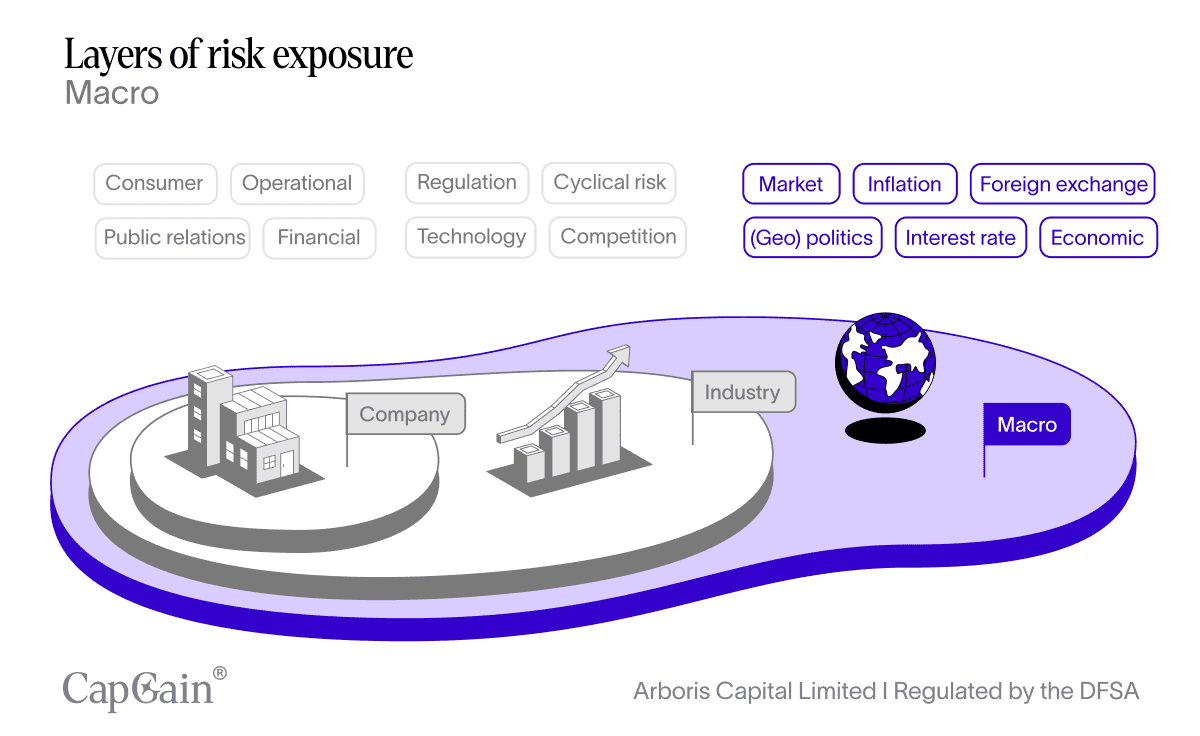

Macro-level risk reflects broad economic and systemic forces such as inflation, interest rates, currency movements, and geopolitical disruption. These factors shape the environment in which private equity investments are made and exited. Because private equity strategies involve long holding periods and limited liquidity, macro conditions can materially influence outcomes, requiring foresight, resilience, and disciplined execution across economic cycles.

Macro risk in private equity includes systemic shifts like inflation, interest rates, FX volatility, and geopolitical disruption.

Unlike public investors, PE firms can't reposition portfolios quickly — making macro foresight and resilience essential.

Strategic timing, active ownership, and deep thesis-driven conviction help top-tier firms navigate downturns.

Cyclical sectors and cross-border portfolios require even greater macro agility.

Case studies like Sensata and Hilton show that enduring value can be built — even in hostile environments — with the right thesis and timing.

Macro risk

When evaluating investment opportunities, analysing potential returns represents just one part of the equation. Another, equally crucial part, is the risk, i.e. the uncertainty relating to the investment case.

In Volatility, we explored risk from a purely mathematical perspective. In this series, we focus less on the algebra and more on the actual risk factors, examining the various levels and degrees of risk to which a company is exposed.

Risks in private equity can be broadly categorised across three levels:

Macro-level risk: Broad economic and systemic forces that impact entire markets — e.g., recessions, interest rates, FX, and geopolitical shifts.

Industry-level risk: Sector-specific trends and structural dynamics, such as regulatory changes or industry cycles.

