Cash flow timing is a critical driver of investment returns. In investing, receiving money sooner is often more valuable than receiving the same amount later due to inflation, opportunity cost, and uncertainty. This principle, known as the time value of money, underpins key performance metrics such as present value and internal rate of return (IRR). This article explains how future cash flows are discounted into today’s value, illustrating how inflation and missed investment opportunities erode purchasing power over time.

Time Value of Money suggests that the value of money decreases over time due to inflation and the opportunity cost of not investing it sooner.

Inflation decreases the purchasing power of money, meaning the same amount will buy fewer goods or services in the future compared to today.

Money available now can earn returns (if invested in the right products), making it worth more in the future compared to receiving the same amount later.

The present value adjusts future cash flows to their equivalent value today, considering both inflation and opportunity costs.

Net Present Value (NPV) calculates the present worth of a series of future cash flows minus any initial investment, while Internal Rate of Return (IRR) is the discount rate that makes the NPV of all cash flows from a particular investment equal to zero.

Why cash flow timing matters

In our masterclass, we highlighted Internal Rate of Return (IRR) as one of the key performance metrics used to assess investments in both private and public markets.

Admittedly, this can be a tedious term, as it relies on some core concepts rarely discussed outside of economics. In fact, even with a background in finance, these topics can be hard to explain. But that is not going to stop us from trying! So, buckle up and embark on a journey... through time.

Because in investing, when you get paid is often just as important as how much. And to make sense of that, we need to start with a deceptively simple idea: a dollar today is worth more than a dollar tomorrow.

Time value of money: Why money is worth more today than tomorrow

First things first, to understand the internal rate of return – or IRR – we need to understand a fundamental economic principle: the time value of money (TVM).

The time value of money states that the value of money decreases over time. That is, USD100 today is worth more than USD100 received five years from now…

Why? Well, for one, the future is uncertain. There's always a risk associated with waiting to receive money, such as the risk of non-payment or other economic changes that could affect the value of the money. We cover risk and its impact on investments in great detail in the {{Dissecting Risk Series}}.

For now, let's focus on the time value of money.

In the context of TVM, there are two major considerations:

Inflation: Over time, prices tend to increase due to inflation. And inflation erodes the purchasing power of money. Imagine you go to the supermarket and buy USD 100’s worth of groceries today. Five years from now, that same basket will cost considerably more. That's inflation.

Opportunity cost: Money available today can be invested and potentially earn a return, leading to more money in the future. Thus, having USD 100 today enables you to invest and essentially grow that USD 100. Meanwhile, if you only receive the money a year from now, you could miss a year's worth of interest, provided that you’d picked the right investment.

These factors combined lead people to prefer receiving 'as soon as possible,' allowing for immediate consumption or investment.

