Private equity works by pooling capital from institutional and private investors and deploying it into companies with the goal of improving their value over time. Private equity firms manage the full investment lifecycle — from sourcing and due diligence to active ownership and eventual exit. This article explains how private equity firms evaluate opportunities across macro, industry, and company-specific factors before investing.

Private equity firms raise capital from institutional and high-net-worth investors, pooling it into funds structured as limited partnerships.

These firms acquire controlling or minority stakes in companies with the goal of improving operations, scaling growth, and enhancing value.

Rigorous due diligence is central to investment selection, evaluating internal, industry, and macro factors before committing capital.

PE firms play an active role during the holding period—working closely with management to drive operational and strategic improvements.

The end goal is a profitable exit—via IPO, trade sale, or secondary buyout—engineered through careful timing and value creation.

How does private equity work?

In How Private Equity Works — A Walkthrough, we explained how private equity works in very practical terms, guiding you through every step of the fund lifecycle from deployment to distribution. But how does all this work? And what makes it work? To understand how this works, let’s take a closer look at the workings of private equity.

Putting your money to work

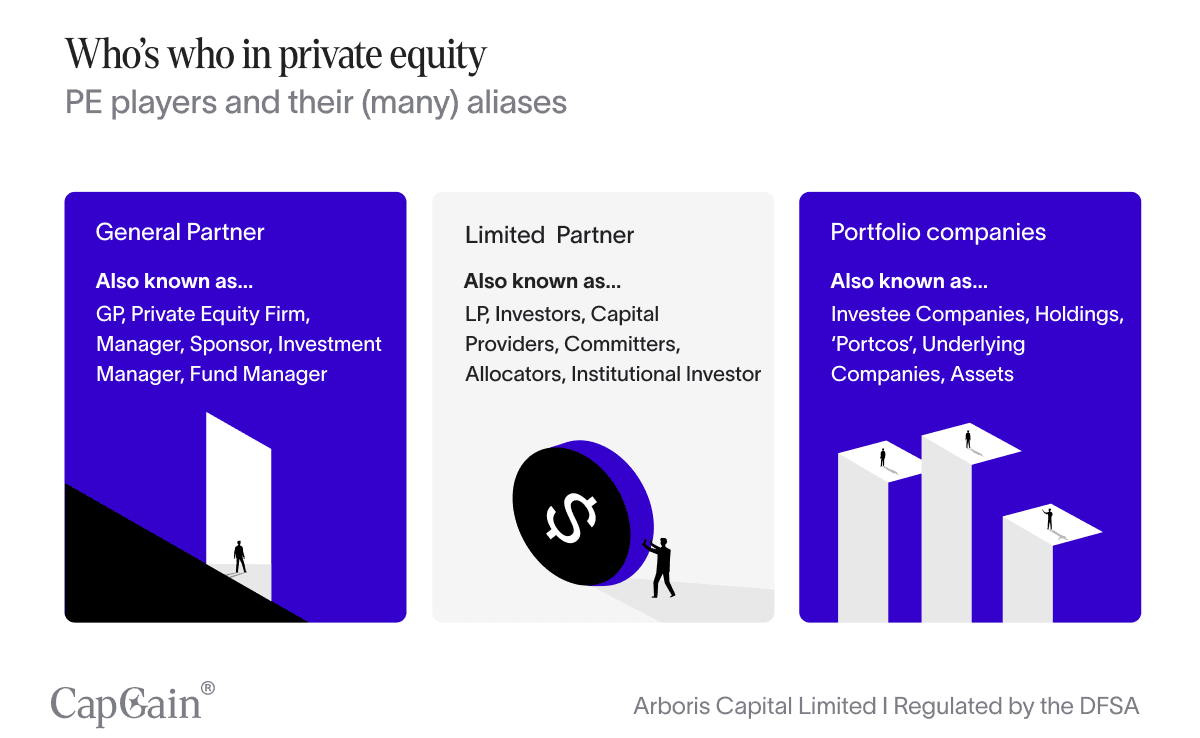

First, private equity (PE) firms raise capital from investors. These investors typically include pension funds, endowments, high-net-worth individuals, and institutional investors. The capital is pooled into an investment vehicle known as the private equity fund. The fund structure is a limited partnership, in which the investors represent the limited partners, or LPs.