Company-specific risk: Internal, firm-level challenges — from operational missteps to leadership failures.

In this piece, we examine how macro-level factors interact with private equity portfolios — and how firms adapt, absorb, and even capitalise on large-scale disruptions.

Economic downturns and their broad impact

Economic downturns have widespread implications for everyone in the economy. During such periods, consumer spending shrinks, most business activity stagnates, and market confidence erodes.

Private equity is not exempt from the ripple effects of broader economic contraction. Moreover, often the impact of economic downturns extends beyond the portfolio companies that private equity invests in — it also affects the private equity industry itself.

Portfolio companies: The individual businesses owned by private equity funds, which are directly affected by demand shifts, credit conditions, and operational pressures.

The private equity industry itself: The fund managers (GPs) and firms responsible for capital deployment, fundraising, and exits — all of which are influenced by macroeconomic conditions.

Portfolio companies

For individual portfolio companies, economic downturns and market fluctuations pose significant risks. Demand may drop sharply, supply chains can become disrupted, and access to capital may tighten — all of which can strain operations and compress margins.

Meanwhile, unlike public shareholders, private equity firms are not passive observers. Their long-term orientation and active ownership model equip them to respond strategically, stabilising companies, protecting value, and in many cases, positioning them for future growth.

Here’s how:

Implement strategic improvements: During economic downturns, private equity firms can leverage their expertise to enhance operational efficiencies within their portfolio companies.

Take advantage of lower valuations: Economic downturns often lead to lower market valuations. Private equity firms can capitalise on this by acquiring companies or assets at attractive prices.

Private equity industry

While portfolio companies feel the operational strain of a downturn, the private equity industry itself faces a different set of macroeconomic headwinds. These challenges affect the core mechanics of the PE model — from fundraising and deal sourcing to exits and capital deployment.

Raising funds: During economic downturns, it can be challenging for private equity firms to raise new funds. Investors, such as pension funds and endowments, may face financial constraints and become more cautious with their capital commitments.

Exiting positions: Economic downturns can make it difficult for private equity firms to exit their investments at favourable prices. With less overall economic activity and lower valuations, finding buyers willing to pay a premium becomes a challenge. This can delay the realisation of returns for investors.

Acquiring new companies: On the flip side, economic downturns can benefit private equity firms in terms of acquisitions. Reduced competition for deals during these periods allows firms to acquire companies at more attractive valuations and terms.

Cyclical risk

Cyclical industries experience periods of rapid growth during economic booms and significant downturns during recessions. For this reason, cyclical industries are often hit the hardest when the economy stagnates. Some examples of cyclical sectors include:

Automotive: The automotive industry is heavily influenced by consumer confidence and economic health. During recessions, car sales often decline as consumers delay major purchases.

Construction: Construction activity slows down during economic downturns due to reduced investment in infrastructure and real estate development.

Consumer Discretionary: During economic downturns, consumers often reduce their discretionary spending on items such as luxury items, entertainment, and leisure.

