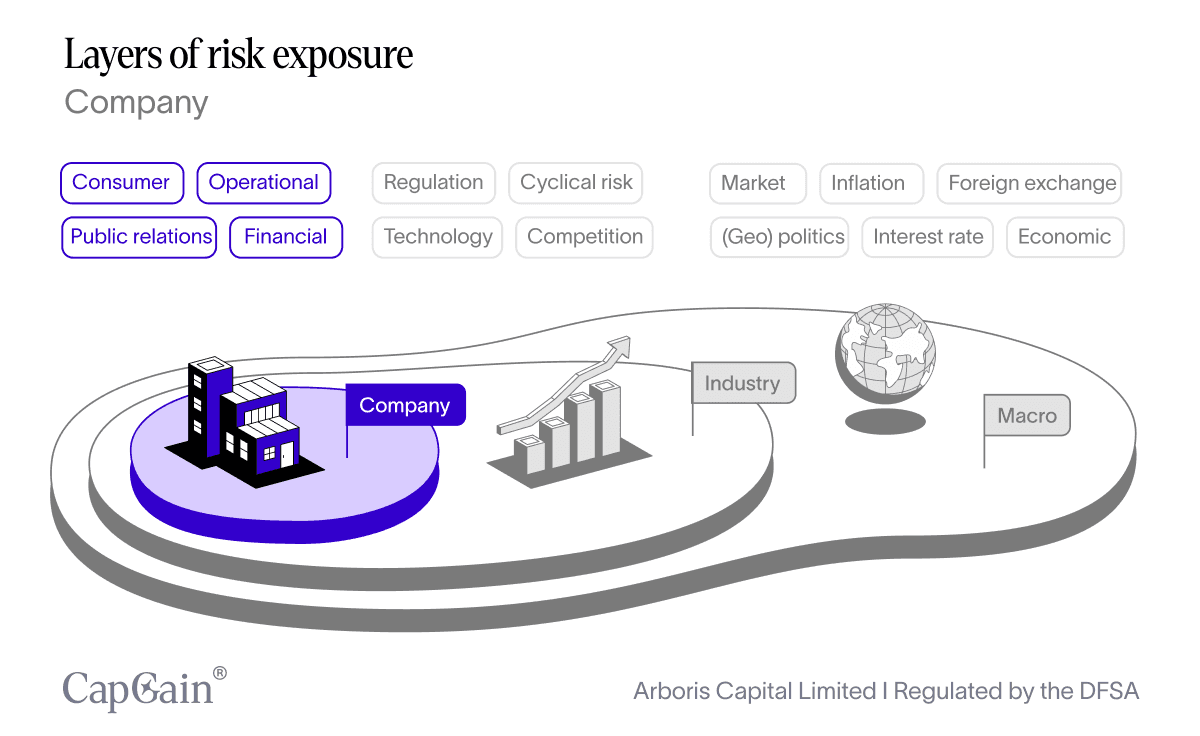

Company-level risk sits at the core of private equity outcomes. Unlike macro or industry forces, these risks are internal and execution-driven, spanning operations, strategy, leadership, and financial discipline. This article examines how private equity identifies, underwrites, and actively manages company-level risk through hands-on ownership, operational expertise, and governance influence, turning execution challenges into opportunities for value creation.

Company risk is the final and most execution-sensitive layer of risk in private equity.

PE firms mitigate these risks through rigorous diligence, placing concentrated bets only after deeply assessing fit, readiness, and alignment.

Once invested, they drive transformation from within—deploying value creation teams to overhaul operations, professionalise leadership, and sharpen strategy.

Macro trends set the stage. Industry dynamics shape the terrain. But at the end of the day, private equity returns are driven by what happens inside the company. This brings us to the last and final layer of risk in this series: company risk.

In this article, we explore company-level risk: what it is, and how it impacts the company. We’ll also dive into how private equity is uniquely positioned ot mitigate and manage these risks through active management.

What is company-level risk?