The LPs have very little involvement and, more importantly, liability, in the fund. Instead, the private equity fund is managed by the private equity firm, also known as the PE firm, the General Partner (GP), or sometimes sponsors.

The fact that GPs go by so many names is fitting; their role is all-encompassing. They handle all aspects of fund management, from acquisition to investment, encompassing all that entails, including advising portfolio companies, reporting to investors, and planning for an eventual exit. Of course, they have highly skilled specialists dedicated to each of these tasks, but as an organisation, they are generalists.

Once the investors have committed capital, the private equity firm (or general partner, GP) uses this capital to acquire or invest in companies.

The goal is to improve these companies' value over a period of 5-7 years, and then exit the investment at a profit.

Note: In the paragraph above, we've used GP, General Partner, Sponsor, and PE firm interchangeably. They are the same. And no, this is by no means a deliberate ploy to keep you second-guessing your understanding. Instead, it's a subtle way to help you get familiar with the terminology. If you want to deepen your understanding of who is who in the industry, check out our novice guide to navigating the private equity industry.

Understanding the workings of the company

Now, how do they enhance the value of the companies in which they invest? It all starts during the initial stage, i.e., the screening process.

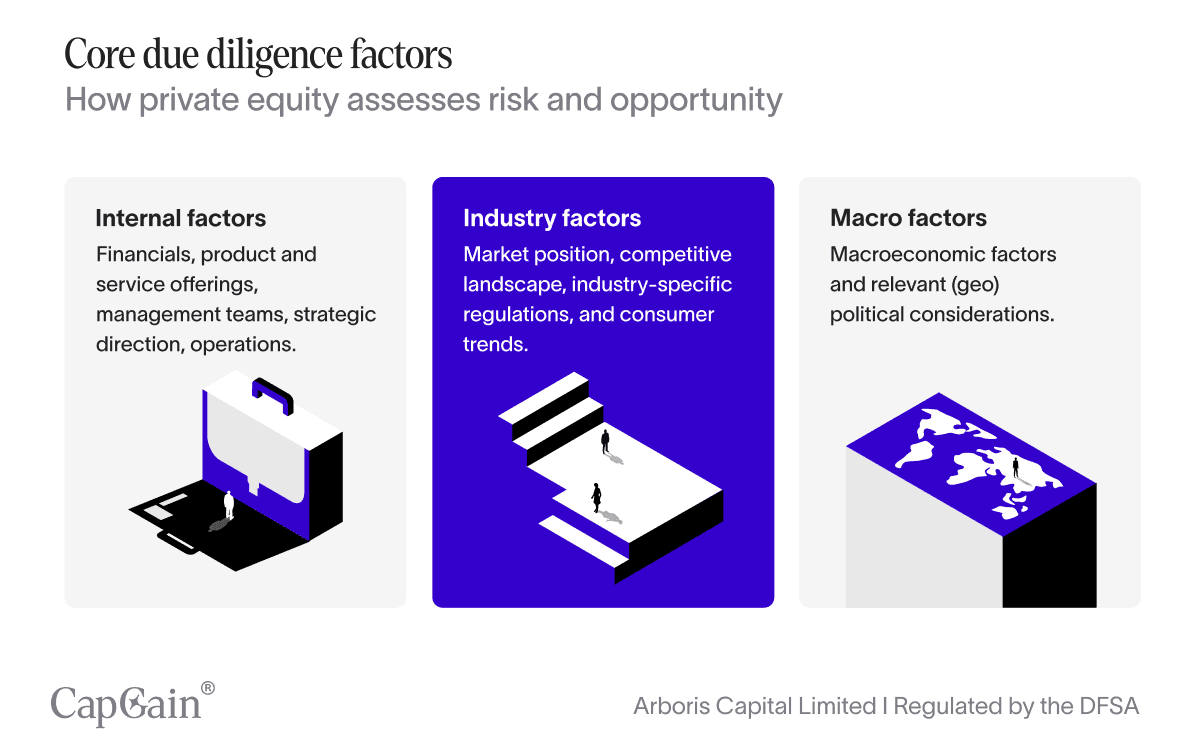

Before a PE firm decides to invest in a company, the prospect undergoes a strategic screening to assess whether the company is a good investment. This process is known as due diligence and involves analysing:

Internal factors: These include the company's financial statements, product and service offerings, management teams, strategic direction, and daily operations.