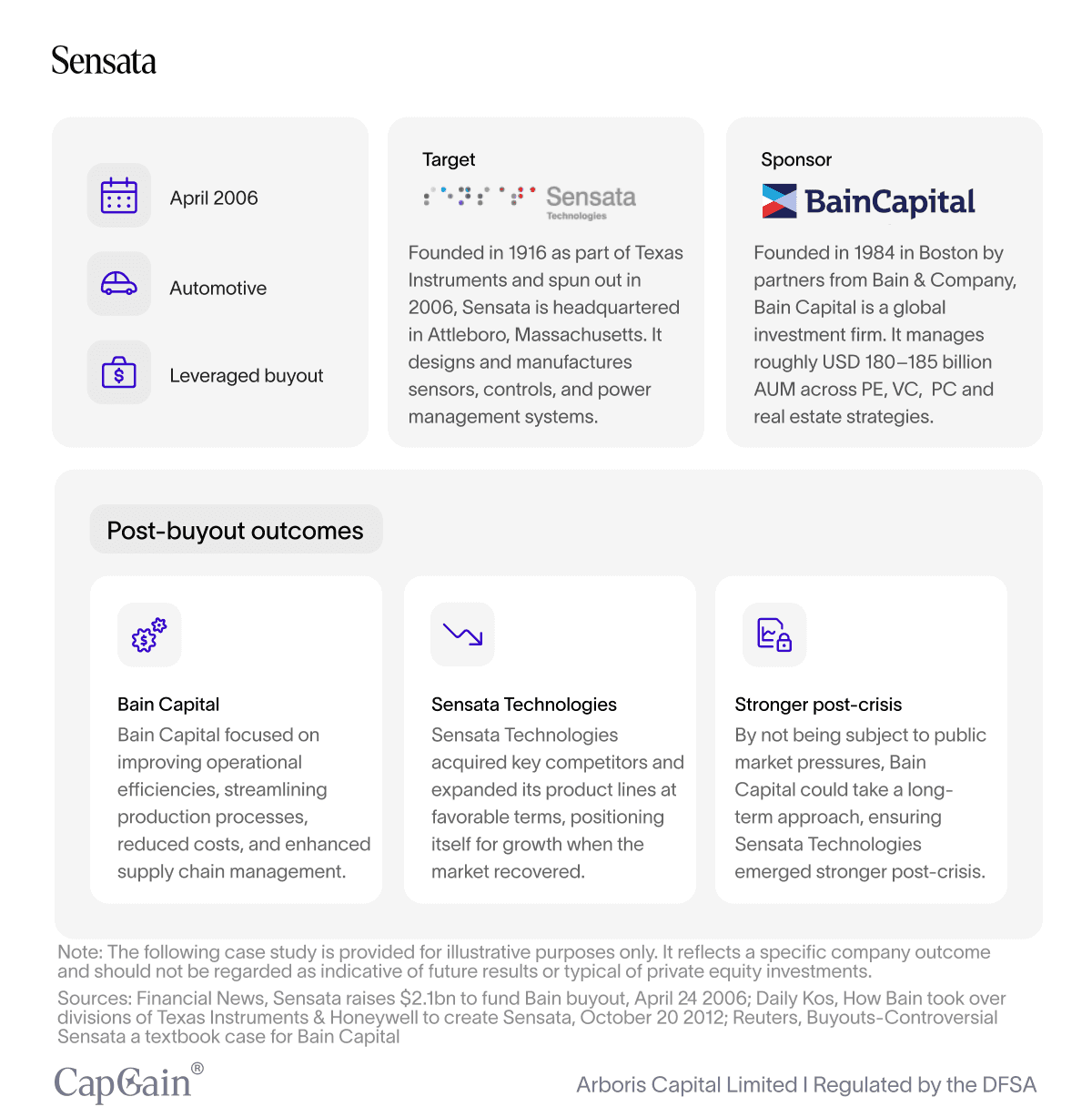

Case study: Sensata

Take the automotive industry, a highly cyclical sector. Sensata, was primarily focused on the development of sensors and controls for automotive, industrial, and aerospace markets.

By the early 2000s, Sensata was recognised as a leader in its field. And yet, the company faced challenges related to market saturation, intense competition, and the need for technological innovation to keep pace with rapidly changing industry demands.

In May 2006, Bain Capital, a prominent private equity firm, acquired Sensata from Texas Instruments for USD 3 billion, with an equity investment of USD 770 million ¹'²'³. This acquisition marked a significant shift in Sensata's trajectory, as Bain Capital sought to transform the company into a more agile and diversified player in the global market.

This transformation proved to be a trial by fire for both Bain Capital and Sensata. Less than two years after the deal closed, the Global Financial Crisis hit, and the automotive industry rapidly contracted.

Focusing on growth when the going gets tough

Despite the challenging macroeconomic environment, Bain Capital remained confident in its investment case. Having identified several long-term growth drivers, the company seized the opportunity to strengthen Sensata’s position in four key domains: safety, fuel efficiency, convenience and emissions.³

They chose not to be distracted by short-term turbulence and focused on the long haul, implementing various initiatives to elevate the business:

Expansion and diversification: Under Bain Capital's ownership, Sensata embarked on an aggressive expansion strategy. This included entering new markets and broadening its product portfolio. Bain supported Sensata in making several strategic acquisitions, such as the purchase of First Technology Automotive and Airpax Holdings. These acquisitions helped Sensata diversify its product offerings and gain access to new technologies and markets, particularly in Europe and Asia.

Operational efficiency: Private equity ownership also allowed Sensata to focus on operational efficiency. Bain Capital implemented various cost-cutting measures and streamlined operations to improve profitability.