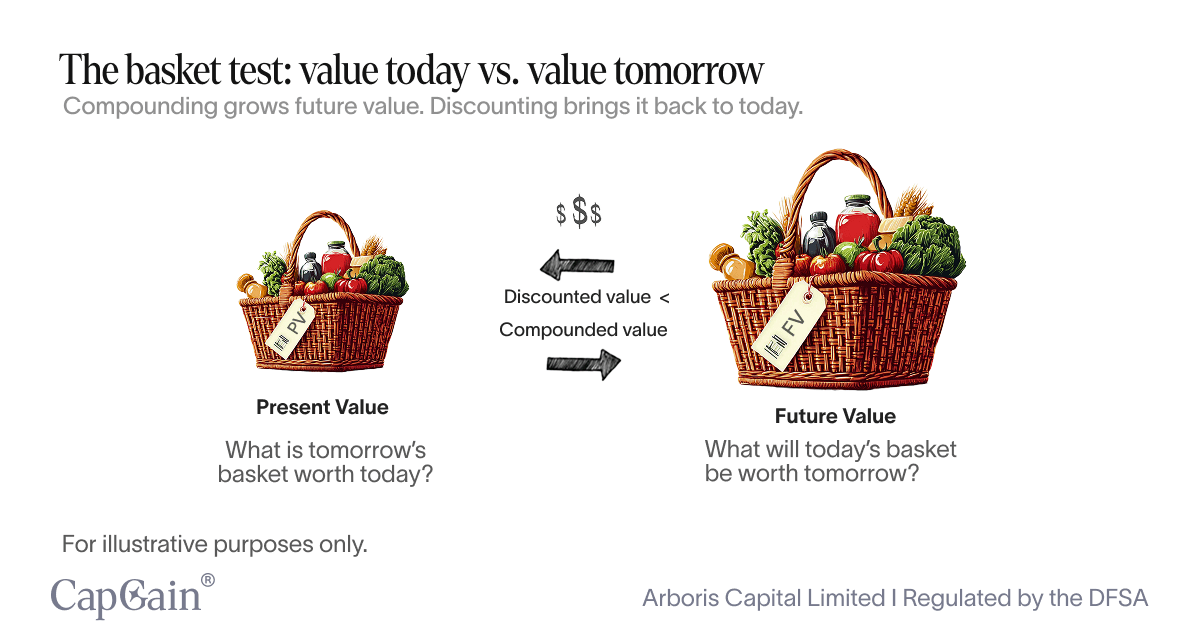

Present value: The value of money tomorrow

Insofar as we only explored the time value of money conceptually. To quantify the time value of money, we'll need to introduce a term called net present value, a central concept to understand IRR and investment opportunities in general.

We know that USD100 five years from now is worth less than USD 100 today. But how much less? And how much is USD 100 four years from now worth compared to USD 100 five years from now?

Remember, in essence, the time value of money means 'sooner rather than later.' Hence, while money four years from now might be worth less than USD 100 today, it's still worth more than USD 100 five years from now.

The present value ensures we are comparing like-for-like. To understand how and why, we need to dissect the time value of money effect into two main components: inflation and missed investment opportunities.

Inflation: Accounting for the economic reality

As noted earlier, inflation erodes the purchasing power of money over time. Therefore, when calculating the present value of a future amount, the first factor we need to consider is the loss of purchasing power.