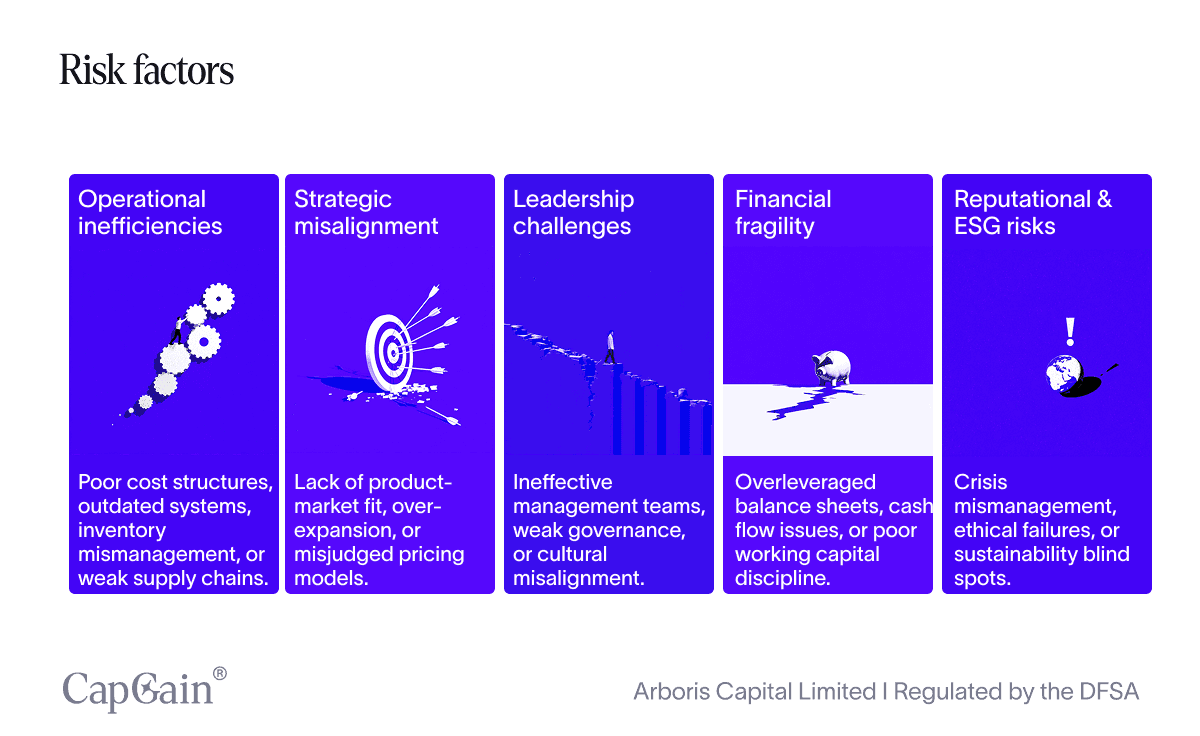

Company-level risk refers to the internal, operational, and execution-specific challenges that can make or break a portfolio investment, regardless of broader economic or industry conditions. Some of the most common include:

Operational inefficiencies: Poor cost structures, outdated systems, or weak supply chains.

Strategic misalignment: Lack of product-market fit, overexpansion, or misjudged pricing models.

Leadership challenges: Ineffective management teams, weak governance, or cultural misalignment.

Financial fragility: Overleveraged balance sheets, cash flow issues, or poor working capital discipline.

Reputational and ESG risks: Crisis mismanagement, ethical failures, or sustainability blind spots.

What’s key is that these risks are actionable. Unlike macro forces, which must be navigated, or sector shifts, which require adaptation, company-level risk is often a function of execution.

This is where private equity shines.

Sourcing as a strategic imperative

The first – and perhaps most crucial – risk mitigation measure starts before capital is even deployed: during the selection process.

While public investors can diversify away some of these risks across a portfolio of stocks, private equity firms place concentrated bets, often taking controlling stakes in just a few companies per fund. That means that investing in the right company is essential.