Innovation and R&D: With the backing of private equity, Sensata significantly increased its investment in research and development. This investment was crucial in helping the company stay ahead of technological trends and meet the evolving needs of its customers.

In 2010, after successfully executing its transformation strategy, Bain Capital took Sensata public through an IPO at a USD 3.2 billion valuation³.

Sensatas case goes to show that with the right investment thesis, a company's performance can improve even if the macro environment is challenging. Seth Meisel, Managing Director at Bain Capital, stated:

"We retain our conviction that great deals can be done in most any environment and we are business as usual seeking out opportunities," Meisel said. "What I'm doing every day looking for themes and investment opportunities against those themes so even if the macro rains I hope to be smiling; and I hope we'll all be smiling."³

Interest rate sensitivity

Interest rate changes have a profound impact on private equity investments, especially within the buyout segment. Private equity firms often rely on debt to finance acquisitions, and fluctuations in interest rates can significantly impact the overall cost of debt servicing for the portfolio company.

Rising Interest Rates: When interest rates rise, the cost of borrowing also increases. This scenario squeezes the cash flows of portfolio companies, making it more challenging for them to service existing debt.

Impact on Valuations: Higher interest rates can also depress asset valuations. As the cost of capital increases, the discount rates applied to future cash flows rise, which can lead to lower present values and, consequently, lower valuations for private equity investments.

Refinancing Risks: Companies that need to refinance existing debt during periods of rising interest rates may face higher costs or stricter lending terms, which can impact their financial stability and operational flexibility.

Cross-border risk: Currency and geopolitics

For globally active portfolio companies, two key risks often go hand in hand: currency volatility and geopolitical disruption.

Currency fluctuations can distort earnings when revenues, costs, or financing are spread across multiple currencies. Even when the underlying business performance is strong, adverse exchange rate movements can reduce reported earnings or lower repatriated returns, particularly in emerging markets or during periods of monetary tightening.

Meanwhile, geopolitical risks — such as trade tensions, regulatory changes, or political instability — can disrupt supply chains, restrict market access, or introduce sudden compliance burdens. These challenges are especially acute for companies operating across multiple jurisdictions or in sectors exposed to government scrutiny.

Why private equity is uniquely equipped to address cross-border risk

Private equity is structurally well-positioned to manage cross-border risk. Unlike passive investors, PE firms take an active, hands-on role in governance and strategy. They can shift supply chains, restructure legal entities, or renegotiate contracts to mitigate exposure.

In addition, many firms actively monitor geopolitical developments and deploy hedging strategies to manage currency risk. Their ability to work behind the scenes — without the quarterly pressures of public markets — allows for strategic, multi-year responses to global volatility. The result: stronger resilience, faster adaptation, and, in many cases, a competitive edge during periods of uncertainty.