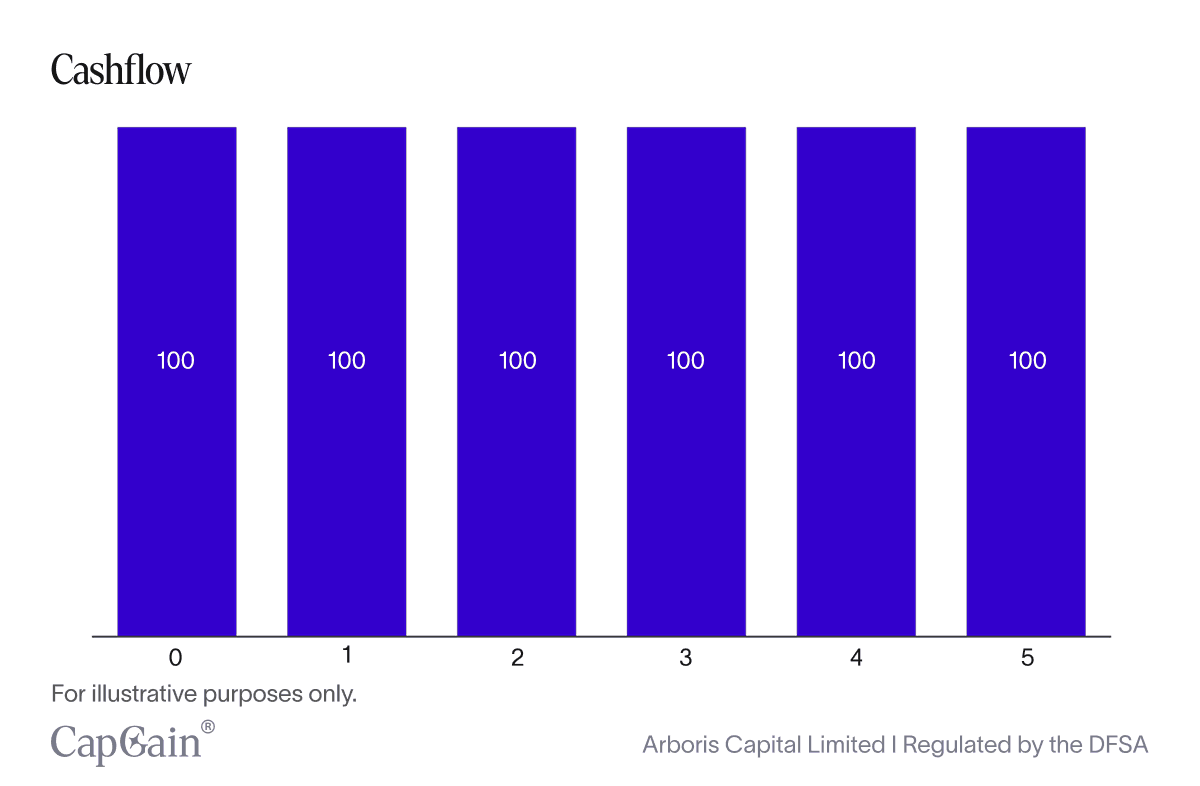

Let's examine an investment opportunity that yields USD 100 each year. The five-year cash flow is illustrated in the chart below, with each bar representing a nominal payment of USD 100.

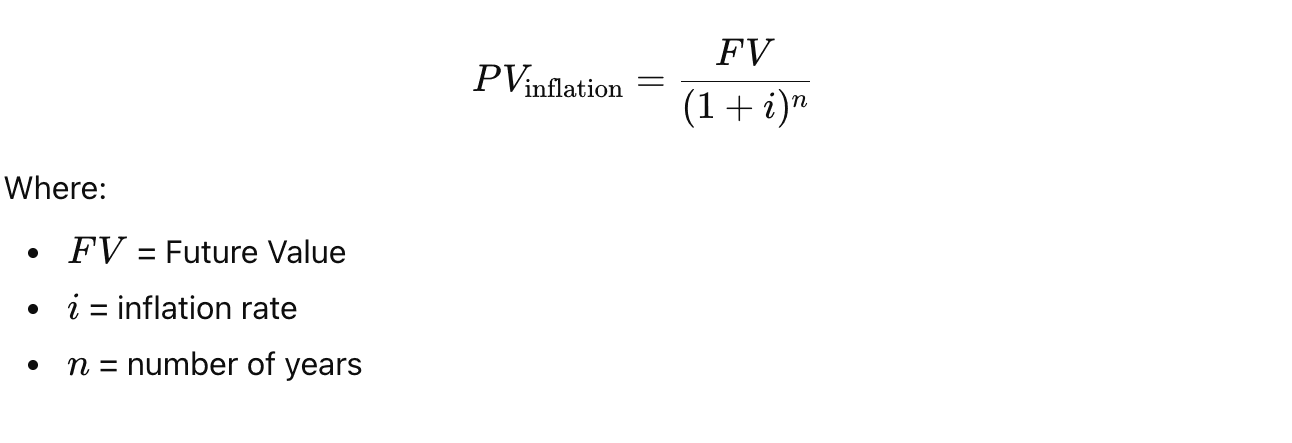

Each year, you receive exactly USD 100. However, as we now know, the value of the USD 100 decreases in part due to inflation. To adjust solely for inflation, we need to discount the cash flow back using the following formula:

If the concept of ‘discounting’ is not yet fully understood, there is no cause for concern; we will cover it in the next section. Meanwhile, for the ‘time’ being, you can think of discounting as 'reverse compounding.'

Compounding entails calculating what prices will increase due to inflation. With discounting, we derive the current value of future money, given expected inflation rates. Tomorrow's money in today's value, essentially.

Going back to our basket of groceries: compounding tells us how much that USD 100 basket will cost five years from now if prices rise at, say, 3% annually—roughly USD 116. That’s inflation in action.

Discounting, on the other hand, works in reverse: if we know that same basket will cost USD 100 in year five, and we expect inflation to average 3% per year, then we can calculate what it's worth in today’s prices—about USD 86. That’s the present value.