This is why due diligence is such a crucial aspect of private equity. During this process, the private equity firm analyses every aspect of the business, leaving no stone unturned. This includes risk factors.

For this reason, private equity and venture capital firms are extremely cautious with their placements. Only a select few make it through, and those who do will have undergone in-depth scrutiny beforehand.

The purpose of this exercise is not to scrutinise or criticise the target company. General Partners understand that risk exposure is an integral part of running a business.

As follows, their objective is not to find the perfect, risk-free investment. It is merely a matter of acknowledging these risks and ultimately deciding whether the manager is the right partner to help the target company navigate these risks on their path to prosperity.

The private equity playbook for company risk

Helping a portfolio company unlock its full potential while avoiding common pitfalls and pricey mistakes is a joint effort. Hence, once capital is deployed, PE firms work closely with management to diagnose pain points, implement best practices, and build resilience at the core.

Rather than relying solely on financial managers, the PE firm deploys specialised value creation teams to work alongside management. These teams comprise seasoned professionals from consulting, operations, finance, supply chain, and digital strategy.

Whether it’s optimising procurement, overhauling go-to-market strategies, upgrading IT systems, or improving unit economics, these teams bring a level of strategic and operational rigour that many founder-led or under-resourced companies have never had access to.

Operational transformation: PE firms are operationally hands-on

Many founder-led or family-owned businesses lack the operational backbone to scale efficiently. Private equity firms help their portfolio companies build that structure from the ground up, leveraging years of experience and tried-and-tested frameworks.

They deploy playbooks for everything from procurement and pricing to customer retention and digital enablement. Common initiatives include:

Benchmarking performance against industry leaders

Optimising working capital and supply chain flows

Introducing data systems, dashboards, and KPIs for real-time visibility

Leadership overhaul: PE firms identify management gaps

Great strategy fails without strong execution. And strong execution relies on excellent leadership. Recognising this, private equity firms often restructure the C-suite to ensure that the company has the necessary human capital to lead and succeed—and ultimately drive outcomes that align with investor goals.

Strategic repositioning

Sometimes a company’s issues stem not from how it executes, but what it’s executing. Private equity teams help reassess market focus, product mix, pricing models, and expansion plans.

These assessments often lead to a strategic restructuring, including:

Focusing on core profitable segments

Shedding or restructuring non-performing units

Reorienting toward scalable, high-margin growth

Case study: Apollo × Sun Country Airlines

Airlines are among the most execution-sensitive businesses in the economy: capital-intensive, cyclical, labour-heavy, and highly exposed to demand shocks. Thin margins, high fixed costs, and complex operating models mean that small execution missteps can quickly translate into material financial stress—particularly during periods of demand volatility or external disruption.

When Apollo acquired Sun Country Airlines in late 2017 (transaction closing in 2018), the company faced significant company-level risk, alongside broader macro and sector-specific headwinds. While the airline operated in a structurally challenging industry, many of the most pressing risks were internal and execution-driven.¹ Key challenges included:

Operational risk: aircraft utilisation, limited ancillary revenue capture, legacy booking and pricing systems.

Strategic risk: unclear positioning between legacy and ultra-low-cost carriers; heavy reliance on discretionary passenger demand.

Financial risk: high fixed costs, capital intensity, sensitivity to demand shocks.

Leadership and execution risk: operating model and governance not designed for rapid scaling or strategic pivots.

Upon acquisition, Apollo underwrote these risks on the basis that they were actionable under control ownership. Leveraging the expertise of their specialist team, they restructured Sun Country into a three-engine business model:

Scheduled leisure passenger flights (peak-optimised)¹

Charter services (including professional sports teams)¹

Cargo operations anchored by long-term partnerships¹

By diversifying beyond scheduled passenger travel into charter and cargo, Sun Country reduced exposure to demand volatility and improved year-round aircraft utilisation, providing cash-flow stability through economic downturns.

