyer's familiarity with the private equity transaction process.

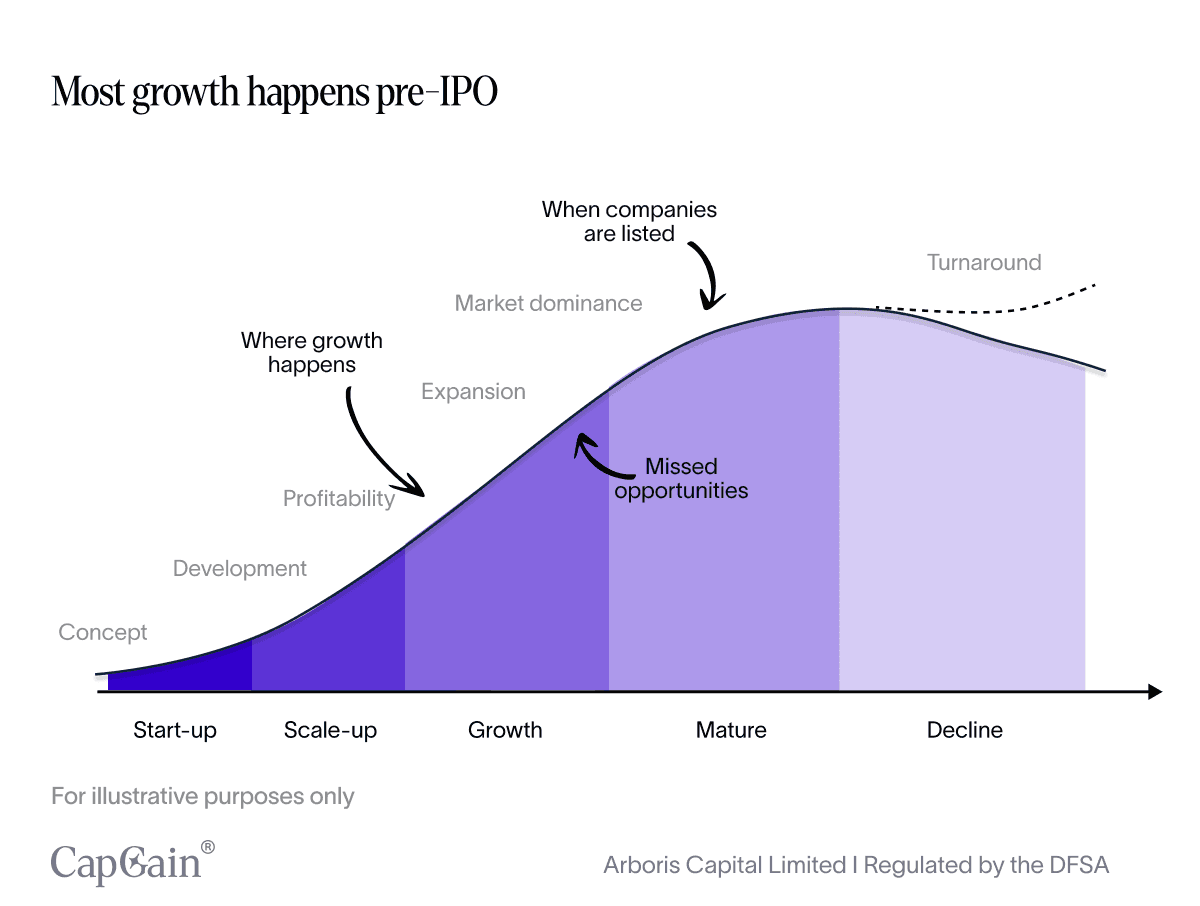

Public Markets (via IPOs): While not a direct buyer in the traditional sense, conducting an Initial Public Offering (IPO) is a significant exit strategy for private equity firms. In an IPO, the firm's shares are offered to the public, allowing the private equity owner to sell its stake partially or entirely over time in the public market.

Management Buyouts (MBOs): In this scenario, the company's existing management team buys the business, often with the financial backing of other investors or lenders. MBOs are attractive to private equity sellers when the management team has a solid plan for the company's future and is best placed to lead it forward.