Illustrating inflation in action over time

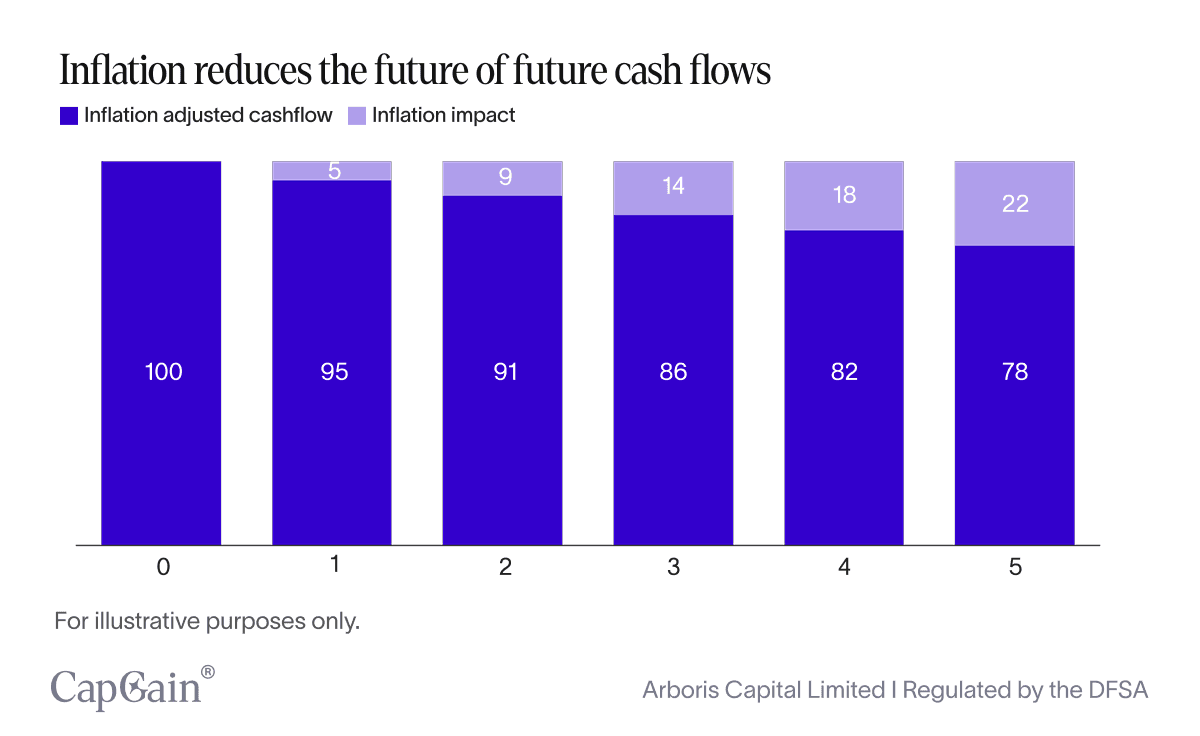

Now let’s look at a time series instead. To visualise the impact of a 5% inflation rate on the value of money over time, we can calculate how much USD 100 will be worth in future years, considering the eroding effect of inflation.

At present, in year 0, no time has passed, so inflation has no impact. USD100 today is USD 100 today. USD 100 a year from now is worth USD 95, corresponding to the expected inflation rate. A year later, the USD100 is worth USD 91, corresponding to a 9% decrease.

The reason for a less than 10% decrease in total over two years, contrary to what might be expected from simply adding two years of 5% decreases, is that the second year's 5% reduction is applied to the already reduced amount from the first year. This compounding effect results in a progressive reduction that is not straightforwardly additive.

For each year, we adjust the cash flow with the expected rate of inflation. As illustrated, the value of the USD 100 decreases over time as inflation carves out a greater part of the purchasing power.

To derive the inflation-adjusted value of the cash flow, we simply summarise the value of the discounted cash flows, i.e.

USD (95 + 91 + 86 + 82 + 78) = USD 433

From this, we see that the total adjustment is USD 67 over 5 years, meaning that USD 500 spread evenly over 5 years is worth USD 433 in "today's currency."

Opportunity cost – Quantifying the 'Could have, would have, should have'

In the earlier paragraph, we noted that USD100 in the future is worth less than USD 100 today, partly due to inflation. The other eroding factor is opportunity cost.

The term opportunity cost is often used in decision-making. For example, imagine you are contemplating taking a year off to travel the world. First, you list the costs associated with this sabbatical, e.g., flights, sights, accommodation, and so on. These are your direct costs. Meanwhile, to take all costs into account, you also need to factor in forgone salaries during that year. That's your opportunity cost.