Operational transformation

More than USD 200 million invested in fleet, cabins, IT systems, and digital infrastructure¹

Implementation of modern booking and revenue-management systems¹

Ancillary revenue per scheduled passenger increased ~148% (2017–2019)²

Strategic shift toward greater fleet ownership to improve long-term unit economics

Leadership and governance

Professionalisation of management and governance structures²

Introduction of KPIs, dashboards, and data-driven decision-making²

Tighter execution discipline across pricing, scheduling, and cost control²

Outcomes (entry to exit)

Revenue: ~USD 560m → ~USD 1.1bn¹

Annual passengers: ~2.5m → ~4.5m¹

Headcount: ~1,800 → ~3,100+ (≈ +75%)¹

Ticket prices: declined ~40%, while revenues more than doubled²

Wages: reported to have more than doubled (sponsor-reported)³

COVID resilience: cargo and charter revenues supported cash flows during the pandemic¹

Exit: IPO in 2021, with strong investor demand reported at launch (including reports of ~13× oversubscription); full exit completed in early 2025 via staged sell-down.¹

Final thoughts

Sun Country illustrates that company-level risk is the most execution-sensitive layer of private equity risk. While macro conditions and industry dynamics shape the operating environment, outcomes ultimately depend on decisions made inside the company—across strategy, operations, leadership, and execution.

Execution risk is unavoidable. Even well-designed strategies encounter friction in practice. What differentiates private equity, however, is the ability of skilled managers to engage directly with these challenges through active ownership, operational expertise, and governance influence.

For investors, this underscores the critical importance of manager selection. Access to private equity alone does not mitigate company-level risk; the capability of the General Partner to identify, assess, and actively manage these risks does. Disciplined underwriting, operational depth, and a proven ability to execute transformation at the portfolio-company level are central to navigating execution risk.

Ultimately, success in private equity depends less on predicting markets and more on selecting managers with the experience, resources, and mandate to shape value from within companies over time.

Sources:

Apollo found a gap in the market to grow Sun Country Airlines, March 4 2025, Accessed December 23 205, https://www.apollo.com/content/dam/apolloaem/documents/insights/pe-hub-apollo-mar25.pdf

SEC IPO Prospectus, Sun Country Airlines Holdings, Inc. Registration No. 333-252858, Accessed December 23 205, https://www.sec.gov/Archives/edgar/data/1743907/000119312521085551/d71456d424b4.htm

The View From Apollo, Private Equity: Alpha in an Evolving Market, November 25 2025, Accessed December 23 205, https://www.apollo.com/institutional/insights-news/insights/the-view-from-apollo/2025/11/private-equity-alpha-in-an-evolving-market

Written by

Sarah Hansen

Head of Research

Disclaimer – For Professional Clients Only

This communication is intended solely for persons classified as Professional Clients as defined by the Dubai Financial Services Authority (DFSA). It is not directed at Retail Clients and should not be relied upon by any person who does not meet the criteria for classification as a Professional Client. The information provided herein is for general informational purposes only and does not constitute, and should not be construed as, an offer, solicitation, invitation, or recommendation to buy, sell, or otherwise transact in any investment product or to engage in any investment strategy.

The subject matter discussed does not relate to a DFSA-regulated financial product or service. The content is intended only to provide a general update on market conditions and does not consider the specific investment objectives, financial situation, or particular needs of any recipient. It should not be relied upon as the basis for any investment decision. Past performance is not a reliable indicator of future performance. The value of investments and any income from them may fluctuate, and there is no assurance that the original capital will be preserved or returned.

Although the information contained in this communication has been obtained from sources believed to be reliable, Arboris Capital Limited makes no representation or warranty as to its accuracy, completeness, or fitness for any particular purpose. No liability is accepted by Arboris Capital Limited, its employees, or affiliates for any direct or consequential loss arising from the use of or reliance on this material. Arboris Capital Limited is authorised and regulated by the Dubai Financial Services Authority (DFSA) and operates within the Dubai International Financial Centre (DIFC), United Arab Emirates.