Regulatory bodies

Last but not least, there are the regulatory authorities. The regulatory landscape for private equity firms varies by jurisdiction, with each country or region having its own set of regulatory authorities overseeing the industry.

Regulatory authorities impose various compliance requirements on private equity firms, such as registration, disclosure, and reporting obligations. These regulations aim to ensure transparency and protect the interests of both investors and consumers.

Meet the facilitators behind the deals

In addition to the industry, there are facilitators and service providers who help the private equity firm with various aspects of deal sourcing, screening, and management. While they are adjacent to the ecosystem, understanding who is who can be helpful for your general understanding.

Financial Advisors and Consultants: Offer strategic advice on acquisitions, divestitures, and capital raising. Consultants may also provide industry insights and operational improvements and help integrate ESG factors into business strategies.

Legal Advisors: Specialise in structuring transactions, ensuring regulatory compliance, and advising on legal matters related to deal negotiations, fund formation, and exit strategies. Mitigate legal risks and facilitate smooth transaction executions by navigating complex regulatory landscapes across different jurisdictions.

Accountants and Tax Advisors: Provide auditing services, financial due diligence, tax structuring, and compliance services. They play a critical role in financial reporting and tax optimisation for PE firms and their portfolio companies. Moreover, they help maximise financial efficiency and ensure compliance with applicable tax laws and accounting standards.

Investment Banks: Assist in raising capital, finding acquisition targets or buyers, and advising on mergers and acquisitions (M&A) transactions. They offer access to a broad network of potential investors, buyers, and sellers, as well as expertise in structuring complex transactions. They may also underwrite securities in public offerings.

Placement Agents: Specialise in assisting PE firms in raising funds from institutional investors and high-net-worth individuals. They help market the fund, identify potential investors, and navigate the fundraising process. They expand the reach of PE firms to a broader investor base and streamline the capital-raising process.

Third-Party Administrators (TPAs): Provide fund administration services, including accounting, reporting, and compliance support. TPAs handle the operational back-office functions, allowing PE firms to focus on making and managing investments. Hence, their services ensure operational efficiency, financial reporting accuracy, and regulatory compliance.

Market Data and Research Providers: Supply valuable market data, research reports, and analytics that inform investment strategies, sector trends, and benchmarking analyses. While not directly engaged in private equity, they enhance decision-making with data-driven insights and industry benchmarks.

Final thoughts

Private equity is often spoken about as a single thing. In practice, it’s a layered system: firms, funds, strategies, buyers, regulators, and a supporting network that makes long-horizon investing possible.

Understanding who does what—and why—turns private equity from an abstract asset class into a legible investment framework. If you want to go further, our private equity masterclass series breaks each layer down step by step.

Written by

Sarah Hansen

Head of Research

Disclaimer – For Professional Clients Only

This communication is intended solely for persons classified as Professional Clients as defined by the Dubai Financial Services Authority (DFSA). It is not directed at Retail Clients and should not be relied upon by any person who does not meet the criteria for classification as a Professional Client. The information provided herein is for general informational purposes only and does not constitute, and should not be construed as, an offer, solicitation, invitation, or recommendation to buy, sell, or otherwise transact in any investment product or to engage in any investment strategy.

The subject matter discussed does not relate to a DFSA-regulated financial product or service. The content is intended only to provide a general update on market conditions and does not consider the specific investment objectives, financial situation, or particular needs of any recipient. It should not be relied upon as the basis for any investment decision. Past performance is not a reliable indicator of future performance. The value of investments and any income from them may fluctuate, and there is no assurance that the original capital will be preserved or returned.

Although the information contained in this communication has been obtained from sources believed to be reliable, Arboris Capital Limited makes no representation or warranty as to its accuracy, completeness, or fitness for any particular purpose. No liability is accepted by Arboris Capital Limited, its employees, or affiliates for any direct or consequential loss arising from the use of or reliance on this material. Arboris Capital Limited is authorised and regulated by the Dubai Financial Services Authority (DFSA) and operates within the Dubai International Financial Centre (DIFC), United Arab Emirates.