Industry factors: Market position, competitive landscape, industry-specific regulations, and consumer trends.

Macro factors: Macroeconomic factors and relevant (geo) political considerations.

Throughout this process, the PE firm meticulously scrutinises every aspect of the business. The objective is to identify areas for improvement to increase profitability and market share. If the investment prospect has enough potential, the private equity firm proceeds to invest in the company.

The terms of the investment differ according to the investment strategy. For example, whereas venture capital investments involve minority stakes and shorter time horizons, buyout acquisitions involve controlling stakes and have longer time horizons.

Want to dive deeper?

Private equity diligence goes deep: from macro conditions to industry dynamics to company-level operations, every layer of risk and opportunity is scrutinised before capital is deployed.

That discipline doesn’t end at investment. Across the holding period, private equity firms continue to manage—and actively mitigate—these risks through operational oversight, strategic adaptation, and close alignment with management. Explore our risk series to understand how PE navigates:

Industry Risk: Sector-specific regulation, disruption, and competition.

Company Risk: Operational, leadership, and execution risks within the firm.

But… What is the point?

The average stock market investor does just 6 minutes of research before buying shares in a company.¹

So why do private equity firms spend so much time making their investment decision? What's the point? Why undergo such rigorous procedures before investing? Why not just pick a few companies, see how it goes, and take it from there?

To understand why, it helps to remember: private equity doesn’t ‘buy and hope’ — it buys and builds.

The PE firm is not betting on the company improving over time, which is often the case with stock investments. Similarly, the PE firm does not have the opportunity to opt out if the company's value decreases.

From this perspective, private equity is fundamentally different from public equity. Private equity doesn't just buy a share in a company. Instead, private equity acquires a significant stake in the company to enhance its value through various initiatives.

These strategies are implemented over an extended period, often referred to as the holding period. Let's move to the next section to understand what happens during the holding period.

Working closely with the management team of investee companies

Post-acquisition, PE firms often take an active role in managing the company. They work closely with the existing management team to implement operational improvements, strategic initiatives, and financial restructuring.

In terms of understanding the 'workings of private equity', the short answer is active management. Private equity firms take an active role in making sure that the company realises its full potential. Throughout this process, PE firms often bring in operational experts and industry veterans to guide the company through changes. These can include optimising supply chains, improving cost structures, and enhancing product or service offerings.

It also includes regular performance monitoring and strategic reviews to ensure that the company stays on track with the growth plan. PE firms set performance targets and key performance indicators (KPIs) to measure success.

Throughout the investment period, PE firms focus on creating value to ensure that the company is more attractive to potential buyers or public markets, which brings us to the final point.