Turning back to finance. Here, opportunity cost means that a USD 100 a year from now is worth less than USD 100 received today, because you could have invested your money today and gained a return by the end of the year. The missed financial gain is the opportunity cost. The could have, would have, should have component.

Example: Adjusting for the missed opportunity

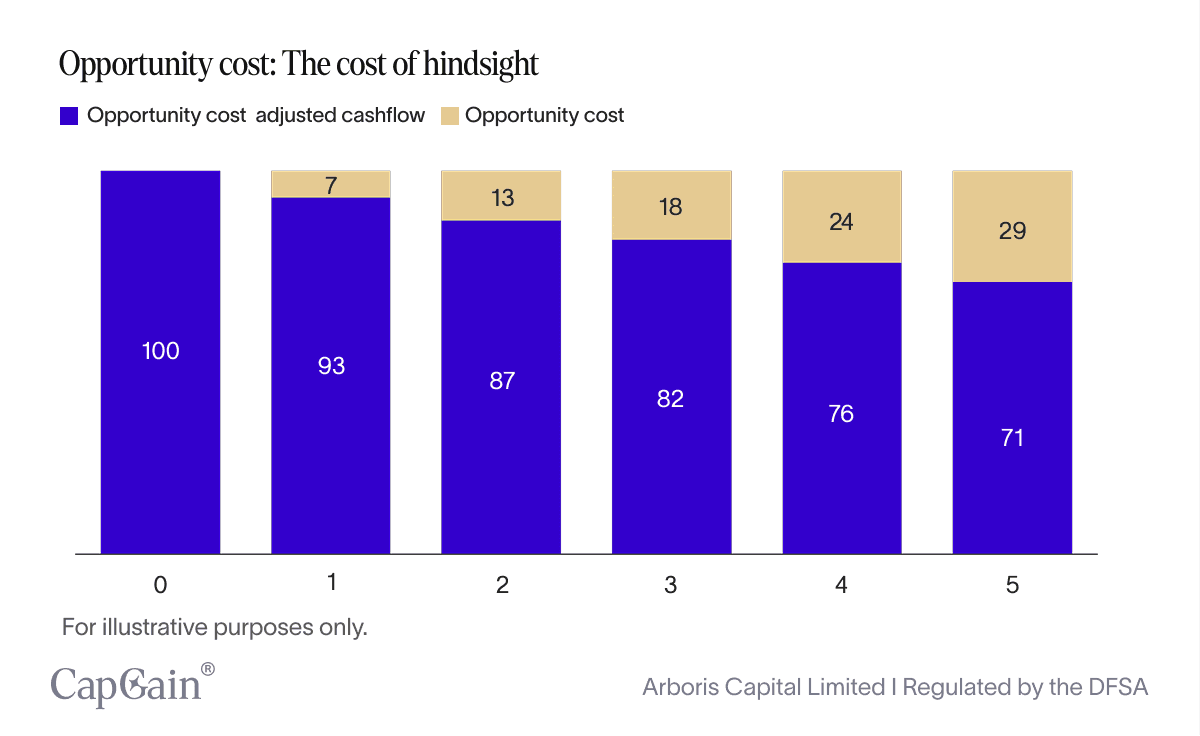

With that in mind, let's adjust our cash flow even further for opportunity costs. At present day, in year 0, no time has passed, meaning we haven't missed any investment opportunities. Hence, USD 100 is USD 100.

A year later, however, we can no longer assess the value of USD 100 in isolation. We need to take the opportunity cost into account.

Let's assume that you could have put your USD 100 in the bank and received a generous 7% annual interest rate on that USD 100. In economics, we call this the required rate of return: this is essentially what you could earn elsewhere.

Now, technically, this rate includes both the expected rate of inflation and any additional return necessary to compensate for the risk of deferring cash. Meanwhile, for the purpose of this illustration, we look at the interest rate alone.

Let's continue this example by calculating the present value of the 100 annual cash flow, adjusting for the opportunity cost represented by this 7% required rate of return.

To account for this, we employ the same methodology as before. In other words, we discount future cash flows based on missed opportunities.