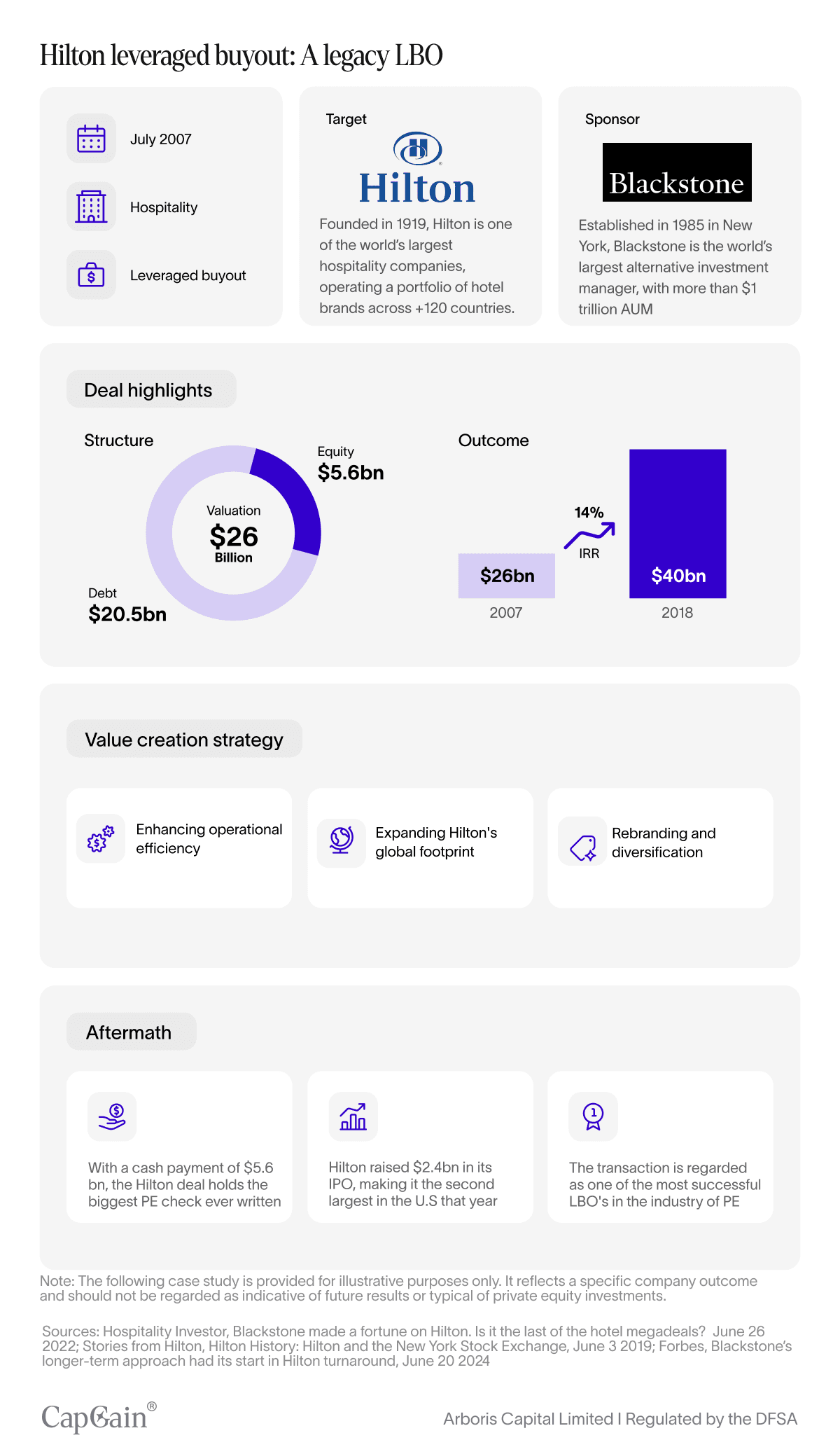

Case study: Blackstone & Hilton — Navigating the global financial crisis

Another prime example of how Private Equity managers can help navigate economic headwinds is none other than the legacy hotel brand, Hilton.

In 2007, Blackstone acquired Hilton Worldwide for approximately USD 26 billion, making it one of the largest leveraged buyouts in the hospitality sector.⁴

At the time, Hilton was a global brand with untapped potential: under-leveraged in international markets, fragmented across ownership models, and ripe for modernisation. Blackstone saw an opportunity to streamline operations, expand aggressively abroad, and unlock value through brand revitalisation and asset reallocation.

Textbook LBO turns into 'trial of fire'

But the plans were rapidly derailed; within a year, the global financial crisis hit, triggering a perfect storm of collapsing demand, plummeting valuations, and tightening credit markets.

The travel industry was among the hardest hit by the 2008 financial crisis. As consumer spending collapsed and corporate budgets froze, global travel demand plummeted. Airlines, hotels, and tour operators faced a sudden and severe contraction in revenues.

Hilton, as a global hotel chain with significant exposure to business and leisure travel, was particularly vulnerable. At the same time, the company’s debt-heavy balance sheet — a result of the leveraged buyout — meant it faced steep interest obligations just as cash flow dried up. Refinancing options evaporated in the post-Lehman credit freeze.

As pressures mounted, analysts questioned whether the acquisition would become a cautionary tale. But instead, it became a masterclass in crisis-era value creation. Blackstone doubled down:

Operational overhaul: Hilton slashed costs, modernised systems, and improved efficiency — without compromising guest experience.

Asset-light shift: The company pivoted to a franchise-heavy model, reducing capital intensity and improving cash flow.

Brand expansion: Even amid the downturn, Hilton launched new brands and strengthened its loyalty program, laying the groundwork for future growth.