Working towards an exit

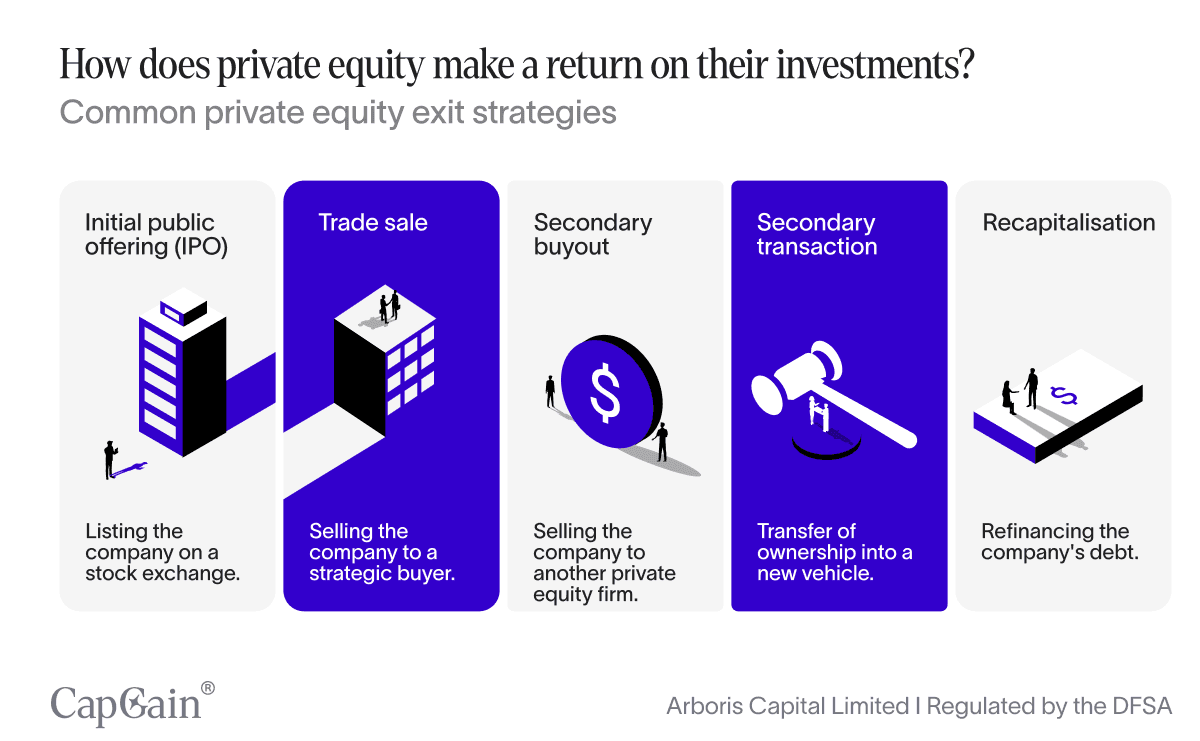

Now comes the final payoff: the exit. The ultimate goal of a PE firm is to exit the investment at a profit. This can be achieved through various strategies, such as:

Initial Public Offering (IPO): Taking the company public by listing it on a stock exchange.

Trade sale: Selling the company to another business or strategic buyer. Also known as a strategic sale.

Secondary buyout: Selling the company to another private equity firm.

Secondary transaction: Selling an existing ownership stake to another investor to provide liquidity to existing LPs.

Recapitalisation: Refinancing the company's debt to distribute cash back to investors while retaining ownership.

Much like public investments, the timing of the exit is crucial. PE firms aim to exit investments during favourable market conditions to maximise returns. This involves careful planning and market analysis to identify the optimal time for the sale or IPO.