Following the same methodology as before, USD 100 received a year from now, discounted back, is USD 93. I.e., USD 100 a year from now is worth USD 93 today. USD 100 received in two years is worth USD 87; by year 5, that USD 100 has shrunk to USD 71.

If we summarise the future cash flow, we find that the USD 500 is worth only USD 410 in today's value. The total opportunity cost amounts to USD 90.

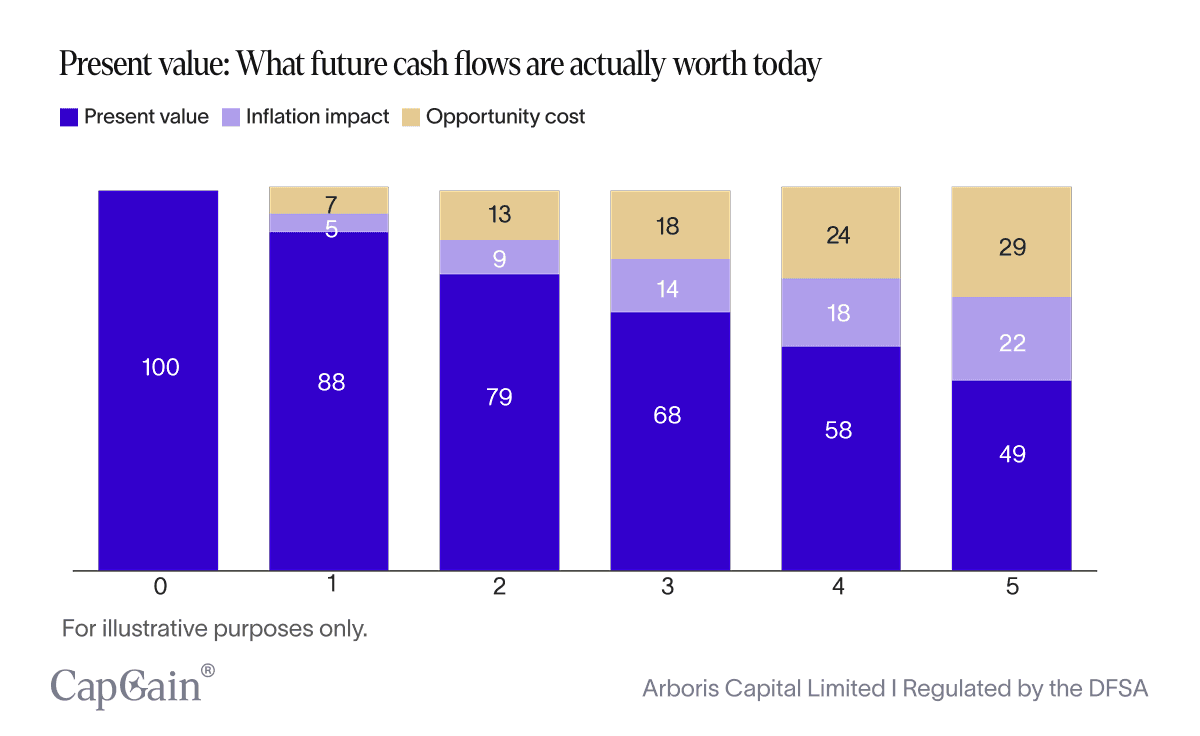

Reversing the clock: Discounting future cash flows into today’s money

Now, let’s bring it all together.

We’ve seen how both inflation and opportunity cost chip away at the value of future money. Over five years, these effects erode the value of a future USD 500 cash flow by a combined total of USD 157. That leaves us with a present value of USD 343—the amount you'd need today to match the purchasing power and investment potential of USD 500 received over time.