By 2013, Hilton was ready for a comeback. Its IPO raised USD 2.35 billion⁵, and Blackstone’s disciplined stewardship ultimately turned a near-collapse into one of the most profitable private equity deals in history — generating over USD14 billion in gains.⁵

Following its IPO, Hilton continued to scale globally, underpinned by the foundational improvements implemented during Blackstone’s ownership. The shift to an asset-light model enabled faster expansion with lower risk, while digital upgrades and brand innovation kept the company competitive in a rapidly evolving travel landscape.

Final thoughts

Macro-level risks shape the operating environment for private equity just as they do for all investors. Inflation, interest rates, currency fluctuations, and geopolitical shifts influence portfolio companies and fund managers alike. Because private equity strategies typically involve longer holding periods and concentrated ownership, the effects of these forces may be more pronounced — both as challenges and as opportunities.

The experiences of Bain Capital with Sensata and Blackstone with Hilton highlight that, while downturns can pressure balance sheets, delay exits, and weigh on valuations, they can also provide room to implement operational improvements, pursue strategic expansion, and position companies for recovery once conditions stabilize. These examples illustrate what has been possible in specific contexts — but no two situations are alike, and outcomes depend on a range of variables unique to each deal and market environment.

When evaluating managers, it is therefore important to look not only at potential returns but also at how they assess and address macro-level risk through portfolio construction, deal structuring, and active ownership. Past performance provides useful insight but is not necessarily indicative of future results. What matters is the discipline of preparing for uncertainty, the ability to adapt when conditions shift, and the judgment to act when opportunity emerges.

Sources:

Financial News, Sensata raises $2.1bn to fund Bain buyout, April 24 2006. Accessed July 21 2025. https://www.fnlondon.com/amp/articles/sensata-raises-to-fund-bain-buyout-20060424

Daily Kos, How Bain took over divisions of Texas Instruments & Honeywell to create Sensata, October 20 2012, Accessed July 21 2025. https://www.dailykos.com/stories/2012/10/20/1147441/-How-Bain-bought-divisions-of-Texas-Instruments-Honeywell-to-create-Sensata

Reuters, Buyouts-Controversial Sensata a textbook case for Bain Capital, July 26 2012, Accessed July 21 2025. https://www.reuters.com/article/markets/buyouts-controversial-sensata-a-textbook-case-for-bain-capital-idUSL2E8IQ612/

Hospitality Investor, Blackstone made a fortune on Hilton. Is it the last of the hotel megadeals? June 26 2022, Accessed July 21 2025. https://www.hospitalityinvestor.com/investment/how-private-equity-giant-blackstone-became-real-estate-monolith#:~:text=In%20late%20December%202013%2C%20Blackstone,Blackstone%20bought%20the%20company%20for5. Stories from Hilton, Hilton History: Hilton and the New York Stock Exchange, June 3 2019, Accessed 21 July 2025. https://stories.hilton.com/hilton-history/hilton-and-the-new-york-stock-exchange

Forbes, Blackstone’s longer-term approach had its start in Hilton turnaround, June 20 2024, Accessed July 21 2025. https://www.forbes.com/sites/veronicairwin/2024/06/20/blackstones-longer-term-approach-had-its-start-in-hilton-turnaround/

Written by

Sarah Hansen

Head of Research

Disclaimer – For Professional Clients Only

This communication is intended solely for persons classified as Professional Clients as defined by the Dubai Financial Services Authority (DFSA). It is not directed at Retail Clients and should not be relied upon by any person who does not meet the criteria for classification as a Professional Client. The information provided herein is for general informational purposes only and does not constitute, and should not be construed as, an offer, solicitation, invitation, or recommendation to buy, sell, or otherwise transact in any investment product or to engage in any investment strategy.

The subject matter discussed does not relate to a DFSA-regulated financial product or service. The content is intended only to provide a general update on market conditions and does not consider the specific investment objectives, financial situation, or particular needs of any recipient. It should not be relied upon as the basis for any investment decision. Past performance is not a reliable indicator of future performance. The value of investments and any income from them may fluctuate, and there is no assurance that the original capital will be preserved or returned.

Although the information contained in this communication has been obtained from sources believed to be reliable, Arboris Capital Limited makes no representation or warranty as to its accuracy, completeness, or fitness for any particular purpose. No liability is accepted by Arboris Capital Limited, its employees, or affiliates for any direct or consequential loss arising from the use of or reliance on this material. Arboris Capital Limited is authorised and regulated by the Dubai Financial Services Authority (DFSA) and operates within the Dubai International Financial Centre (DIFC), United Arab Emirates.