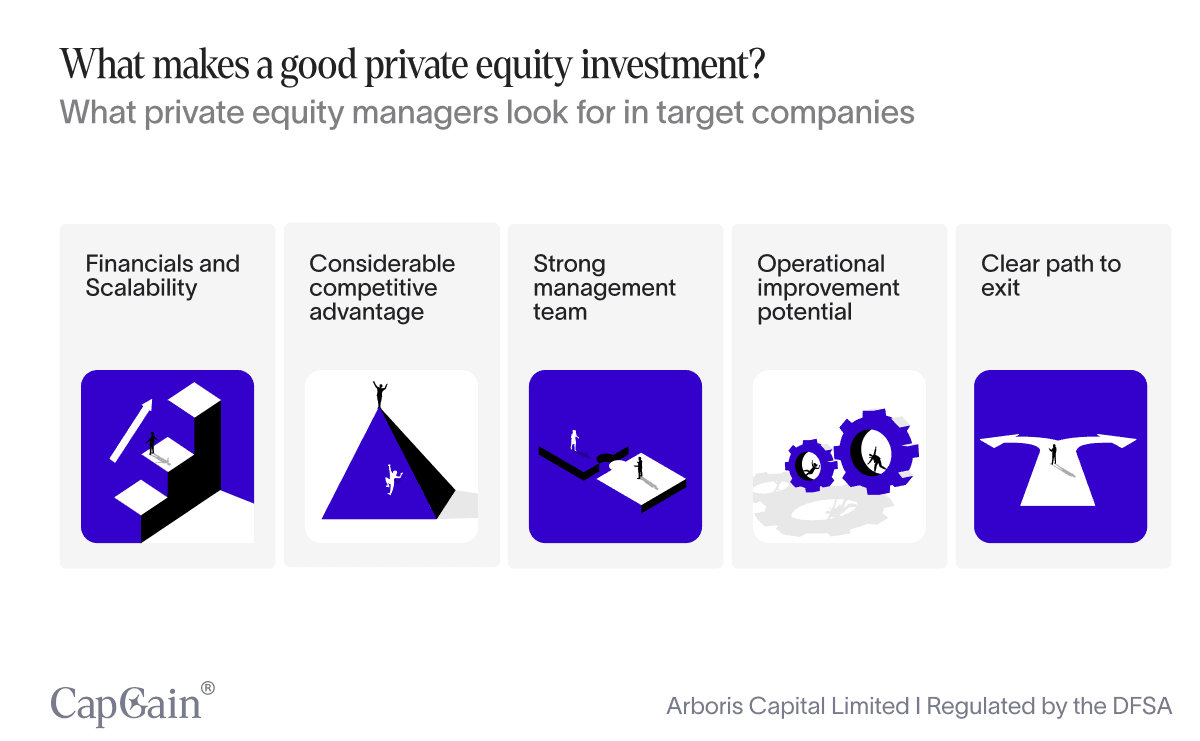

What makes a private equity investment “work”

And finally, a bonus question for the curious: What makes private equity work?

Insofar as we’ve looked at how private equity investing works, we’ve explained the key steps involved in putting capital to work and helping companies grow through strategic deployment of this capital. We’ve only scratched the surface, and we’ll take a closer look at these in subsequent chapters, but for now, let’s switch our attention to how private equity investments work. That is what makes a good private equity investment:

Strong financials and scalability: Companies with consistent revenue growth, profitability, and potential to scale without proportional cost increases are prime PE targets.

Competitive advantage: Strong market position and clear differentiation—through brand, IP, innovation, or customer base—enhance attractiveness.

Strong management team: Experienced leadership aligned with investor goals is critical to executing growth and delivering returns.

Operational improvement potential: Opportunities to boost efficiency or implement strategic growth initiatives are key value drivers.

Clear exit strategy: Viable exit options—such as trade sale, IPO, or secondary buyout—are essential for realising returns.

Ultimately, what makes private equity work is the disciplined execution of a strategy that transforms potential into performance.

The best investments combine sound fundamentals with a clear path to enhancement and exit. Private equity thrives at the intersection of operational excellence, strategic foresight, and aligned incentives. When done well, it’s not just about buying and selling companies—it’s about building better ones.

Lastly, since each company is unique with its distinct characteristics and growth potential, there is no one-size-fits-all approach. Instead, the private equity firms tailor their strategies to match each target company's unique needs and circumstances. These strategies are designed to maximise value and achieve the best possible outcomes for both the firm and its investors.

To explore how each of these strategies works in detail, explore our masterclass.

Sources:

Saxo, Many investors buy stocks blindfolded—why spending six minutes on research isn’t enough, May 14 2025, Accessed July 22 2025. https://www.home.saxo/en-mena/content/articles/equities/investor-stock-research-14052025

Written by

Sarah Hansen

Head of Research

Disclaimer – For Professional Clients Only

This communication is intended solely for persons classified as Professional Clients as defined by the Dubai Financial Services Authority (DFSA). It is not directed at Retail Clients and should not be relied upon by any person who does not meet the criteria for classification as a Professional Client. The information provided herein is for general informational purposes only and does not constitute, and should not be construed as, an offer, solicitation, invitation, or recommendation to buy, sell, or otherwise transact in any investment product or to engage in any investment strategy.

The subject matter discussed does not relate to a DFSA-regulated financial product or service. The content is intended only to provide a general update on market conditions and does not consider the specific investment objectives, financial situation, or particular needs of any recipient. It should not be relied upon as the basis for any investment decision. Past performance is not a reliable indicator of future performance. The value of investments and any income from them may fluctuate, and there is no assurance that the original capital will be preserved or returned.

Although the information contained in this communication has been obtained from sources believed to be reliable, Arboris Capital Limited makes no representation or warranty as to its accuracy, completeness, or fitness for any particular purpose. No liability is accepted by Arboris Capital Limited, its employees, or affiliates for any direct or consequential loss arising from the use of or reliance on this material. Arboris Capital Limited is authorised and regulated by the Dubai Financial Services Authority (DFSA) and operates within the Dubai International Financial Centre (DIFC), United Arab Emirates.