Discount rate: The greater the rate, the greater the regret

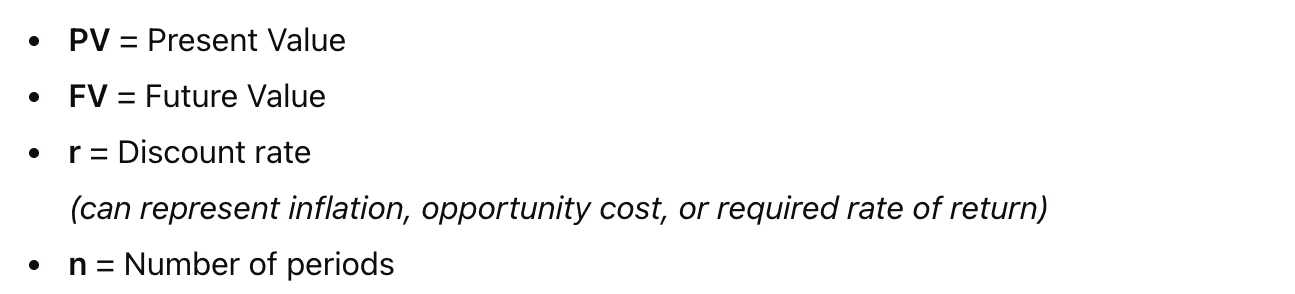

Hopefully, by now, this should make both mathematical and intuitive sense. Meanwhile, for the sake of cementing this, let's have another look at the formula:

Where

From this, you can see that both time and rate affect present value negatively.

Here’s the intuition:

As the number of years increases, the denominator in the present value formula grows, reducing the value of future cash flows.

As the discount rate rises, the denominator increases even more. That’s because the cost of deferring grows—you’re not just waiting, you’re missing out on more potential return.

Internal Rate of Return (IRR): A technical overview

And, finally, now to IRR.

IRR calculates the break-even rate: the return at which your investment’s future cash flows are worth exactly the initial cost when adjusted for time.

Now that we understand the time value of money and how to calculate present value, we can make sense of the internal rate of return (IRR). Unlike earlier examples where we chose the discount rate ourselves, IRR is the rate that makes the total value of all future cash flows exactly equal to the initial investment. In other words, IRR tells you the annual return an investment is expected to generate, after accounting for the timing of each cash flow.

Where

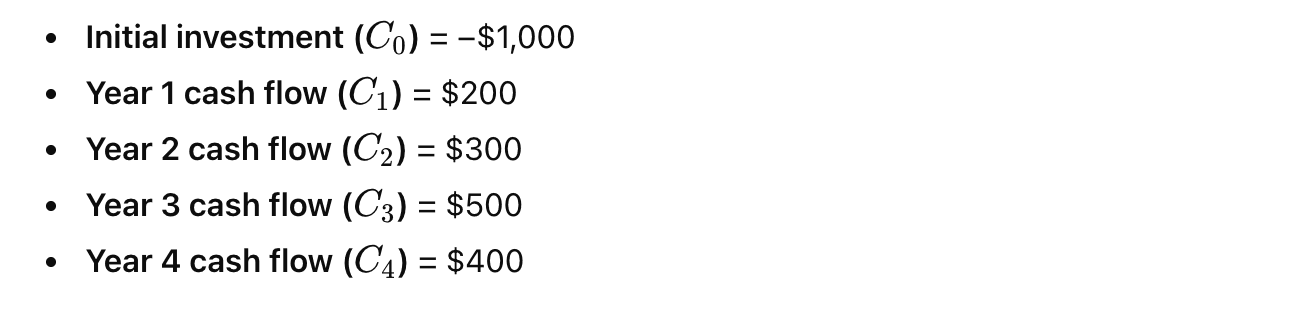

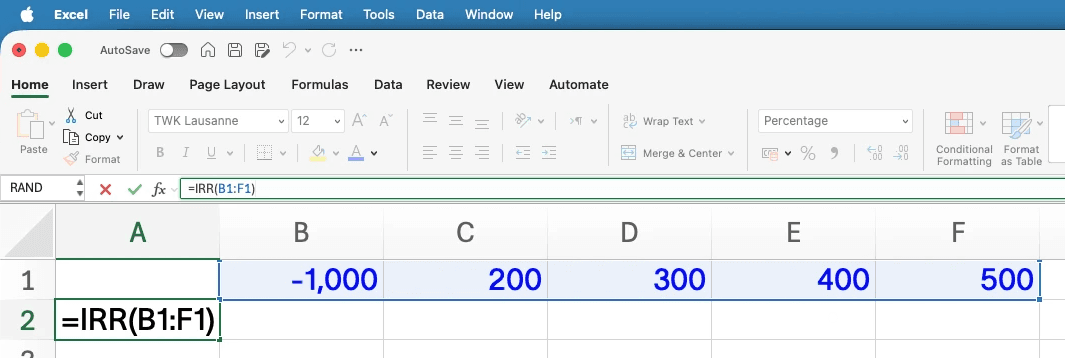

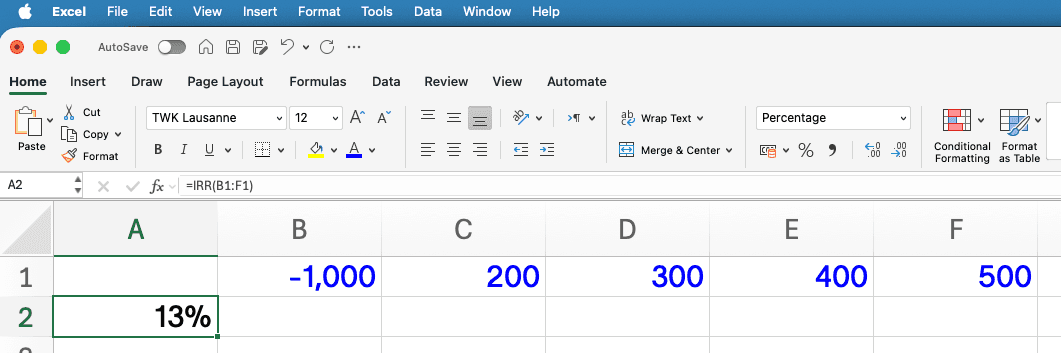

Consider an investment with the following cash flows:

Notice that the first number, 1,000, is negative. That is because this represents the investment. From the investor’s perspective, this is a cash outflow. The remaining (i.e., the returns) are inflows and therefore positive.

To find the IRR, you would need to solve this equation iteratively. Before you get your pencil out, it’s worth noting that these formulas require financial calculator software due to their complexity. In Excel, you can solve for this using the IRR formula:

What does this mean for you as an investor?

Understanding IRR enables you to compare investment opportunities on equal footing by taking timing into account. For example, imagine two investments: one pays USD 200 every year for five years, while the other pays USD 1,000 once, at the end of year five. Both total USD 1,000, but their value is not the same. The first returns capital gradually, allowing you to reinvest along the way. The second ties up your money for the full period. IRR captures that difference by reflecting not just how much you earn, but also the timing of your return.

Finally, it is worth noting that IRR is not a standalone performance measure. For a well-rounded assessment of the potential returns of an investment strategy, it’s important that you consider investment opportunities in terms of taking risk, correlation, and other performance measures into account. To learn more about IRR and other performance metrics in private equity, go to our masterclass to learn more.

Written by

Sarah Hansen

Head of Research

Disclaimer – For Professional Clients Only

This communication is intended solely for persons classified as Professional Clients as defined by the Dubai Financial Services Authority (DFSA). It is not directed at Retail Clients and should not be relied upon by any person who does not meet the criteria for classification as a Professional Client. The information provided herein is for general informational purposes only and does not constitute, and should not be construed as, an offer, solicitation, invitation, or recommendation to buy, sell, or otherwise transact in any investment product or to engage in any investment strategy.

The subject matter discussed does not relate to a DFSA-regulated financial product or service. The content is intended only to provide a general update on market conditions and does not consider the specific investment objectives, financial situation, or particular needs of any recipient. It should not be relied upon as the basis for any investment decision. Past performance is not a reliable indicator of future performance. The value of investments and any income from them may fluctuate, and there is no assurance that the original capital will be preserved or returned.

Although the information contained in this communication has been obtained from sources believed to be reliable, Arboris Capital Limited makes no representation or warranty as to its accuracy, completeness, or fitness for any particular purpose. No liability is accepted by Arboris Capital Limited, its employees, or affiliates for any direct or consequential loss arising from the use of or reliance on this material. Arboris Capital Limited is authorised and regulated by the Dubai Financial Services Authority (DFSA) and operates within the Dubai International Financial Centre (DIFC), United Arab Emirates.